Buy CEAT Ltd for the Target Rs 4,228 by Motilal Oswal Financial Services Ltd

Spurt in costs to test the industry’s pricing discipline

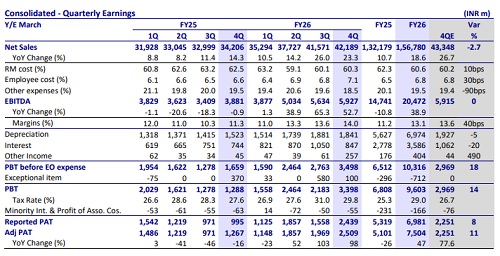

* CEAT’s 4QFY26 adjusted PAT was higher than our estimate at INR2.5b, largely on account of higher other income, even as operational performance was in line with our estimates.

* The GST rate cut has helped boost tyre demand, both in replacement and OEM segments. However, the recent surge in input costs is likely to drive near-term margin pressure, as the industry will need a couple of quarters to pass on the entire impact. Further, while the recent Camso acquisition is likely to take time to normalize, we remain positive on the long-term benefits that this acquisition can deliver for the group. Hence, we reiterate our BUY rating with a TP of INR4,228 (based on ~18x FY28E EPS).

PAT beat estimates on higher other income

* Net sales grew 23.3% YoY to INR42b (largely in line with our estimates) in 4QFY26, aided by healthy YoY volume growth across all segments and slightly better realizations. The management expects the growth momentum to continue going forward.

* FY26 product mix: Truck/bus 29%, 2/3Ws 27%, PV 22%, OHT 15%, and Others 7%.

* FY26 market mix: Replacement 51%, OEM 30%, and Exports 19%.

* Gross margin has remained stable QoQ at 39.7% due to a stable RM basket.

* EBITDA margin improved 270bp YoY (+50bp QoQ) at 14%, above our estimate of 13.6%. Margin improvement is led by operating leverage benefits.

* EBITDA was up 53% YoY to INR5.9b (in-line with estimates).

* Other income was higher than expected at INR257m (our est. at INR44m).

* The company incurred a one-time extraordinary expense of INR100m as compensation for employees opting for VRS.

* Adjusted for this, PAT grew 98% YoY to INR2.5b, ahead of our est. of INR2.25b.

* 4Q capex was INR4b, while net working capital increased INR1b QoQ.

* Gross debt increased QoQ by INR800m to INR30b.

* FY26 performance: Revenues grew 19% to INR156b, while margins expanded 190bp YoY to 13.1%. PAT grew 47% to INR7.5b.

* OCF generation stood at INR17.8b, while FCF was negative INR4.8b (on account of Camso acquisition).

Highlights from the management commentary

* The current demand continues to be healthy across all segments. However, given the sharp input cost inflation that is likely to be passed on soon and the ongoing West Asia conflict, demand is likely to moderate in the coming months, especially for the CV segment.

* Replacement demand for TBR in FY27 is expected to grow in the single digit, driven by economic activity, positive seasonality, and an aging fleet. PCR replacement is likely to grow 3-5%. Even the scooters segment is expected to witness high single-digit growth in FY27.

* In the OE segment, the MHCV segment continues to experience strong double-digit growth, and PV is expected to witness healthy single-digit growth coming largely from the SUV and MPV segments. LCV growth is also likely to remain strong.

* In international business, the company expects demand recovery in multiple segments, especially in the MHCV in the US and the EU. PV demand in the EU is also recovering for CEAT. The Middle East accounts for 15% of CEAT’s exports, and this business is affected due to the ongoing tensions in the region.

* Raw material prices in 4Q remained stable QoQ, but they are likely to increase by ~15–20% QoQ in 1QFY27. They need an almost 10% price increase in the replacement market to pass on this impact. So far, they have been able to take a 5% price hike by the end of Apr’26 and may require another 5% increase over May and Jun. However, the subsequent price hikes would be dependent on competitive dynamics.

Valuation and view

The GST rate cut has helped boost tyre demand, both in replacement and OEM segments. However, the recent surge in input costs is likely to drive near-term margin pressure, as the industry will need a couple of quarters to pass on the entire impact. Further, while the recent Camso acquisition is expected to take time to normalize, we remain positive on the long-term benefits that this acquisition can deliver for the group. Hence, we reiterate our BUY rating on the stock with a TP of INR4,228 (based on ~18x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412