Buy ICICI Bank Ltd for the Target Rs.1750 by Motilal Oswal Financial Services Ltd

Well-positioned to sustain sector leadership Growth outlook healthy; asset quality robust

* ICICI Bank (ICICIBC) is well-positioned to sustain its growth momentum while maintaining profitability benchmarks. We expect the bank to deliver a 16% loan CAGR over FY26-FY28, led by strong growth in Business Banking and PL, while the corporate segment is also expected to witness healthy traction, supported by working capital demand.

* The liability franchise continues to remain best-in-class, supported by diversified acquisition engines and a rapidly expanding physical network. With a domestic CD ratio of 85.5% and LCR of ~126%, the bank is well placed to capitalize on growth opportunities compared to peers.

* ICICIBC is likely to maintain cost leadership despite meaningful investments in technology, customer delivery, analytics, and talent. We estimate the C/I ratio to range ~39%/38% over FY27/28, respectively.

* ICICIBC’s asset quality remains robust, supported by disciplined underwriting, continued monitoring, and strong recoveries, while the bank maintains a healthy contingency buffer (0.9% of loans). The bank currently does not face additional portfolio stress from the West Asia crisis or ECL transition. Credit costs are, thus, expected to remain contained, with GNPA/NNPA improving to ~1.4%/0.3% by FY28E.

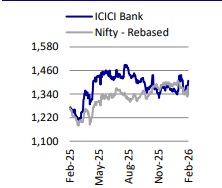

* The stock has delivered tepid performance over the past year, reflecting broader derating across large banking stocks amid persistent FII selling. However, with operating performance holding strong and sustained market share gains across key lending segments, we expect a gradual rerating.

* We build in FY28E RoA/RoE of 2.3%/16.2%. ICICIBC remains our top BUY within the banking sector, with a TP of INR1,750 (2.5x Sep’27E standalone ABV).

Broad-based growth; market share gains to continue

ICICIBC’s credit growth has witnessed improved traction in 2HFY26 following a relatively muted 1HFY26, with the bank reporting 15.8% YoY and 6% QoQ growth in 4QFY26. The domestic portfolio expanded at a healthy pace, supported by improved traction in secured retail segments and continued dominance in the business banking space (21% of the loan mix). The corporate sector is also gaining traction, enabling the bank to exercise better pricing power. Growth in the credit card book, KCC loans, and select auto loans segments remains muted. However, the personal loan segment has started witnessing improved traction over the past couple of quarters and is expected to sustain momentum. We estimate a 16% credit CAGR over FY26-28, with sustained traction in the business banking and SME segments, supported by recovery in corporate and personal loan growth.

Robust liability franchise; comfortable LDR and LCR position the bank for sustained growth

The bank continues to strengthen its liability franchise through diversified acquisition engines, including corporate salary accounts, transaction banking, digital channels, and an expanding physical network. While CASA accretion remains challenging industry-wide, ICICIBC continues to focus on building a sustainable retail deposit franchise rather than chasing rate-sensitive deposits. Deposit growth stood at 12% YoY in FY26, driven by a pickup in CA balances. The bank’s robust liquidity position, along with LCR at 126% and a controlled domestic C/D ratio of ~85.5%, provides sufficient flexibility to support healthy loan growth compared to peers. Over the medium term, strong customer engagement, deep ecosystem partnerships, and branch-led sourcing are expected to support sustained deposit momentum. We expect deposits growth to remain healthy at a 15% CAGR over FY26-28.

Valuations and view

* ICICIBC is well-positioned to sustain healthy operating performance, led by allround delivery across key metrics (loan growth, liabilities, margins, and asset quality).

* Growth is becoming increasingly broad-based, led by business banking, improvement in corporate and mortgage loan demand, and a gradual uptick in unsecured segments (mainly PL)

* Operating leverage remains a key lever to support the next leg of growth in earnings, backed by improved traction in fee income, superior digital capabilities, and continued network expansion.

* Asset quality remains a key strength, with low credit costs (~40-45bp throughcycle), strong provision buffers, and minimal impact expected on earnings due to the ECL transition and inflationary macro environment.

* With a disciplined, risk-calibrated approach and increasing focus on market share gains (currently ~7%), ICICIBC remains well-positioned to deliver consistent earnings compounding. We, thus, estimate the bank to deliver a PPoP/PAT CAGR of ~16%/15% over FY26-28, leading to an RoA/RoE of 2.3%/16.2%.

* ICICIBC remains our top BUY in the sector with a TP of INR1,750 (2.5x Sep’27E standalone ABV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412