Neutral Urban Company Ltd for the Target Rs.135 by Motilal Oswal Financial Services Ltd

Core accelerating; InstaHelp investments a key unknown Steady performance across business units; breakeven guidance for 3QFY28 maintained

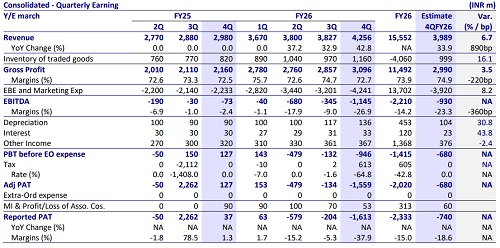

* Urban Company’s (URBANCO) consolidated NTV for 4QFY26 stood at INR11.5b, rising 42% YoY, above our estimate of 38% YoY.

* India consumer services NTV came at INR8.08b, growing 26% YoY vs. our estimate of 23.4% YoY. Native Business NTV came at INR890m, growing 67% YoY vs. our estimate of 70% YoY. InstaHelp NTV came at INR400m vs our estimate of INR504m.

* For India consumer services, adjusted EBITDA as a % of NTV margin contracted 230bp QoQ at 3.3% vs our estimate of 1.8%. For InstaHelp, adjusted EBITDA losses came at INR1.19b for 4QFY26 (vs our estimates of INR850m loss). Adj PAT loss came in at INR1,559m (est. loss of INR680m).

* For FY26, its revenue grew 35.9% YoY, while EBITDA loss increased to INR2,210m in FY26 (vs. INR320m in FY25). For FY26, Adj PAT loss increased to INR2,018m (30% YoY).

* While URBANCO remains well-positioned to benefit from the long-term formalization of home services, we believe current valuations already reflect much of the improvement in the core business. Continued investments and TAM uncertainty in InstaHelp, execution risks around penetration, and risk around habit formation keep the risk-reward balanced, in our view. Reiterate Neutral with a revised TP of INR135.

Our view: Supply densification and utilization gains aid core profitability

* Core India business accelerating on the back of supply densification; margins also expanding: India Consumer Services NTV growth accelerated to ~26% YoY in 4QFY26, the fastest in 11 quarters, driven by higher supply density across top cities, better professional utilization, and faster fulfilment times. Management indicated supply (not demand) remained the key constraint during the quarter, suggesting demand continues to remain healthy.

* Margins are also scaling alongside growth, with adjusted EBITDA margin expanding to ~3.3% of NTV in 4QFY26 vs ~1.6% last year. We believe the core business is now on a much stronger footing compared to FY24. We build in India Consumer Services NTV growth of ~22%/20% for FY27/28E.

* Losses in InstaHelp elevated and TAM unclear; key overhang in our view: InstaHelp scaled rapidly to ~2.7m orders in 4QFY26, but adjusted EBITDA losses remained elevated at ~INR1.19b. Management continues to prioritize market leadership, network density, and service quality over near-term profitability; it has guided for losses to remain elevated for the foreseeable future. While repeat rates and service quality trends appear encouraging, visibility on steady-state margins and TAM size remains limited, in our view.

* Native business scaling well; profitability now within sight: Native NTV grew ~67% YoY in 4QFY26, while adjusted EBITDA margins expanded materially from - 25.1% in FY25 to -8.9% in FY26, despite continued investments in new categories. Management indicated the core Native business is already nearing breakeven, with profitability expected over the next few quarters. We expect existing categories such as water purifiers and smart door locks to remain the key growth drivers, with service revenue gradually becoming a larger part of the mix over time.

* International business turning profitable earlier than expected: International NTV grew ~56% YoY in FY26, while turning adjusted EBITDA positive (~INR60m), driven by strong growth in the UAE and Singapore. Subscription-led cleaning models are driving more recurring revenue behavior, while competitive intensity also appears manageable. We estimate international business EBITDA margins at ~2.7%/4.7% in FY27/28.

* Guidance appears achievable, supported by core business execution: Management reiterated consolidated adjusted EBITDA breakeven by 3QFY28 and ~INR10b adjusted EBITDA target by FY31. While InstaHelp losses may remain elevated for longer, the core India business is now operating from a much stronger base, in our view. Consolidated adjusted EBITDA breakeven by 3QFY28 also remains management’s stated guidance, which we broadly build into our estimates. We expect consolidated adjusted EBITDA margins at -3.1%/- 0.4% for FY27/28E

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412