Buy Power Finance Corporation Ltd for the Target Rs.525 by Motilal Oswal Financial Services Ltd

Muted loan growth; pressure on yields weighs on NIM Earnings beat driven by provision write-backs from stressed asset resolutions

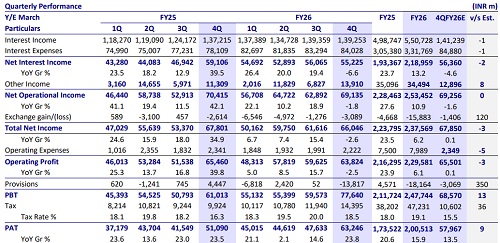

* PFC’s 4QFY26 PAT grew ~24% YoY to INR63.2b (~9% beat). FY26 PAT grew 16% YoY to INR201b (PQ: INR174b). NII declined ~7% YoY to ~INR55.2b (in line). Other operating income grew ~23% YoY to ~INR13.9b, including dividend income of ~INR11.8b.

* PFC reported exchange losses of INR3.1b (PQ: exchange loss of INR1.3b). Opex declined ~5% YoY to ~INR2.2b (~5% lower than est.). PPoP declined ~3% YoY to INR63.8b (in line). FY26 PPOP grew ~6% YoY to INR230b.

* Provisions write-backs stood at INR13.8b in 4Q (PQ: INR52m; PY: INR4.4b). This translated into credit costs of -25bp in 4QFY26 (PY: 8bp).

* Reported yields stood at ~9.96%, while CoB rose ~8bp QoQ to ~7.5%, resulting in spreads of ~2.45% for FY26. Reported NIM for FY26 declined ~10bp to ~3.55% (9MFY26: 3.65%).

* Management guided for loan growth of ~10% in FY27. PFC indicated that FY26 loan growth remained below earlier guidance of 10-11% primarily due to high prepayments and refinancing activity. However, PFC expects prepayments to moderate going forward as the interest rate cut cycle is now behind. We also model loan CAGR of ~10% over FY26-FY28E.

* Management highlighted that while lower domestic interest rates supported funding costs, heightened volatility in forex markets led to an increase in overseas borrowing costs. Given the continued uncertainty in forex markets and high competition weighing on yields, the company guided for spreads of 2.4-2.5% in FY27 (FY26: 2.45%).

* We estimate a CAGR of 9%/10%/5% in disbursement/advances/PAT over FY26-28, with RoA/RoE of 3.2%/18% and a dividend yield of ~4.5% in FY28. We maintain our BUY rating with an SoTP (Mar’28E)-based TP of INR525.

PFC-REC merger expected to be effective in Apr’27, subject to approvals

* The proposed merger of PFC and REC is being positioned as a transformational step aimed at creating a larger and strategically stronger institution for India’s power and infrastructure financing ecosystem, with enhanced scale, financing capabilities, and operational efficiency.

* The boards of both entities have already granted in-principle approval for the merger and appointed legal, transaction, valuation, and merchant banking advisors. The merger is expected to be effective from 1 st Apr’27, subject to regulatory and government approvals. The endeavor is retain its government company status despite the likelihood of govt. shareholding falling below 50% (with a simple share swap).

Valuation and view

* PFC delivered an operationally weak quarter. While the earnings beat was driven by provision write-backs, loan growth remained muted at <2% QoQ. Asset quality continued to improve, aided by the resolution of Sinnar thermal and TRN Energy, which resulted in provision write-backs. NIMs declined due to yield compression driven by competitive pressure from banks and higher incremental borrowing costs from volatility in forex markets.

* While the company has indicated that the proposed merger could become effective from 1st Apr’27, we are not factoring the same into our estimates at this stage given the limited clarity on the overall structure, execution roadmap, and potential financial implications. Further, the merger remains subject to multiple regulatory, governmental, and shareholder approvals, and hence we believe it is premature to build in any merger-related synergies, balance sheet benefits, or operational changes into our projections at this point.

* PFC (standalone) trades at 1.1x FY27E P/BV and ~6x FY27 P/E, which we view as attractive, and we therefore maintain our BUY rating with an SoTP (Mar’28E)- based TP of INR525 (premised on a 1.1x target multiple for the PFC standalone business and INR148/sh for PFC’s stake in REC after a holdco discount of 20%).

Key risks:

1) weaker loan growth driven by higher prepayments

2) an increase in exposure to power projects without PPAs

3) compression in spreads and margins due to an aggressive competitive landscape

4) any slowdown in the offtake of renewable energy projects.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412