Mauritius economy update: Risks subdue growth by CareEdge Ratings

Growth outlook revised down amid heightened external risks

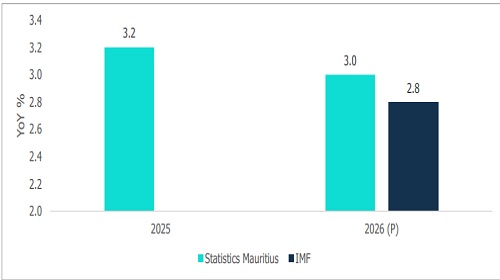

Mauritius’ growth outlook for 2026 faces increasing external risks from ongoing geopolitical tensions and softer global demand. As highlighted previously, Statistics Mauritius projects baseline growth at around 3.0% in 2026, but it could drop to around 2.3% if the Middle East conflict intensifies and prolongs.

In its Article IV end-of-mission statement released recently, the International Monetary Fund (IMF) announced that it has revised Mauritius’ 2026 growth forecast to 2.8% from an earlier 3.4%, citing external pressures and Middle East conflict spillovers. The IMF explained that the Mauritian economy remained relatively resilient in 2025, with real GDP growth estimated at 3.2%, supported by a strong services sector, particularly tourism and financial services. However, momentum is expected to moderate in 2026 amid heightened global uncertainty and subdued construction activity. Nonetheless, downside risks are contained as the Mauritian tourism sector continues to outperform (even though arrivals fell) regional peers such as the Maldives and Seychelles.

April sees YoY contraction in tourism as external risks mount

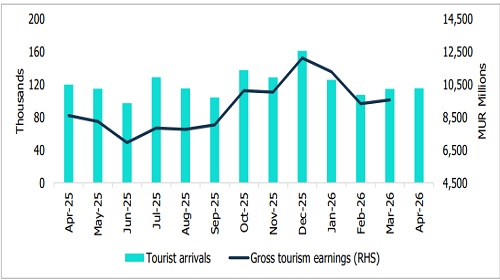

Tourist arrivals shrank 3.7% year-on-year (YoY) in April 2026, compounding the weak momentum observed recently as geopolitical uncertainties dampen travel demand and weigh on sector performance. Over January-April 2026, cumulative tourist arrivals increased 4% YoY to 464,208, supported by strong performance earlier in the year. However, the recent decline suggests that momentum is beginning to soften, leaving the sector vulnerable to prolonged external headwinds

Nevertheless, tourism earnings continued to be strong through March. Gross tourism receipts rose by 23% YoY to MUR 9.6 billion in the month, boosting cumulative earnings for the January-March period to MUR 30.2 billion, representing a 28% YoY increase. This strong performance reflects higher per-tourist spending, a depreciation of the Mauritian Rupee (MUR) against the Euro and favourable pricing dynamics. While these factors should partially cushion the sector against the moderation in tourist arrivals in April, a prolonged slowdown in arrivals will eventually soften tourism receipts in the coming months.

Looking ahead, Mauritius’ tourism sector faces increasing headwinds, as elevated airfares, flight cancellations, and global economic uncertainty weigh on travel demand and constrain visitor budgets. These factors are likely to dampen arrival growth in the near term. Nevertheless, cumulative performance since the start of the year suggests that Mauritius remains relatively resilient compared with its regional peers. Tourist arrivals to Mauritius increased by 4% YoY over January-April 2026, contrasting with a significant 13.4% contraction recorded in Seychelles over the same timeframe. Meanwhile, available data for Maldives over January-March indicates a marked growth slowdown, with arrivals rising by just 0.2% YoY. This relative outperformance highlights Mauritius’ continued competitiveness, though sustaining this position will depend on how effectively the sector navigates ongoing external pressures.

Gross tourism earnings and arrivals

Inflationary pressures resurface amid rising cost dynamics

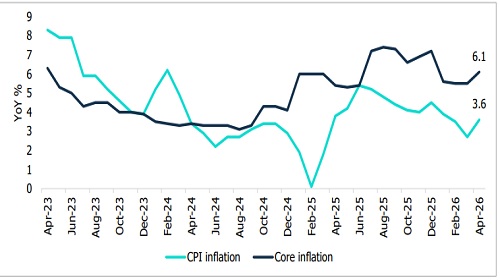

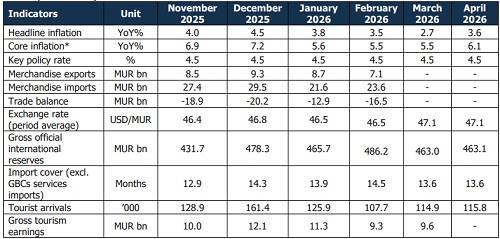

Headline inflation accelerated to 3.6% YoY in April 2026 from 2.7% YoY in March, reflecting broad-based price pressures. Notably, ‘transport’ inflation rose by 2.7% YoY, while ‘restaurants and accommodation services’ increased by 1.9%. Additionally, ‘housing, water, electricity, gas and other fuels’ grew by 1.7%, alongside a 4.5% surge in ‘personal care, social protection and miscellaneous goods and services’. These were the primary drivers of the rise in inflation during the month. Core inflation edged higher to 6.1% YoY in April from 5.5% YoY in March.

