Buy Nippon AMC Ltd for the Target Rs.1,040 by Motilal Oswal Financial Services Ltd

Strong inflows sustain, scaling up adjacencies

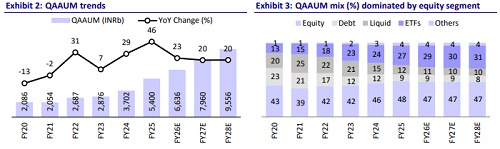

* NAM continues to deliver industry-leading market share gains, with MF QAAUM of INR7t (+23% YoY) and overall share at a five-year high of 8.7%. It is underpinned by steady net inflows, robust SIP momentum, and a favorable equity mix (47% in Dec’25), driving the highest FY26YTD equity share accretion in the industry to 7.1% (+11bp YoY).

* NAM reported stable blended yields of 37bp in 3Q (equity: 53bp) despite rising passive contribution, supported by a healthy equity mix and traction in high-yielding commodity ETFs. Management continues to guide for an annual compression of 1- 2bp due to telescopic pricing, to be offset by diversified retail flows, SIP growth, and product innovation.

* The company has the largest retail investor base of 22.7m in the industry (38.4% share), underpinned by a highly granular SIP book of INR1.7t, exhibiting materially higher stickiness than industry averages (49% vs. industry at 31% over five years).

* Its ETF platform, with INR2.1t AUM (+39% YoY/+14% QoQ in 3Q, led by strong growth in Gold/Silver ETFs) and ~20% market share, anchors passive leadership, supported by dominant folio share (48%) and exchange trading liquidity (51% volume share).

* The company is scaling up its alternatives, GIFT City, and offshore platforms, with cumulative AIF commitments of INR89.2b, GIFT City AUM of INR3.7b, and offshore AUM of INR180b, positioning these verticals as incremental growth drivers beyond the core MF franchise amid rising institutional and global investor participation.

* We expect a CAGR of 16%/17%/18% in revenue/EBITDA/core PAT over FY26-28E. We reiterate a BUY rating on the stock with a TP of INR1,040, premised on 38x core FY28E earnings.

Fastest-growing AMC with steady SIP flows and ETF dominance

* MF QAAUM grew 23% YoY/7% QoQ to INR7t, leading to a 35bp YoY/14bp QoQ increase in overall MF market share to 8.7%, the highest level since May’19. Equity market share increased 11bp YoY to 7.1%, marking the strongest equity share accretion across the industry so far in FY26. Equity (ex-arbitrage) assets constituted 47% of total AUM as of Dec’25.

* SIP AUM stood at INR1.7t (+23% YoY), while quarterly systematic transactions rose 19% YoY to INR50.4b. The SIP book demonstrates strong stickiness, with five-year retention of 49% vs. ~31% for the industry, supported by lower discontinuation rates and steady inflows. Notably, ~75% of SIPs by value are below INR10k, highlighting strong granularity.

* Despite the rising contribution from passive assets, blended yields remained broadly stable, supported by a healthy equity mix (47%) and strong traction in commodity ETFs (Gold and Silver), partially offsetting the typical margin dilution associated with passive scale-up.

* The company has the largest retail investor base in the industry, with 22.7mn unique investors and ~38.4% market share as of Dec’25, implying that over one-third of mutual fund investors in India are associated with the platform.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041