Neutral Westlife Foodworld Ltd for the Target Rs. 535 by Motilal Oswal Financial Services Ltd

Weak print; positive start to 2026

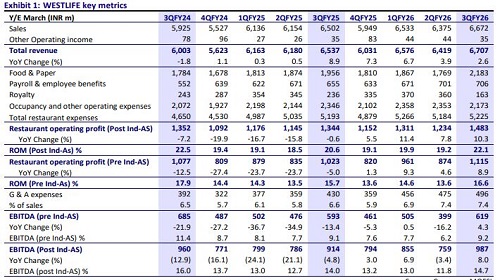

* Westlife Foodworld (WESTLIFE) reported revenue growth of 3% YoY (slowest among peers) to INR6.7b in 3QFY26 (below). Same-store sales growth (SSSG) declined 3.2% YoY (est. flat) on a soft base of +3%, given the ongoing challenging operating environment. Average sales per store declined 4% YoY to INR60m (annually) in 3QFY26. On-premise business grew 6% YoY, while the delivery business declined slightly due to volatility in third-party aggregators business.

* The company highlighted a healthy footfall growth in the West, while demand in the South remained soft. Footfalls improved from November onwards, with November–December reporting flat-to-positive YoY footfalls. This momentum extended into January, with positive SSSG driven by a mid-single-digit growth in footfalls.

* The company added net eight new stores (+9% YoY) in 3Q, with 27 stores added 9MFY26. It plans to open 20-25 stores in 4QFY26 and aims to grow its network to 580-630 restaurants by 2027.

* Reported GM contracted 260bp YoY to 67.5%. However, like-for-like GM was broadly stable QoQ. The reported GM reflects a one-off optical impact of 400–500bp in 3QFY26 due to the reclassification of processing charges from opex to COGS. EBITDA margin expanded 70bp YoY to 14.7%. (est. 14.3%) on account of lower royalty payment, while EBITDA margin (pre IND AS) was flattish YoY at 9.2%. ROM pre IND AS was up 90bp YoY to 16.6%.

* WESTLIFE continues to face demand headwind in the Southern region, but has been taking various initiatives to address the same. We believe regional demand will see a gradual improvement and, therefore, expect a gradual ADS recovery in the near future. We reiterate our Neutral rating with a TP of INR535, based on 28x Dec’27E EV/EBITDA (pre-IND AS).

Muted performance; same store sales down 3%

* Same store revenue down 3%: Sales grew 3% YoY to INR6.7b (est. INR7b), led by store additions of 9% YoY. SSSG declined 3.2% YoY in 3QFY26 (est. flat, -3% in 2QFY26, +2.8% in 3QFY25). WESTLIFE opened net eight stores (opened 10 stores, closed two stores), bringing the total count to 458 stores in 73 cities. Average sales per store declined 4% YoY to INR60m (annually) in 3QFY26.

* EBITDA (pre IND AS) up 4% YoY: GM contracted by 260bp YoY to 67.5% (est. 72%). However, like-for-like GM remained broadly stable QoQ, driven by supply chain efficiencies, partly offset by menu price adjustments following the GST rate change. The reported GM reflects a one-off optical impact of 400–500bp in 3QFY26 due to the reclassification of processing charges from opex to COGS. Reported EBITDA rose 8% YoY to INR987m (est. INR1,000m). EBITDA margin expanded 70bp YoY to 14.7% (est. 14.3%), led by lower royalty payment. EBITDA margin (pre IND AS) was up marginally by 10bp YoY to 9.2%, EBITDA (pre IND AS) up 4% YoY. ROM post Ind As was up 150bp YoY to 22.1% (est. 21.2%). ROM pre IND AS was up 90bp YoY to 16.6% (est. 16.1%).

Key takeaways from the management commentary

* Amid an ongoing challenging operating environment, the company prioritized driving affordability through its value platform while maintaining strict execution discipline.

* In December (every year), WESTLIFE receives additional accrued incentives from its parent company for its strong performance (e.g. store count, etc.)

* GM contracted 260bp YoY to 67.5%. However, like-for-like gross margin remained broadly stable on a sequential basis, driven by supply chain efficiencies, partly offset by menu price adjustment following the GST rate change.

* WESTLIFE plans to open 20-25 stores in 4QFY26. The company remains on track to achieve its target of 580–630 restaurants by 2027.

Valuation and view

* We largely maintain our estimates for FY27 and FY28. * Demand continued to remain impacted in 3Q, with SSSG declining YoY. However, the positive momentum of December has carried over into January, with positive SSSG driven by a mid-single-digit rise in footfalls. WESTLIFE has been aggressive in store additions, which was not the case historically. However, the performance in South India remains a challenge. Therefore, the benefits of its various initiatives may be gradual.

* Soft underlying growth, coupled with rising costs related to strategic initiatives, could weigh on the operating margins. We remain watchful of the same.

* We reiterate our Neutral rating with a TP of INR535, based on 28x Dec’27E EV/EBITDA (pre-IND AS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412