Neutral Cipla Ltd for the Target Rs.1,380 by Motilal Oswal Financial Services Ltd

Weak US flow; strong India show US growth to pick up from 2HFY27 onwards

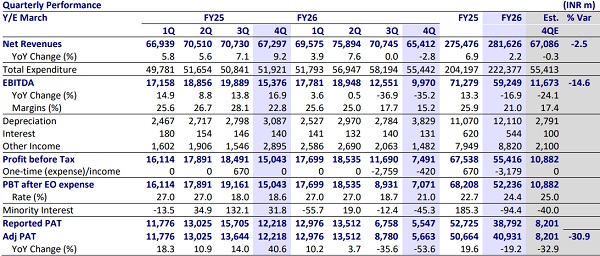

* Cipla (CIPLA) delivered in-line revenue for 4QFY26. However, it delivered 15%/31% miss on EBITDA/PAT for the quarter. Lower-than-expected revenue in North America (NA), Emerging Markets (EM), and API segment, coupled with reduced operating leverage, dragged overall performance for the quarter.

* The YoY decline in NA sales intensified in 4QFY26, supported by competition in g-Lenalidomide and adverse regulatory impact on the off-take of lanreotide.

* This was offset, to some extent, as the Indian business, comprising Domestic Formulation (DF), trade generics, and consumer wellness, reported a broadbased double-digit YoY growth during the quarter.

* The African business, comprising private markets, tender business, and North Africa, also grew at a healthy rate of 14% YoY (in CC terms) for the quarter.

* We have reduced our earnings estimate by 10% for FY27, factoring in:

a) the ongoing regulatory issue with respect to Lanreotide for the US market

b) the adverse impact of geopolitical tension in emerging markets and enhanced marketing/promotional spend.

* We value CIPLA at 23x 12M forward earnings to arrive at a TP of INR1,380. We expect earnings to remain under check due to a reduction in contribution from g-lenalidomide and some gestation period for the accruing of upcoming niche launches. Reiterate Neutral rating on the stock.

Product mix and reduced operating leverage drag profitability YoY

* CIPLA’s 4QFY26 revenue declined 2.8% YoY to INR65.4b.

* Gross margin contracted 430bp YoY to 63.2%.

* EBITDA margin contracted 760bp YoY to 15.2% (our est. 17.4%), largely due to higher R&D/employee expenses (up 145/90bp as a % of sales).

* EBITDA declined 35.2% YoY to INR9.9b (our est. INR11.7b).

* Adj. PAT declined 53.6% YoY to INR5.7b (our est. INR8.2b). We await clarity on the sharp increase in depreciation/amortization in 4QFY26 (INR3.8b vs INR3b YoY and INR2.8b QoQ).

* Extraordinary items of INR420m include impairment of investment in associates.

* For FY26, CIPLA delivered 2.2% YoY growth in revenue to INR281.6b, while it delivered 17%/19% YoY decline in EBITDA/PAT to INR59.2b/INR40.9b.

Valuation and view:

* We reduce our earnings estimate by 10% for FY27, factoring in:

a) the ongoing regulatory issue with respect to Lanreotide for the US market

b) the adverse impact of geo-political tension in emerging markets and enhanced marketing/promotional spend.

* We value CIPLA at 23x 12M forward earnings to arrive at a TP of INR1,380. We expect earnings to remain under check due to a reduction in contribution from g-lenalidomide and some gestation period for accruing of upcoming niche launches. Hence, we reiterate a Neutral rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412