Buy CG Power and Industrial Solutions Ltd For Target Rs.940 Motilal Oswal Financial services Ltd

Capacity commissioning to aid growth

CG Power’s FY26 result came in line with respect to revenue and EBITDA, while the outperformance on earnings was led by higher other income and a lower-thanexpected tax rate. Order inflows for the year remained strong at INR196b (up 34% YoY), primarily led by strong inflows in the power systems division. The division’s performance remained strong, driven by a healthy demand environment, pricing power, and efficient execution. The company’s capacity will increase to 1,10,000 MVA after the current ongoing capex. The industrial system performance was relatively weaker on inflows and revenue, while price hikes of nearly 17.5% taken during the entire year helped in passing through the RM cost inflation. We expect losses from the OSAT division to begin narrowing down from FY28 as the second phase of capacity expansion would be completed by the end of CY26. We expect strong pricing power in the power systems segment, the ability to pass through RM cost pressures in industrial systems, and the narrowing of losses from the OSAT division to result in margin improvement from FY28. We tweak our estimates by 6%/5% for FY27/28 to bake in better margins in power systems and other BS details. We roll forward our SoTP-based TP to Jun’28 and reiterate our BUY rating with a TP of INR940.

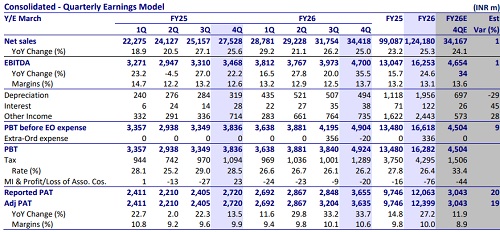

In-line revenue and EBITDA, while PAT beat our estimate Consolidated revenue grew 25% YoY to INR34b in 4QFY26, driven by strong performance in the power systems division (+50% YoY), while industrial systems grew 2% YoY. Gross margin expanded 230bp YoY to 32.1%, while EBITDA increased 36% YoY to INR5b with margin expanding 110bp YoY to 13.7%. While revenue and EBITDA were broadly in line, PAT beat our estimate due to higher other income and a lower tax rate. PAT was up 34% YoY to INR4b with PAT margin at 11%. Order inflow during the quarter stood at INR53b (+39% YoY), taking the total order book to INR171b (+61% YoY). For FY26, revenue/EBITDA/PAT grew 25%/25%/27% YoY to INR124b/INR16b/INR12b, and EBITDA margin remained broadly flat YoY at 13.1%. Meanwhile, OCF dipped 23% YoY to INR7b due to higher working capital requirements, while FCF turned negative at INR724m (vs. INR4.9b in FY25) due to higher capex during FY26.

Power systems segment growth to remain strong

The power systems segment delivered a strong FY26 performance with revenue growing 46% YoY to INR51b, while PBIT increased 68% YoY to INR11b, leading to a 290bp YoY margin expansion to 21.9%, driven by strong execution and operating leverage. Order inflow remained strong at INR112b (+69% YoY), taking the backlog to INR126b (+91% YoY), supported by strong demand across domestic utilities, exports, and data centers. To support future growth, the transformer capacity across the Gwalior and Bhopal plants has increased to ~65,000 MVA currently and is likely to rise to ~110,000 MVA by the end of CY26, with the commissioning of the new greenfield facility. The company has price variation clauses to pass on RM price hikes. We expect this division’s revenue to clock a 36% CAGR over FY26-28 with an EBIT margin of 22% for FY27/28.

Industrial systems: Margin pressure remains during the year

The industrial systems segment delivered a relatively muted FY26 performance, with revenue growing 6% YoY to INR67b. However, PBIT declined 16% YoY to INR6b, leading to a 230bp YoY contraction in PBIT margin to 9.3%. This was hurt by mix changes and competitive pricing in railways, along with higher material costs in motors. Order inflow declined ~8% YoY to INR64b, although management highlighted healthy traction in motors, railways, exports, and services. During the year, the company implemented cumulative price hikes of ~17.5% in motors to offset commodity inflation while maintaining market share, with further hikes dependent on commodity movements and pricing discipline. Commodity inflation remains a near-term risk; the impact is being mitigated through pricing actions, cost optimization, and productivity initiatives, and railway segment margins are expected to gradually improve through service growth and operational efficiencies. We expect the Industrial Systems segment to deliver a 6% revenue CAGR over FY26-28, with an EBIT margin at 9.5%/10% in FY27/FY28.

Steady progress in the semiconductor business

The semiconductor business continued to make steady progress in FY26, with CG Semi’s G1 OSAT facility now operational with a peak capacity of ~0.5m units per day, while the G2 facility for 14.5m units per day would be completed by the end of CY26. On the design side, Axiro strengthened capabilities through the integration of the RF business acquired from Renesas, which contributed ~USD65m revenue during FY26, while management also indicated further investments in semiconductor design and AI capabilities. We expect the semiconductor business to achieve EBITDA breakeven from FY28 as operating leverage improves with scale-up.

Financial outlook

We marginally revise our estimates by 6%/5% for FY27/FY28 to bake in better margins in power systems and other BS details. We expect overall order inflows to register an 11% CAGR over FY26-28E, fueled by healthy demand for transformers and switchgear in the power systems segment across domestic and export markets. In the Industrial segment, inflows will be supported by expansion in motors and railways. We model a revenue CAGR of 25% over FY26-28E and an EBITDA margin of 13.9%/15.1% for FY27/FY28, resulting in a PAT CAGR of 32% over the same period.

Valuation and view

The stock is currently trading at 81.3x/60.7x P/E on FY27E/FY28E EPS. We roll forward our SoTP-based TP to Jun’28 and reiterate our BUY rating with a TP of INR940. We ascribe a 58x multiple for the power systems business, which bakes in the upcoming large capacity in the power systems segment and also some discount to MNC players. We ascribe a 55x multiple to industrial systems, which is at 10% discount to ABB, and we ascribe value to the OSAT business via DCF to capture the benefits that will start accruing from FY28.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041