Buy Bharti Airtel Ltd for the Target Rs.2,180 by Motilal Oswal Financial Services Ltd

Muted 4Q; robust FCF generation aids significant deleveraging in FY26

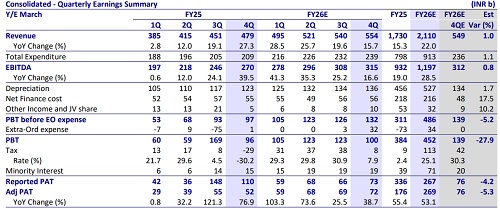

* Bharti Airtel (Bharti) reported a muted performance in 4QFY26, with consolidated EBITDA rising 2.3% QoQ. The India performance (EBITDA +1.2% QoQ) was broadly in line, while Airtel Africa (AAF, +8% QoQ, 6% ahead) continued its strong display, benefitting from higher margins in Nigeria and favorable currency movements.

* India wireless revenue and EBITDA grew less than 1% QoQ, due to two fewer days QoQ, while Homes continued on a high growth path.

* Consolidated capex surged ~36% QoQ to INR161b (~12% YoY), with India capex (excl. Indus) rising ~54% QoQ to INR112b. FY26 capex for India (excl. Indus) at INR310b was marginally higher than FY25 (INR303b, vs. management’s guidance of YoY moderation). Management expects FY27 capex in India to remain in the same ballpark as FY26 capex.

* 4Q consolidated FCF moderated to INR84b (vs. ~INR169b in 3Q), due to seasonal working capital build-up and AGR payments. However, FY26 FCF (after leases and interest) improved sharply to INR542b (vs. INR389b YoY).

* Driven by robust FCF generation and a recent rights issue (INR157b), Bharti’s consolidated net debt (ex-lease) declined ~INR214b QoQ to INR910b (down ~INR475b YoY), with leverage moderating to 0.84x (vs. ~1.5x YoY).

* The Board approved issuance of ~147m shares (at ~INR1,923/share) to the promoter, ICIL (part of Bharti Enterprises), in lieu of its ~16.3% stake in AAF (at GBP3.67/share). The transaction avoids ~INR282b cash outgo, but will lead to ~2.4% equity dilution (the deal is EPS accretive on FY26 earnings).

* The most pertinent investor concern about Bharti has been its capital allocation plans. However, we believe the concerns are overdone. We view the AAF stake purchase from promoters as positive and expect the NBFC foray to be calibrated. We believe any further international acquisition (except AAF) could be the most concerning aspect of Bharti’s capital allocation policy.

* We tweak our estimates for FY26 actuals and build in ~2.4% equity dilution to account for ~16.3% AAF stake purchase.

* We model a CAGR of ~15% in Bharti’s consol. revenue/EBITDA over FY26-28E, driven by

1) flow-through of the ~15% tariff hike in India wireless from 2QFY27

2) continued acceleration in Home broadband net adds

3) strong double-digit CC growth in Africa

4) steady growth in Enterprise offerings.

* We reiterate our BUY rating on the stock with an SoTP-based revised TP of INR2,180. The India wireless and home businesses are valued at a DCFimplied ~12x FY28 EV/EBITDA. Risk-reward remains favorable (bull case: INR2,645; bear case: INR1,715).

Valuation and view

* The most pertinent investor concern about Bharti has been its capital allocation plans. However, we believe the concerns are overdone. We view the AAF stake purchase from promoters as a positive, given the long-term growth opportunity. Further, the outlay on the NBFC foray would be measured and less than Bharti’s one-quarter FCF to be invested over 5-7 years. However, any further international acquisition (except AAF) could be the most concerning development.

* We continue to like Bharti in the telecom space, given robust FCF generation and an improving return ratio. With a potential tariff hike and range-bound core capex, Bharti could deliver ~INR1.3t+ FCF over FY26-28, with the company turning net cash by FY29 and return ratios climbing to ~25% by FY28.

* We model a CAGR of ~15% in Bharti’s consolidated revenue/EBITDA over FY26- 28E, driven by

1) flow-through of the ~15% tariff hike in India wireless from 2QFY27

2) continued acceleration in Home broadband net adds

3) strong double-digit CC growth in Africa

4) steady growth in Enterprise offerings.

* We reiterate our BUY rating with an SoTP-based revised TP of INR2,180 (earlier INR2,205, albeit on a higher share count). We value the India wireless and homes business on DCF (implies ~12x Mar’28E EV/EBITDA), DTH/Enterprise at 5x/10x Mar’28E EBITDA, and Bharti’s stake in Indus Towers and Airtel Africa at a 25% discount to our TP/CMP.

* Impending tariff hikes and the upcoming JPL IPO remain the key near-term triggers. The long-term risk-reward remains attractive (bull case: INR2,645; bear case: INR1,715).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412