Sell Cyient Ltd For Target Rs. 830 by Motilal Oswal Financial Services Ltd

Stability emerging; growth still uneven Margin expansion remains a work in progress

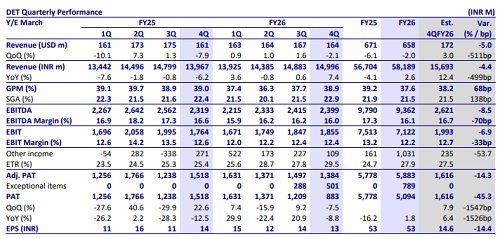

* Cyient’s (CYL) DET business reported 4QFY26 revenue of USD163m, down 2.4% QoQ in constant currency (CC) terms, below our estimate of 2.1% growth. Transportation & Mobility grew 4.5% QoQ CC, while Network & Infrastructure/Strategic Units down 3.6%/12.4 QoQ CC. Adj. EBIT margin of DET business at 12.4% missed our estimate of 12.7%. DET Adj. PAT was down 7.6% QoQ/9.1% YoY at INR1,382m (est. INR1,616m). The board approved a buyback plan worth INR7.2b or 6.4m equity shares each at a price of INR1,125 (representing 5.76% of total paid-up equity share capital).

* For FY26, DET revenue/adj. PAT grew 2.6%/1.8% YoY, while adj. EBIT fell 5.2% YoY. In 1QFY27, we expect revenue/EBIT to grew 8.8%/13.3% and adj. PAT to decline by 9.3% YoY. Free cash flow stood at 124.3% of net profit in FY26. FY26 RoE was 9% (vs. 12.1%/18.3%/17.5% in FY25/FY24/FY23). We reiterate our Sell rating with our SoTP-based TP of INR830, implying an 11% potential downside.

Our view: Recovery to be remain back-ended in FY27

* Stabilization visible, but recovery still back-ended: DET revenue declined ~2.4% QoQ CC in 4Q, impacted by delays at three large customers and West Asia energy deal pushouts. Management attributes this to timing rather than demand weakness with order intake improving in 2H (4Q +23% YoY). While this suggests the business may be nearing a floor, near-term growth remains dependent on deal conversion and ramp-ups. We believe 1QFY27 could also remain soft, with growth improving gradually through the year. We estimate DET revenue growth of 0.3%/4.3% YoY CC in FY27/FY28.

* Order book strong, but conversion remains key monitorable: Large deal pipeline is at a record high, with strong traction in connectivity and healthcare. Order book visibility remains reasonable, with ~75% of converted orders typically executed within nine months. However, recent delays (energy, connectivity) highlight that conversion timelines can be uneven. We believe the pace of closures and execution of large deals will be critical to sustaining growth over the next few quarters.

* Margins to improve, but path remains gradual: DET EBIT margin was stable at 12.4% in 4Q, with FY26 margins at 12.2% (down 70bp YoY). Management has guided for ~15% EBIT margin by 4QFY27, driven by revenue recovery, AI-led productivity (20-30% gains in select areas), and pricing actions. However, near-term margins may remain range-bound given continued investments and weak utilization in parts of the portfolio. We estimate EBIT margins of 13.5% by 4QFY27.

* Vertical trends mixed; T&M provides stability: Transportation & Mobility remains the most stable segment, growing ~4.5% QoQ and ~13.2% YoY in FY26, supported by aerospace MRO and aftermarket demand. Networks & Infrastructure declined (~3.6% QoQ), impacted by delayed project starts, though fiber and autonomous network investments provide medium-term visibility. Strategic Units remained weak (-12% QoQ), with recovery dependent on normalization in West Asia energy business. Overall, vertical performance suggests selective strength rather than broad-based recovery at this stage.

Valuation and changes to our estimates

* We maintain our Sell rating on Cyient, as recovery remains back-ended. With 1QFY27 likely to remain soft and visibility on execution still evolving, we believe near-term earnings upgrade risk is limited. We cut our FY27/FY28 estimates by ~2.7%/1.8% to reflect current trends, but do not see a meaningful change to the overall growth trajectory at this stage.

* Based on SoTP, we continue to value the company conservatively given execution risks. We value the DET business at 12x FY28E EPS, factoring in gradual margin improvement (to ~13.5% by FY27) and modest growth outlook. We continue to assign a ~20% holding company discount to the DLM stake. Our SoTP-based TP of INR830 implies an 11% downside.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412