Buy UltraTech Cement Ltd for the Target Rs.13,800 by Motilal Oswal Financial Services Ltd

Cost efficiency drives EBITDA beat; growth story intact

Cost headwinds manageable; leverage comfortable to support growth

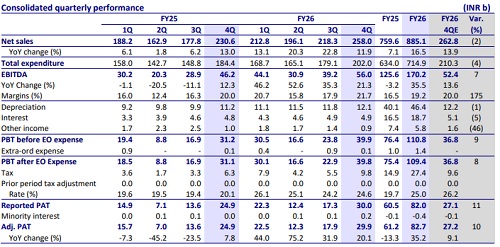

* UltraTech Cement’s (UTCEM) 4QFY26 EBITDA was above our estimate, led by lower opex/t. Consol. EBITDA increased ~21% YoY to INR56.0b (7% beat). EBITDA/t grew ~11% YoY to INR1,253 (est. INR1,148). OPM surged 1.7pp YoY to ~22% (1.8pp above estimate). Adjusted PAT grew ~20% YoY to INR29.9b (~10% beat).

* Management indicated that near-term cost pressures (high fuel, packaging, logistics costs) amid West Asia crises are manageable with mitigation levers such as fuel mix optimization, supplier diversification and benefits from long-term contracts for input materials. The company’s cost efficiency initiatives yielded cumulative cost benefits of ~INR185/t in FY25-26, and further gains are expected going ahead. The integration of acquired assets (ICEM and Kesoram) has been completed ahead of schedule, with full brand migration done in Mar’26. Capex is pegged at INR80-100b annually for capacity expansion over the next few years. The balance sheet remains strong, with a net debt-to-EBITDA ratio at <1.0x on a consolidated basis.

* We increase our FY27/FY28 EBITDA estimates by ~5% each, considering better cost efficiencies and integration benefits of acquired assets. Our EPS estimates are raised by ~9%/8% for FY27/28. We value UTCEM at 18x FY28E EV/EBITDA to arrive at a TP of INR13,800. Reiterate BUY.

Sales volume up ~9% YoY; realization rises ~3% YoY to INR5,770

* Consol. revenue/EBITDA/adj. PAT stood at INR258.0b/INR56.0b/INR29.9b (+12%/+21%/+20% YoY and -2%/+7%/+10% vs. our estimates). Sales volume grew ~9% YoY to 44.7mt (-2% vs. estimate). RMC revenue increased ~24% (+13% vs. estimate) and white cement revenue grew ~15% YoY (+26% vs. estimate). Other operating income/t stood at INR74 vs. INR67/INR83 in 4QFY25/3QFY26.

* Blended realization increased ~3% YoY/QoQ (each). Grey cement realization was flat YoY (up ~2% QoQ). Opex/t remained flat YoY (-2% QoQ; ~2% below estimate). Variable/other expenses/staff cost per ton rose ~1% YoY (each), while freight cost/t remained flat YoY. EBITDA/t increased ~11% YoY to INR1,253. Depreciation/interest costs rose ~7%/3% YoY, while other income declined ~14% YoY. ETR was 24.6% vs. 20.1%/24.2% in 4QFY25/3QFY26.

* In FY26, revenue/EBITDA/adj. PAT stood at INR885.1b/INR170.2b/ INR82.7b (up 17%/36%/35% YoY). EBITDA/t grew ~18% YoY to INR1,103. OPM surged 2.7pp YoY to ~19%. In FY26 OCF stood at INR153.2b vs. INR106.7b in FY25. Capex stood at INR96.8b vs. INR91.3b in FY25, while FCF stood at INR56.4b vs. INR15.4b in FY25.

Highlights from the management commentary

* The company crossed 200mtpa of domestic grey cement capacity, which is the largest in any country, excl. China. It plans to add ~37mtpa capacities in a phased manner to reach ~240mtpa by FY28E. ? Industry volume growth during 4QFY26/FY26 was 6-7%/6.5% YoY and is expected to be at 7-8% in FY27 too, led by infrastructure growth, growing rural demand and PMAY allocation. ? Lead distance stood at 367km in 4Q (down 18km YoY/up 4km QoQ) and 367km in FY26. The green power mix stood at ~43% in 4QFY26 vs. 35.7%/42.1% in 4QFY25/3QFY26 and targets ~85% by FY30.

Valuation and view

* UTCEM’s 4Q performance was ahead of our estimates, mainly driven by better cost savings. The company believes cost headwinds due to the West Asia conflicts are manageable in the near term with multiple levers and partially through the price hike taken so far. We estimate a CAGR of 13%/15%/18% in consolidated revenue/EBITDA/PAT over FY26-28. We estimate its consolidated volume CAGR at ~10% and EBITDA/t of INR1,136/INR1,216 in FY27E/FY28E vs. INR1,103 in FY26. OPM is estimated to expand 80bp to ~20% by FY28 (vs. ~19% in FY26).

* We estimate its net debt at INR178.4b in FY27 (to be peaked out) vs. INR146.9b in FY26. The net debt-to-EBITDA ratio is estimated to remain below 1.0x. We estimate its RoE/RoCE to increase to ~14%/12% by FY28 from ~11%/10% in FY26, backed by a rise in profitability and lower cost for ongoing expansions.

* The stock is currently trading at 19x/16x FY27E/FY28E EV/EBITDA. We value UTCEM at 18x FY28E EV/EBITDA to arrive at a TP of INR13,800. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412