Buy Poonawalla Fincorp Ltd for the Target Rs.560 by Motilal Oswal Financial Services Ltd

Strategic scale, operating leverage to drive profitability

AUM poised for robust growth, supported by improving asset quality

* Poonawalla Fincorp (PFL) has largely moved past its portfolio clean-up and balance sheet repair phase and is now transitioning into a structurally stable growth cycle, supported by a rebuilt operating platform.

* The company has re-architected its business model with deeper AI-led integration across underwriting, fraud detection, risk analytics, collections, and targeted marketing, enabling sharper credit selection, faster turnaround times and more efficient customer acquisition. As a result, PFL is witnessing strong traction across its newly launched product segments, with disbursement momentum accelerating across all its verticals. New businesses already contribute ~11% of AUM and ~20% of quarterly disbursements, highlighting rising customer acceptance, improving distribution throughput, and increasing diversification.

* The ~INR15b equity capital infusion by the promoter group in early FY26 underscores strong promoter commitment and provides incremental balance sheet comfort, reinforcing confidence in the company’s long-term growth roadmap. In addition, we view the proposed ~INR55b capital raise as a proactive growth initiative rather than a balance sheet requirement. This equity capital will support management’s ambition of delivering ~35- 40% AUM CAGR over the medium term while accelerating expansion in secured lending segments such as gold loans, CV finance and MSME lending.

* Over the past two years, PFL has evolved into a management-led franchise, supported by stronger governance frameworks, institutionalized processes and a cultural reset that has materially improved PFL’s execution credibility. The platform is no longer dependent on a single individual, with experienced vertical heads capable of managing significantly larger balance sheets, positioning the company for the next phase of scale-up under the leadership of MD & CEO Arvind Kapil.

* We believe PFL’s diversified multi-product architecture, supported by a balanced mix of secured and unsecured lending, enhances earnings resilience and moderates credit cost volatility across cycles. The company continues to expand its product suite, distribution reach and geographic presence while leveraging AI-driven operating efficiencies to improve productivity without compromising asset quality. As profitability stabilizes and return ratios improve, this combination of disciplined growth and operating leverage should support gradual valuation re-rating over the medium term.

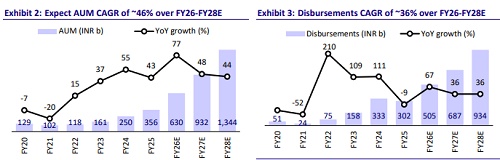

* PFL currently trades at 2.2x FY27E P/B, and we estimate AUM/PAT CAGR of ~46%/129% over FY26-FY28E, with RoA/RoE expected to reach ~2.5%/15% by FY28E. We reiterate our BUY rating with a target price of INR560 (based on 2.7x Dec’27E BVPS)

Strategic multi-product expansion fueling strong, diversified growth

* PFL is entering a new phase of growth, supported by sustained investments in branch expansion, digital infrastructure, and management capability. These initiatives have enabled a successful launch and a rapid scale-up of multiple lending verticals, including prime personal loans (~7.3% of AUM), gold loans (~1.2%), education loans (~1.1%), consumer durable loans (~0.6%) and commercial vehicle loans (~1.1%). Together, these businesses are expanding the company’s presence across both secured and unsecured retail lending segments while strengthening the breadth of its product portfolio.

* The company’s multi-product, multi-channel strategy is aimed at building a diversified and scalable retail franchise. In 3QFY26, these new products contributed ~11% to AUM and ~20% to total disbursements, highlighting early traction and a gradual increase in portfolio diversification. This growth is supported by a robust distribution ecosystem spanning digital platforms, physical branches, dealer networks and advisor partnerships, which not only supports product scale-up but also enhances cross-selling opportunities.

* High-velocity products such as consumer durable loans help build a large customer funnel, while long-tenure products like education loans enhance customer lifetime value and relationship depth. These new businesses complement PFL’s core portfolio, which continues to account for ~89% of AUM, and together position the company to deliver strong AUM growth of ~46% over FY26E-FY28E while improving portfolio diversification, strengthening customer engagement, and supporting sustained profitability.

AI- led transformation unlocking operating leverage

* Artificial intelligence is emerging as a key pillar of PFL’s operational transformation, enabling the company to enhance productivity, strengthen governance and improve customer experience while building a scalable, datadriven operating platform. AI integration across the lending lifecycle is improving underwriting quality, automating KYC and document validation processes, and enabling multilingual customer engagement via conversational bots. At an organizational level, internal tools such as BuildBuddy and DartGenie are accelerating application development and enabling faster data-driven insights, allowing teams to focus more on strategic and value-added initiatives.

* Importantly, these technology investments are translating into tangible operating efficiencies. Despite ongoing expansion in its branch network and geographic footprint, PFL expects structural and AI-led productivity gains to drive a meaningful improvement in operating efficiency, with the cost-toincome ratio projected to decline from ~52% in FY26E to ~42% by FY28E, alongside a gradual reduction in the opex-to-AUM ratio.

Diversified credit mix to support stable asset quality and earnings stability

* PFL continues to reposition its loan portfolio toward a more granular, retaildriven and diversified structure, with a deliberate increase in secured and prime borrower segments to reduce credit volatility across cycles. The company has guided for a gradual moderation in credit costs, supported by the rising contribution from relatively lower-risk segments such as gold loans, education loans and loan against property (LAP), which should enhance portfolio resilience over time.

* Although reported credit costs stood at ~2.6% in 3QFY26, largely attributed to the instant personal loan segment, its core portfolios’ credit costs remain stable in the ~1.4-1.5% range. Importantly, portfolio-level six-month-on-book 30+ delinquencies have eased meaningfully, reflecting improved underwriting discipline in recent vintages. Asset quality trends remain encouraging, with unsecured salaried loans reporting 6 MoB 30+ dpd of only ~0.4%, reinforcing confidence in a structurally strengthening credit profile. As the portfolio mix continues to shift toward secured and prime segments, we expect credit costs to decline from ~2.6% in FY26E to ~2% in FY27 and further to ~1.9% in FY28.

Valuation and view

* We believe PFL is evolving into a structurally stronger, digitally enabled, and well-diversified retail NBFC, supported by disciplined growth execution, improving asset quality and visible operating leverage. The company’s calibrated shift toward secured and prime lending segments, combined with an improving bias in margins and a gradual moderation in credit costs, should enhance its earnings visibility while reducing volatility across cycles. At the same time, sustained investments in technology, AI and governance frameworks are driving productivity gains and improving operational efficiency, even as the company continues to expand its branch network and geographic footprint.

* PFL currently trades at 2.2x FY27E P/B, and we estimate AUM/PAT CAGR of ~46%/129% over FY26-FY28E, with RoA/RoE expected to reach ~2.5%/15% by FY28E. We reiterate our BUY rating with a target price of INR560 (based on 2.7x Dec’27E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041