Neutral MCX Ltd for the Target Rs. 2,850 by Motilal Oswal Financial Services Ltd

Strong growth driven by new launches and higher participation

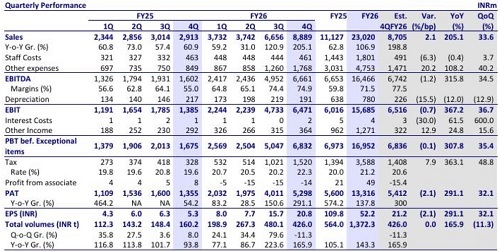

* MCX’s operating revenue came in at INR8.9b (in line), up 205% YoY/34% QoQ, led by healthy growth in bullion and energy contracts. For FY26, revenue jumped 107% YoY to INR23b.

* Opex grew 70% YoY/31% QoQ to INR2.2b, with staff costs flat YoY at INR461m and other expenses up 108% YoY at INR1.8b. 4Q EBITDA stood at INR6.7b, up ~4.2x YoY and ~1.3x QoQ. FY26 EBITDA stood at INR16.5b.

* The company reported PAT of ~INR5.3b, up 291% YoY/32% QoQ (in line). For FY26, PAT rose 138% YoY to INR13.3b.

* MCX continues to strengthen its product pipeline across metals, energy, and commodity indices, with focus on commodity index futures alongside options. New metal index products are expected in FY27.

* We have cut our EPS estimates for FY27/FY28 by 6%/4% to factor in current volume trends and higher costs. We expect revenue/EBITDA/PAT to clock a CAGR of 16%/15%/17% over FY26-28E. We reiterate a Neutral rating on the stock with a one-year TP of INR2,850 (premised on 40x FY28E EPS).

Volumes moderated sequentially, led by bullion contracts

* The transaction fee for 4QFY26 stood at ~INR8.1b, up 218% YoY/34% QoQ, comprising options and futures in the ratio of 70:30 (vs. 4QFY25 at INR2.5b in the ratio of 71:29).

* Overall ADT grew 168% YoY to INR6.7t, driven by 432% and 53% growth in bullion and energy contracts, respectively, though overall ADT declined 11% QoQ due to a 26% QoQ drop in bullion contracts.

* Options notional ADT grew 160% YoY to INR5.8t, though declined 14% QoQ due to a 30% drop in bullion contracts. Meanwhile, options premium ADT surged 223% YoY and 50% QoQ to ~INR106b, led by strong volume growth across segments.

* Futures ADT rose 230% YoY to INR902b, driven by 305%/66%/219%/26% /125% growth in bullion/energy/base metal/Agri/index contracts.

* MCX retained more than 99% market share in commodity futures in 4QFY26, with gold and silver contributing ~77% of futures turnover.

* Client participation rose 7% YoY to 583 members as of Mar’25, while traded clients reached 1.4m, with futures-to-options participation mix at 48%-42%.

* The number of UCCs as of 4QFY26 end stood at 46.5m vs. 24.8m in 4QFY25 and 40.3m in 3QFY26. This growth was driven by improved onboarding through digital brokers, better user experience, and integration improvements such as consolidated ledger systems.

* FPIs currently contribute ~2-3% of overall MCX ADT. Within the energy segment, FPIs account for a double-digit percentage contribution. Strong onboarding momentum continued with a healthy future pipeline.

* Product pipeline remains strong, with electricity derivatives seeing healthy traction, while MCX has received approval to set up a coal exchange subsidiary and awaits regulatory clarity on agri commodities.

* Other income at INR364m grew 25% YoY/16% QoQ (13% above estimate).

* Total expenses jumped 70% YoY/31% QoQ to INR2.2b, with CIR at 25.1% vs. 45% in 4QFY25 and 25.6% in 3QFY26.

* Staff costs remained flat YoY at INR461m, while other expenses were up 188% YoY at INR1.8b, including mainly computer tech costs/contribution to SGF/other expenses, rising 128%/214%/168% YoY to INR425m/INR619m/INR442m. Software charges declined 6% YoY to INR281m.

Valuation and view

* Bullion and energy drove incremental volume growth in FY26; however, elevated bullion volatility led to a sequential moderation from peak levels in 4Q. Going forward, commodity volumes are expected to normalize, with estimates assuming a 10% decline in FY27 futures volumes but strong 92%/40% growth in options notional/premium volumes.

* We have cut our EPS estimates for FY27/FY28 by 6%/4% to factor in current volume trends and higher costs. We expect revenue/EBITDA/PAT to clock a CAGR of 16%/15%/17% over FY26-28E. We reiterate a Neutral rating on the stock with a one-year TP of INR2,850 (premised on 40x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412