Buy State Bank of India Ltd for the Target Rs.1,300 by Motilal Oswal Financial Services Ltd

Business growth robust; RoA outlook steady at >1% Margins decline 17bp QoQ - guidance unchanged

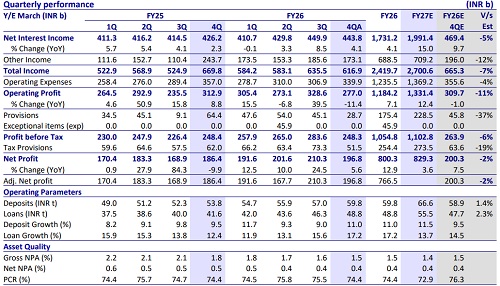

* State Bank of India (SBIN) reported 4QFY26 PAT of INR196.8b (up 5.6% YoY/ down 6.4% QoQ, in line), affected by a sharp NIM contraction and treasury losses.

* NII grew 4% YoY/fell 1% QoQ to INR443.8b (5% miss). NIMs fell 17bp QoQ to 2.81%, impacted by repo rate transmission, MCLR cuts, and select large corporates shifting toward T-bill linked rate. Management indicated that corrective measures are already underway and guided for domestic NIMs of 3%+ in FY27.

* Loan book grew 17.2% YoY/5.4% QoQ, while deposits grew 11% YoY/4.8% QoQ. SBIN is confident of growing its loan book at 13-15% in FY27.

* Fresh slippages inched up to INR55.5b from INR48.6b in 3QFY26. GNPA/NNPA ratios were up 8bp/flat QoQ at 1.49%/0.39%. PCR ratio moderated to 74.4%.

* We cut our earnings estimates by 3%/5% for FY27/FY28 and expect FY27E RoA/RoE at 1%/15.3%. Reiterate BUY with a TP of INR1,300 (1.4x Sep’27E ABV + INR351 for subs).

Advances growth guided at 13-15%; asset quality robust

* SBIN reported 4Q PAT of INR196.8b (up 5.6% YoY, 2% miss) amid tepid NII and treasury losses. However, this was partly offset by lower provisions.

* NII grew 4% YoY/fell 1% QoQ to INR443.8b (5% miss). NIM declined 17bp QoQ to 2.81%. SBIN expects FY27 domestic NIMs to recover to 3%+, with course correction already in play.

* Other income declined by 29% YoY/7% QoQ to INR173.1 (12% miss) amid treasury loss of INR14.7b (vs. profit of INR32.8b in 3QFY26). Total revenue declined 8% YoY/3% QoQ to INR616.9b.

* Opex declined 5% YoY/rose 11% QoQ to INR339.9b (4% lower vs. MOFSLe). PPoP declined 11% YoY/16% QoQ to INR277b (11% miss). C/I ratio thus increased to 55.1% vs. 48.3%. The bank expects the C/I ratio to be maintained below 50% levels.

* Advances grew by 17.2% YoY/5.4% QoQ, of which retail grew by 15.2% YoY/4.3% QoQ, agri grew 19.7% YoY/6.4% QoQ, and corporate grew 14.8% YoY/6.8% QoQ. Xpress credit rose 7.4% YoY/2.9% QoQ, while gold loan grew faster at 111.5% YoY/ 23.1% QoQ.

* Provisions came in lower at INR28.7b (down 55.4% YoY/36.3% QoQ; 37% below estimate). Deposits grew 11% YoY/4.8% QoQ. CASA ratio improved by 33bp QoQ to 39.5%. CD ratio increased to 81.6% vs. 81.2% in 3QFY26.

* Fresh slippages increased to INR55.48b in 4Q (vs. INR48.6b in 3QFY26). GNPA/NNPA ratios were up 8bp/flat QoQ at 1.57%/0.39%. PCR ratio moderated to 74.4%. Credit cost stood at 0.37% vs. 0.39% in 3Q, while SMA book stood at 7bp of loans (8bp in 3QFY26).

* Subsidiaries: SBICARD clocked a PAT of INR3.6b (down 33% YoY/35% QoQ). SBILIFE’s PAT grew by 39.3% QoQ/fell 1.1% YoY to INR8.04b. AMC business PAT grew 4.4% YoY/fell 22.6% QoQ to INR6.4b.

Valuation and view

SBIN reported a mixed quarter, affected by a decline in NII and NIM contraction due to repo rate transmission, MCLR cuts, and migration of select corporate loans from MCLR linked to T-bill. However, the bank aims to maintain domestic NIMs above 3% going ahead, supported by ongoing corrective measures and expected improvement in yields. Treasury profits were also weaker during the quarter amid a spike in bond yields. The bank continues to expect healthy credit growth and has guided for loan growth of 13-15% going forward. Asset quality remained resilient overall, although slippages were slightly higher in 4Q, reflecting the seasonality seen in all PSU banks. We trim our earnings estimates by 3%/5% for FY27/FY28, as we cut our NIM estimates, partly offset by low provisions. We estimate FY27 RoA/RoE at 1.0%/ 15.3%. Reiterate BUY with a TP of INR1,300 (1.4x Sep’27E ABV + INR351 for subs).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412