Neutral Voltas Ltd for the Target Rs.1,250 by Motilal Oswal Financial Services Ltd

Weak earnings; margin pressure continues in UCP Price hikes offset cost partially; channel inventory declined

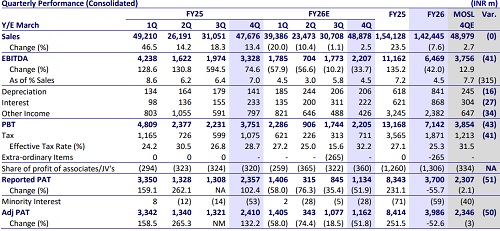

* Voltas (VOLT)’s 4QFY26 earnings were significantly below our estimates due to lower revenue and margin in UCP segment vs. our estimates. Revenue was up marginally ~3% YoY to INR48.9b (in line), while EBITDA declined ~34% YoY to INR2.2b (~41% miss). OPM contracted 2.5pp YoY to ~4.5% (est. 7.7%). Adj PAT declined ~52% YoY to INR1.2b (~50% miss).

* Management indicated significant margin pressure due to commodity inflation, INR depreciation and West Asia crises. Price hikes of ~5-10% were taken for the BEE rating changes and ~2% for commodity inflation so far. Further price increases may be necessary as inflation remains high across key raw materials. It guided for a gradual improvement in margin, backed by demand improvement and cost-optimization initiatives like localization, value engineering, sourcing efficiencies and manufacturing automation. Channel inventory has declined and is currently closer to 30 days.

* We cut our EPS estimates by ~19%/11% for FY27/FY28 due to persistent margin pressure in UCP segment. We arrive at a revised TP of INR1,250 based on SoTP (45x FY28E EPS for the UCP segment, 20x FY28E EPS for the PES and EMPS each, and INR20/sh for Voltbek). Reiterate Neutral.

UCP revenue rises ~1% YoY; UCP margin dips 5pp to 5.0%

* Consol. revenue/EBITDA/adj. PAT stood at INR48.9b/INR2.2b/INR1.2b (+3%/-34%/-52% YoY and in line/-41%/-50% vs. our est.) in 4QFY26. Depreciation increased ~47% YoY, while interest cost declined ~5%. Other income declined ~47%.

* Segmental highlights:

1) UCP – Revenue increased ~1% YoY to INR34.9b, EBIT declined ~50% YoY to INR1.7b, while EBIT margin contracted 5pp YoY to 5.0%.

2) EMPS – Revenue grew 5% YoY to INR11.9b, EBIT stood at INR756m vs. loss of INR17m in 4QFY25, and EBIT margin surged 6.5pp YoY to 6.4%.

3) PES – Revenue rose 27% YoY to INR1.6b, EBIT increased ~10% YoY to INR376m, and EBIT margin contracted 3.5pp YoY to 22.3%.

* In FY26, consol. revenue/EBITDA/adj. PAT stood at INR142.5b/INR6.5b/ INR4.0b (-8%/-42%/-53% YoY). UCP/EMPS/PES segment revenue stood at INR95.0b/INR40.5b/INR6.0b (-10%/-3%/+5% YoY). UCP EBIT declined ~66% YoY to INR3.1b, and EBIT margin contracted 5.2pp YoY to 3.2%. CFO stood at INR710m vs. cash outflow of INR2.2b in FY25. Capex stood at INR1.3b vs. INR2.1b in FY25. Net cash outflow stood at INR617.8m vs. INR4.3b in FY25

Valuation and view

* VOLT’s 4QFY26 performance was significantly below our estimates, due to persistent margin pressure in the UCP segment and lower revenue. RAC business is estimated to face challenges due to input cost pressure and high dependance on weather conditions. Variability in summer intensity and seasonal patterns may significantly impact sales momentum and operating leverage, while ongoing commodity inflation and pricing competition further constrain margin recovery.

* We estimate VOLT’s revenue/EBITDA/PAT CAGR at ~15%/47%/62% over FY26- 28, albeit on a low base (CAGR at ~7%/8%/8% over FY25-28). Estimate UCP revenue CAGR at ~18% over FY26-FY28 (~8% over FY25-28), with UCP margin at 5.5%/7.0% in FY27E/FY28E (3.2% in FY26) vs. average of 8.4% over FY23-25. The stock is trading at 57x/41x FY27E/FY28E EPS. We reiterate our Neutral rating on the stock with a revised TP of INR1,250, based on 45x FY28E EPS for the UCP segment, 20x FY28E EPS for the PES and EMPS (each), and INR20/sh for Voltbek.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)