Buy Federal Bank Ltd for the Target Rs.325 by Motilal Oswal Financial Services Ltd

Steady quarter; one-offs prudentially utilized to fortify the B/S

Core NIM and asset quality ratios improve

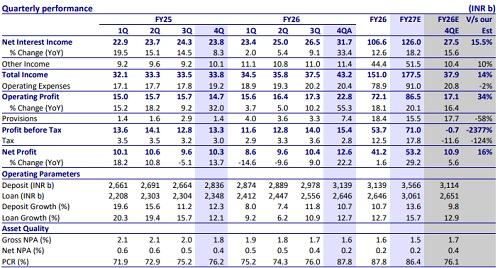

* Federal Bank (FB) reported 4QFY26 PAT of INR12.6b (up 22% YoY/21% QoQ, 16% beat), led by healthy NII and tax reversal of INR1.15b.

* NII was up 33% YoY/20% QoQ to INR31.7b (15% beat amid interest on IT refund and inline otherwise). The NIM improved 8bp YoY/2bp QoQ to 3.2% (3.74% on a reported basis).

* Advances grew 12.7% YoY/3.5% QoQ. Deposits grew 11% YoY/5% QoQ, while CASA growth stood at 20.6% YoY/ 8.3% QoQ, leading to an improvement in CASA mix to 32.9% (vs. 32.1% in 2QFY26).

* Provisions stood at INR7.4b, as the bank created floating provisions of INR4.6b (inline otherwise). Slippages increased to INR4.83b (INR4.43b in 3QFY26) while GNPA/NNPA ratios declined 10bp/ 22bp QoQ to 1.62%/0.2%.

* We raise our PAT estimates by ~2.5%/2.3% for FY26/FY27, factoring in NIM expansion, healthy fee, and loan growth outlook. We estimate FB to deliver an FY27E RoA/RoE of 1.26%/12.2%. Reiterate BUY with a TP of INR310 (based on 1.7x Sep’27E ABV).

NIM dips 2bp QoQ; CASA mix improves to 32.9%

* FB reported 4Q earnings of INR12.6b (up 22% YoY/21% QoQ, 16% beat) amid healthy NII and lower tax outgo.

* NII grew 33% YoY/20% QoQ (15% higher, amid interest on IT refund and inline otherwise). The NIM expanded 2bp QoQ to 3.2%, led by CoF reduction and steady growth in mid-yielding assets as well as improvement in CASA mix.

* Other income grew 14% YoY/4% QoQ to INR11.4b (10% beat). Treasury profits came in at INR120m vs INR1.26b in 3QFY26.

* Opex grew 6.4% YoY/1% QoQ (in line). The bank expects the C/I ratio to be range-bound at 53-55% in the near term. PPoP increased 55% YoY/32% QoQ to INR22.8b (INR18.2b on an adjusted basis, which represents a 6% beat).

* On the business front, advances jumped 12.7% YoY/3.5% QoQ to INR2.64t, driven by a healthy growth in gold loans (9% QoQ) and CVs (8.5% QoQ). In contrast, the corporate book stood flat QoQ. Within retail, LAP and credit cards continued to witness healthy traction, whereas HL saw subdued growth.

* Deposit growth was healthy at 10.7% YoY/5.4% QoQ, led by robust growth in CA (up 23.2% YoY/19.1% YoY), while SA book grew by 19.7% YoY/5.2% QoQ. As a result, the CASA mix improved to 32.9% from 32.1% in 3QFY26.

* Provisions stood at INR7.4b, as the bank created floating provisions of INR4.6b (inline otherwise). Slippages increased to INR4.83b (INR4.43b in 3QFY26). GNPA/NNPA ratios declined 10bp/22bp QoQ to 1.62%/0.2%.

Key highlights from the management commentary

* The bank has deliberately reduced wholesale deposits due to higher costs, which should be viewed as a strength rather than a weakness.

* Further scope for deposit repricing remains, likely extending into 1Q & 2QFY27.

* Floating NPA provisions are aligned with floating standard provisions and can be utilized during the upcoming ECL transition.

* One-off gains included interest on the tax refund (~INR4.5bn) and tax reversal (~INR1.15bn), along with direct net worth adjustments related to the reversal of excess tax provisions.

* The bank continues to focus on mid-market corporates rather than large corporates, as the focus remains on continued improvement in high-yielding asset mix.

Valuation and view:

Reiterate BUY with a TP of INR325 FB reported a steady quarter, albeit impacted by one-offs, with a tax provisioning reversal of INR1.15b being utilized towards floating provisions. The NIM remained largely stable QoQ at 3.2%, with further tailwinds expected from the repricing of the cost of funds, even as the share of mid-yielding assets continues to rise. Loan growth remained healthy, led by strong traction in SME, gold loans, and CV, along with a gradual recovery in the MFI segment. Deposit growth stood at 11% YoY, supported by healthy CASA accretion, resulting in a sequential improvement in the CASA ratio to 32.9%. Asset quality improved during the quarter, with both GNPA and NNPA ratios trending lower. We expect asset quality to remain broadly stable over FY27–28E, with credit costs likely to stay contained at ~50–55bp over the same period. We raise our PAT estimates by ~2.5%/2.3% for FY26/FY27, factoring in NIM expansion, healthy fee, and loan growth outlook. We estimate FB to deliver an FY27E RoA/ RoE of 1.26%/12.2%. Reiterate BUY with a TP of INR310 (based on 1.7x Sep’27E ABV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)