Buy TVS Motor Company Ltd for the Target Rs.4,267 by Motilal Oswal Financial Services Ltd

Margins stable despite cost pressures Continued outperformance to support premium valuation

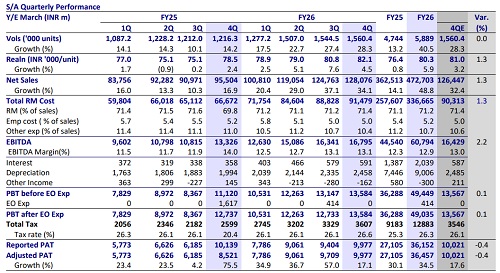

* TVS Motor Company (TVS)’s 4QFY26 PAT stood at INR10b, in line with our estimates. EBITDA margin remained stable QoQ at 13.1% (in line) despite the sharp rise in input costs, as cost headwinds were offset by improved mix and favorable currency benefits.

* Overall, we factor in a revenue/EBITDA/PAT CAGR of 16%/19%/21% over FY26-28E. TVS’s consistent market share gains across key domestic and export segments, along with a gradual improvement in margins, have driven healthy returns over the years. We expect this outperformance to continue over our forecast period, given its healthy new launch pipeline. This sustained outperformance is likely to help sustain its premium valuations in the long run. We reiterate our BUY rating and value the stock at 35x FY28E EPS to arrive at our TP of INR4,267.

Earnings in line

* TVS’s 4QFY26 PAT came in at ~INR10b, in line with our estimate.

* TVS posted its highest-ever quarterly sales of 1.56m units this quarter, up 28.3% YoY. Motorcycle volumes were up 23% YoY, Scooters rose 32%, and 3W volumes were up 65% YoY. Despite supply constraints of the rare earth magnet, the EV business recorded a 51% growth YoY, registering quarterly sales of 115k units.

* Revenues came in line with estimates at INR128.1b, up ~34% YoY.

* Realizations were up 4.5% YoY at INR82.1k per unit.

* EBITDA margin remained stable QoQ at 13.1% (in line) despite the spike in input costs, as cost headwinds were offset by improved mix and favorable currency benefits.

* EBITDA grew 26% YoY to INR16.8b, broadly in line with our estimate.

* Other income was below our estimate, as it included a loss on the fair valuation of an investment of INR527m made by TVS.

* Overall, PAT came in line at INR10b, up 17% YoY.

* The Board declared an interim dividend of INR12 per equity share. Further, the company had also allotted four fully paid bonus non-convertible redeemable preference shares for every equity share held (amounting to INR19b), with a maturity date of 1 st Sep’26.

* TVS’s FY26 revenue/EBITDA/adj. PAT stood at INR473b/INR60.8b/INR36.5b, having grown by 49%/36.5%/34.5% YoY.

* The CFO for the year came in at INR57.3b, with the company being free cash positive with INR38.1b. The RoE and RoCE for the year stood at 34.4% and 39.5%, respectively.

Valuation and view

Overall, we factor in a revenue/EBITDA/PAT CAGR of 16%/19%/21% over FY26-28E. TVS’s consistent market share gains across key domestic and export segments, along with a gradual improvement in margins, have driven healthy returns over the years. We expect this outperformance to continue over our forecast period, given its healthy new launch pipeline. This sustained outperformance is likely to help sustain its premium valuations in the long run. We reiterate our BUY rating and value the stock at 35x FY28E EPS to arrive at our TP of INR4,267.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)