The Economy Observer : Expect real GDP growth of ~7.5% in 4QFY26 by Motilal Oswal Financial Services Ltd

EAI – Monthly Dashboard: Economic activity remains robust in Jan’26

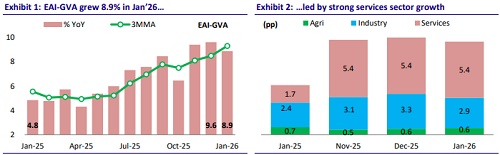

* Preliminary estimates indicate that India’s economic activity remained robust in Jan’26 (though moderated slightly from Nov’25/Dec’25), with EAI-GVA growing 8.9% YoY (vs. 9.6% in Dec’25 and 4.8% in Jan’25), marking the third consecutive month of over 8% growth. Growth was primarily driven by strong services activity and robust construction, although manufacturing momentum softened after a strong expansion in the previous two months.

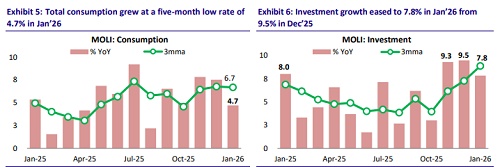

* EAI-GDP growth moderated to a three-month low of 2.1% YoY in Jan’26, led by a five-month low in consumption growth (4.7% YoY) and three-month low in investment growth (7.8% YoY). In addition, net exports weighed on growth, as imports expanded faster than exports.

* Services remained the key growth driver. Services sector growth strengthened to 9.9% YoY in Jan’26, supported by strong auto sales, expansion in trade credit, rising mutual fund AUMs, and continued growth in freight traffic and telecom subscribers, reflecting strong consumer and financial sector activity.

* The industry remained strong but moderated sequentially, and agriculture growth remained stable. Industrial growth eased to 9.3% YoY in Jan’26 from 11.9% in Dec’25, mainly due to moderation in manufacturing growth, although construction activity remained robust supported by strong steel and cement output. Meanwhile, agriculture growth improved to 4.3%, supported by strong tractor sales and double-digit rural wage growth.

* High-frequency indicators for Feb’26 suggest broadly resilient economic activity. Manufacturing PMI improved to 56.9 from 55.4 in Jan’26, while services PMI remained strong at 58.1, indicating continued expansion in both sectors. Domestic demand indicators were supportive, with registered motor vehicle growth accelerating sharply and CV sales remaining robust, while FX reserves increased further, strengthening India’s external buffer. On the downside, PV sales growth moderated compared with the previous month, and power generation contracted, indicating some softness in electricity demand. Overall, the indicators point to continued economic expansion, albeit with some mixed signals

* Our in-house models suggest that economic activity remained strong in Jan’26, with growth estimated at 8.9% YoY, though slightly moderating from Nov–Dec’25 (9.6%/9.4%). For Feb’26, high-frequency indicators indicate a mixed but broadly resilient picture. Based on our EAI estimates, real GVA growth is likely to remain around 7.4–7.5% YoY in 4QFY26, broadly in line with the CSO’s projection of 7.3%. The Second Advance Estimates (SAEs) have also revised FY26 GDP growth upward to 7.6% from 7.4%. Looking ahead, with the Chief Economic Advisor revising FY27 growth expectations to 7.0–7.4%, we expect real GDP growth of around 7.5% in FY27, with nominal GDP growth of about 11.5%, reflecting India’s continued structurally strong growth momentum.

* EAI-GVA grew 8.9% in Jan’26: Preliminary estimates indicate that India's economic activity moderated slightly in Jan’26 compared with Dec’25, though it remained strong on a YoY basis. EAI-GVA grew 8.9% YoY in Jan’26, growing over 8% for the third straight month (vs. 9.6%/4.8% YoY in Dec’25/Jan’25), with growth supported primarily by strong services activity and continued robustness in construction, while manufacturing momentum softened (8.8% in Jan’26 vs. 11.9% in Dec’25) after the sharp expansion seen in the previous two months. The agriculture sector improved modestly, supported by strong rural indicators such as rising tractor sales and sustained growth in real rural wages. Within services, growth strengthened further to 9.9% YoY in Jan’26 (9.5% in Dec’25), supported by strong auto sales, expansion in trade credit, and sustained growth in financial sector indicators such as mutual fund AUMs.

* EAI-GDP posted the lowest growth in three months: At the same time, EAI-GDP grew at a three-month low rate of 2.1% YoY in Jan’26 (vs. 6.6%/3.5% YoY in Dec’25/Jan’25), led by five-month low growth in consumption (4.7% in Jan’26 vs. 7.5%/5.3% in Dec’25/Jan’25) and a three-month low growth in investments (7.8% in Jan’26 vs. 9.5%/8% in Dec’25/Jan’25). Net exports contributed negatively to EAI-GDP in Jan’26 (lowest in three months) as imports grew faster than exports.