Looking ahead, Mauritius’ inflation outlook is increasingly tilted to the upside following the recent pickup in price pressures. Rising international oil prices and ongoing geopolitical tensions are beginning to feed through to domestic prices. Given the economy’s high dependence on imported fuel, higher energy costs are expected to transmit quickly via transport, electricity, and broader production and distribution channels, with potential secondround effects on services and food prices. Recent increases in administered prices, including fuel, electricity, and selected food items, will further reinforce these underlying pressures. Consequently, inflation in 2026 could overshoot initial expectations before gradually stabilising1 .

Monthly CPI and core inflation

Trade shows early signs of external strain

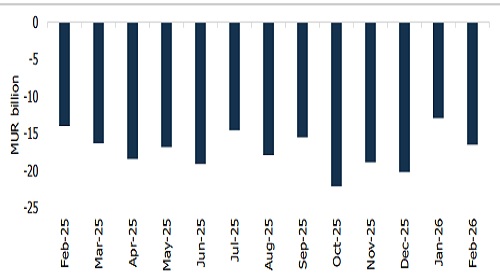

In February 2026, Mauritius’ merchandise trade deficit widened to MUR 16.5 billion, up from MUR 14.0 billion in February 2025. This deterioration was driven by an 11.7% YoY decline in exports alongside a 7.2% increase in imports. Weakening export performance reflected a 17.4% contraction in ‘food and live animals’, as well as a sharp 39.9% decline in ‘machinery and transport equipment’. At the same time, import growth was underpinned by higher purchases of ‘food and live animals’, a 19% increase in ‘machinery and transport equipment’, and a notable 42.7% rise in ‘chemicals and related products’.

Monthly merchandise trade balance

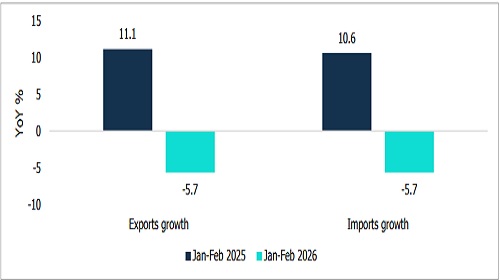

Cumulatively, Mauritius’ merchandise trade deficit narrowed to MUR 29.5 billion for the January-February 2026 period, down from MUR 31.2 billion in the corresponding 2025 period. This improvement was driven by lower import demand, with both imports and exports declining by 5.7% YoY over the period. The contraction in imports reflected a 12.4% decline in ‘mineral fuels, lubricants and related materials’, alongside a 17.6% fall in ‘manufactured goods classified chiefly by material’. On the export side, a 14.4% decrease in exports of ‘ship’s stores and bunkers’, and a 15.6% contraction in ‘miscellaneous manufactured articles’ weighed on performance.

Import and export growth

Looking ahead, Mauritius’ trade performance remains highly sensitive to global energy and commodity price developments, reflecting its structural dependence on imports. As a net oil importer, higher fuel prices are likely to directly increase the import bill, particularly for petroleum products, freight, and related logistics costs, while exerting indirect pressure through higher food and intermediate goods prices. Concurrently, export growth faces constraints from weakening global demand and rising transport costs, which may weigh on export margins despite trade preferences such as AGOA until December 2026. Overall, the external trade balance is likely to remain under pressure, with limited scope for rapid adjustment given Mauritius’ import-intensive production structure and reliance on external inputs.

Reserves position remains resilient

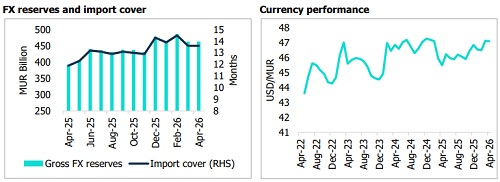

Mauritius’ gross official international reserves held steady at MUR 463 billion (USD 9.8 billion) in April 2026, compared with March levels. Consequently, import cover was maintained at 13.6 months in April, based on imports of goods and services, excluding Global Business Companies (GBC) services. However, under the Bank of Mauritius’ newer metric incorporating GBC services imports, in line with the enhanced Balance of Payments framework since September 2025, import cover was lower at 10.0 months in April 2026. This provides a broader assessment of external sector resilience and reserve adequacy.

In April 2026, the MUR averaged 47.1 against the USD, broadly unchanged from March, despite continued global uncertainty linked to geopolitical tensions. Over February-April, however, the currency recorded a modest depreciation of 1.3%. The relative stability observed in April partly reflects balanced foreign exchange conditions, although this was moderated by weaker tourism inflows, as geopolitical developments weighed on tourist arrivals.

In addition, the Bank of Mauritius intervened in the domestic foreign exchange market, selling USD 15 million on April 16, 2026 at a rate of MUR 46.21 per USD, which helped contain excessive volatility in the exchange rate.

Looking ahead, the MUR is expected to face moderate depreciation pressures, driven by rising import demand amid elevated global commodity prices, alongside higher freight and insurance costs. Simultaneously, softer tourism receipts may reduce foreign currency inflows in the near term. While other service exports continue to provide support, these are unlikely to fully offset the anticipated increase in the import bill, thereby maintaining downward pressure on the currency.

FX reserves and import cover

Above views are of the author and not of the website kindly read disclaimer