Neutral PB Fintech Ltd for the Target Rs. 1,870 by Motilal Oswal Financial Services Ltd

Gaining strength across segments

* We attended PB Fintech’s Analyst Day, where the top management provided insights into its strengths and future initiatives across key segments that it operates in. The broader story remains intact that the company will continue to gain market share across its key verticals. PB is well placed to achieve its guidance of INR10b of PAT in FY27 and INR1t of premium over the medium term.

* Over FY26-28, we expect PB to post a strong CAGR of 28%/40% in revenue/PAT. However, the potential risk of commission caps on take rates remains the key monitorable. We reiterate our Neutral stance with a TP of INR1,870 (based on DCF valuation), implying 53x FY28E EV/EBITDA

PB Fintech: Building India’s largest retail insurance distribution and services ecosystem

* PB Fintech has steadily evolved from being a digital insurance comparison platform into a much broader retail insurance ecosystem spanning customer acquisition, underwriting support, claims servicing, healthcare engagement, renewal monetization and financial planning.

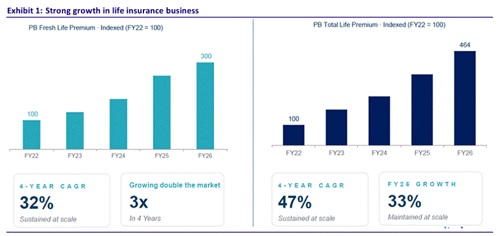

* PB continues to strengthen its positioning across life, health and motor insurance, while its earnings profile is gradually shifting from upfront acquisition-led growth toward renewals, customer retention and better portfolio quality.

* Strategy now appears increasingly centered around owning the customer relationship across the insurance lifecycle rather than simply generating leads for insurers. This is visible through investments in assisted distribution, claims support, healthcare ecosystems, AI-led customer engagement, co-created products and servicing infrastructure.

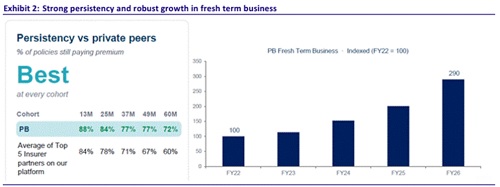

* Management remains confident of achieving its FY27 PAT target of INR10b. Importantly, the business is now being supported by structural drivers such as renewal revenue, stronger persistency, lower churn, cross-selling opportunities and improved portfolio quality, rather than relying only on fresh customer acquisition.

* PB is also using AI more as a growth enabler than purely as a cost optimization tool. The platform currently handles ~100m monthly customer interactions, while advisors reportedly make ~250 calls per day. AI is being deployed across verification calling, underwriting assistance, personalization, claims support and conversion optimization. Management's view is that the long-term winners in insurance AI are likely to be companies that can improve customer engagement and scale conversions rather than only reduce costs.

* Another important change has been PB's increasing focus on assisted and physical distribution despite being a digital-first platform. The company now has ~450k PB Partners, of which ~125k are active. Physical presence is helping improve conversion rates, ticket sizes, customer trust and persistency, particularly in savings and health products. 750 1,150 1,550 1,950 2,350 May-25 Aug-25 Nov-25 Feb-26 May-26 PB Fintech. Nifty - Rebased Investors are advised to refer through important disclosures made at the last page of the Research Report. Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital. Research Analyst: Prayesh Jain (Prayesh.Jain@MotilalOswal.com)/ Nitin Aggarwal (Nitin.Aggarwal@MotilalOswal.com) Research Analyst: Kartikeya Mohata (Kartikeya.Mohata@MotilalOswal.com) Muskan Chopra (Muskan.Chopra@MotilalOswal.com

* Renewals are now emerging as one of the most important profitability drivers for the company. PB generated INR9.4b in renewal revenue in FY26 with margins of nearly 80%, creating a rapidly compounding annuity stream. Renewal revenue has reportedly grown ~15x since FY19, supported by improving persistency and long-duration customer cohorts.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412