* Agriculture activity remained stable in Jan’26: Agriculture and allied sector growth improved to 4.3% YoY in Jan’26, up from 3.5% in Dec’25 and 4.8% in Jan’25, indicating stable rural activity. High-frequency indicators present a mixed but broadly supportive picture. Domestic tractor sales surged sharply, reflecting strong farm demand, while real rural wages grew in double-digits. Reservoir levels also remained comfortable, supporting agricultural prospects, although fertilizer output growth moderated slightly compared with the previous month.

* Industrial momentum softens slightly in Jan'26: Industrial activity moderated slightly in Jan’26, with sectoral growth easing to 9.3% YoY from 11.9% in Dec’25, though it remained stronger than 7.9% in Jan’25. The sequential slowdown was primarily driven by moderation in manufacturing growth (8.8% YoY in Jan’26 vs. 12.4%/11.9% in Dec’25/Nov’25) after strong expansion in the previous two months. However, underlying activity remained robust, supported by continued strength in construction, which maintained double-digit growth, driven by strong steel production and cement output. However, mining activity remained relatively subdued, reflecting continued contraction in crude oil and natural gas production

* Services: Strong consumer and financial activity drives continued expansion: Services sector growth strengthened further to 9.9% YoY in Jan’26, slightly higher than 9.5% in Dec’25 and significantly above 3.0% in Jan’25, highlighting strong momentum in the sector. The expansion was supported by robust growth in auto sales, trade credit, and mutual fund AUMs, indicating strong financial activity and consumer demand. Freight traffic and telecom subscribers also continued to expand, suggesting sustained momentum in logistics and digital services. However, real fiscal spending contracted for the second straight month

* EAI - Consumption growth moderated in Jan’26: Consumption growth moderated in Jan’26, with EAI consumption expanding at a five-month low of 4.7% YoY, compared with 7.5% in Dec’25 and 5.3% in Jan’25. High-frequency indicators present a mixed consumption picture. On the positive side, auto sales remained strong (grew at over 20% for the third straight month), reflecting continued discretionary demand, and personal credit continued to grow in double digits. Rural consumption conditions remain relatively supportive, with real rural wages continuing to post double-digit growth. At the same time, some indicators point to a moderation in demand conditions. Passenger traffic growth remained subdued, while consumer durable production contracted.

* Investment activity moderated but still strong: Investment activity also moderated sequentially, with EAI investment growth easing to a three-month low of 7.8% YoY in Jan’26, down from 9.5% in Dec’25 and 8.0% in Jan’25. Investment indicators suggest moderating but still supportive momentum through early 2025. Infrastructure-linked indicators such as cement production and IIP for non-metallic products continued to post strong growth, CV sales remained robust, and industrial credit growth also strengthened, reaching double-digit levels in the last two months. Meanwhile, capital goods imports remained volatile and government capex contracted for the 4th straight month in Jan’26 after strong expansion earlier. Despite these fluctuations, the manufacturing PMI remained comfortably in expansion territory, indicating continued improvement in industrial activity and investment sentiment.

* Economic picture for Feb’26 appears mixed but broadly resilient: High-frequency indicators for Feb’26 present a mixed but broadly resilient economic picture. Manufacturing activity strengthened, with PMI rising to 56.9 from 55.4 in Jan’26, while services PMI remained robust at 58.1, indicating continued expansion in both sectors. Domestic demand indicators were supportive, with registered motor vehicle growth accelerating sharply and CV sales remaining strong, although PV sales growth moderated somewhat compared with the previous month. On the other hand, power generation contracted in Feb’26, reversing the growth seen in Jan’26 and suggesting some softness in electricity demand. Meanwhile, FX reserves increased further, providing a strong external buffer. Overall, the indicators point to continued economic expansion with some mixed signals across sectors.

* Expect real GDP growth at 7.5% YoY in 4QFY26: Our in-house models suggest that economic activity remained strong in Jan’26, with growth estimated at 8.9% YoY, although slightly moderating from the pace seen in Nov’25/Dec’25 (9.6%/9.4%). For Feb’26, high-frequency indicators present a mixed but broadly resilient picture. Based on our EAI estimates, we expect real GVA growth to remain around 7.4–7.5% YoY in 4QFY26, broadly in line with the CSO’s projection of 7.3%. At the same time, according to Second Advance Estimates (SAEs), real GDP growth for FY26 has been revised upward to 7.6% from 7.4%, indicating stronger underlying growth momentum. Looking ahead, the Chief Economic Advisor has revised FY27 growth expectations to 7.0–7.4% (from 6.8– 7.2%), with an emphasis that growth is likely to be closer to the upper bound of the range. This reinforces the view that India remains in a structurally highgrowth phase. In line with this outlook, we expect real GDP growth of around 7.5% in FY27, with nominal GDP growth at approximately 11.5%..

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412