Neutral Bajaj Housing Finance Ltd for the Target Rs. 100 by Motilal Oswal Financial Services Ltd

Higher NIM contraction; competitive intensity still elevated

Earnings in line; asset quality robust

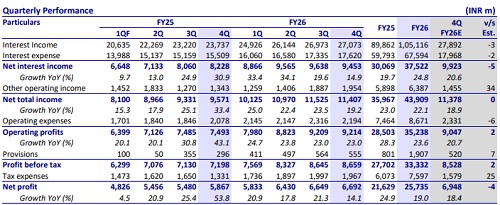

* Bajaj Housing’s (BHFL) 4QFY26 PAT grew 14% YoY to ~INR6.7b (in line). FY26 PAT grew ~19% YoY to INR25.7b. NII in 4QFY26 grew 15% YoY to ~INR9.5b (~5% miss). Other income grew 46% YoY to ~INR2b (~34% beat). NTI grew ~19% YoY to INR11.4b (in line).

* Opex rose ~6% YoY to INR2.2b (~6% lower than est.), and PPoP grew 23% YoY to INR9.2b (in line). FY26 PPoP grew ~24% YoY to ~INR35.2b.

* Net credit costs stood at INR555m (7% higher than est.), which translated into annualized credit cost of ~18bp (PQ: ~20bp and PY: ~12bp). Reported RoA/RoE in 4QFY26 stood at ~2.3%/12.2%.

* BHFL continues to pursue an aggressive but calibrated growth strategy, with a clear intent to sustain expansion at roughly twice the industry pace. The growth momentum is expected to be increasingly led by non-HL segments, which are scaling faster than traditional home loans due to their higher return profile and greater portfolio flexibility via sell-down opportunities.

* The company is sharpening its focus on both near-prime housing and the affordable housing segment under the Sambhav initiative, which is steadily scaling and is expected to reach meaningful disbursement run-rate over the next year. While home loan growth may remain relatively moderate due to elevated balance transfers, total AUM growth will be supported through diversification across product lines and active portfolio management.

* Margins are expected to remain stable in the near term but may gradually moderate since the disbursement yields are lower than portfolio yields. Mild yield compression is likely in early FY27 due to the competitive pricing and a higher proportion of home loans and LRD. CoF remains well managed, supported by a diversified borrowing base, though some upward pressure cannot be ruled out depending on money market interest rates.

* Management highlighted that the operating environment remains highly competitive, with strong participation from PSU banks and large private lenders, leading to persistent pricing pressure across segments. Banks continue to remain the pricing setter in mortgages, and BT-Outs continue to remain structurally high (~10%) despite a stable policy rate environment.

* We continue to believe in management’s ability to drive profitability improvement, supported by a healthy AUM CAGR of 22% over FY26-28E, broadly steady NIMs, and benign credit costs. We expect BHFL to deliver strong AUM growth, but rising competition from PSU banks and higher BTOUTs may push BHFL to cut its lending rates, which could exert pressure on NTI. We estimate BHFL to post a CAGR of 22%/21% in AUM/PAT over FY26- 28E and RoA/RoE of ~2.2%/14% in FY28E. Reiterate Neutral with a TP of INR100 (based on 2.8x FY28E BVPS).

Yield compression drives moderation in spreads despite stable CoF

* Reported yields declined ~20bp QoQ to ~8.9%, and CoB remained stable at ~7.3%, leading to ~10bp QoQ decline in spreads to ~1.7%.

* Reported NIM in 4QFY26 declined ~20bp QoQ to ~3.8%.

* Overall spreads are being influenced by two offsetting forces, declining acquisition yields in certain segments and efficiency gains from strong fee and assignment income, which have helped cushion margin contraction more than initially anticipated. We expect BHFL to deliver an NIM of ~3.2% in FY27/28E.

Strong AUM momentum led by broad-based growth

* AUM grew 23% YoY to ~INR1.4t, while 4QFY26 disbursements grew ~23% YoY to ~INR175b. Within the housing finance strategy, the Sambhav affordable housing portfolio has reached ~INR50b in AUM and is currently seeing steady disbursements of ~INR4.1-4.25b per month, with management targeting ~INR6b monthly run-rate over the next 12 months.

* We expect BHFL to deliver an AUM CAGR of ~22% over FY26-28.

Stable asset quality with a conservative provisioning buffer

* Asset quality was largely stable with GS3/NS3 at 0.3%/0.1%. PCR rose ~1pp QoQ to ~59.8%. (PQ: ~58.8%). Early delinquency indicators, including bounce rates, are showing a consistent improvement, indicating improving borrower behavior across segments. Importantly, no micro-level stress has been observed across any portfolio, and trends, including recent monthly data, remain stable.

* As a prudent measure, Stage 2 PCR has been increased despite the absence of any specific stress triggers, reflecting a conservative stance considering broader macro uncertainty. Overall, asset quality remains stable, well-controlled, and resilient across cycles. We model credit costs of ~13bp/~16bp for FY27/FY28E.

Highlights from the management commentary

? Incremental yields remain competitive, with home loans at ~8.5-8.6%, LAP at ~9%, and developer finance at ~11.75%.

? The branch network expanded to 226 branches across 182 locations, supporting growth and distribution reach.

Valuation and view

* BHFL is a strong franchise, well-positioned to navigate rising competition and a declining interest rate environment while maintaining healthy growth and profitability. However, the company continues to face increasing competitive pressure from banks, which are leading the pricing across product segments. This may result in some near-term margin contraction as BHFL prioritizes growth and market share.

* Given these dynamics, the current valuation of 3x FY27E already reflects its medium-term growth and profitability potential. We reiterate a Neutral rating on the stock with a TP of INR 100 (based on 2.8x FY28E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412