Lending Momentum Continues on a Stable Trajectory by CareEdge Ratings

Synopsis

• Credit growth continued to outpace deposit accretion, although the gap narrowed slightly to ~370 bps in the current fortnight from 380 bps in the previous fortnight. The Loan-to-Deposit Ratio (LDR) consequently increased to 82.0% as on April 30, 2026, from 81.6% in the previous fortnight, reflecting stronger sequential growth in credit relative to deposits, while remaining below the peak level of 83.0% recorded in mid-March 2026.

o Total bank credit stood at Rs 212.1 lakh crore as on April 30, 2026, registering a y-o-y growth of 16.0% compared with 10.3% in the corresponding period last year. Sequentially, credit increased by 1.4% over the previous fortnight, supported by continued growth in retail and MSME lending, incremental lending to NBFCs, and selective corporate borrowings.

o Aggregate bank deposits increased to Rs 258.6 lakh crore as on April 30, 2026, registering a y-o-y growth of 12.3% compared with 10.1% in the corresponding period last year. Sequentially, deposits rose by 0.8% over the previous fortnight, supported by steady retail deposit mobilisation.

• As of May 01, 2026, the Weighted Average Call Rate (WACR) increased marginally to 5.16% compared to 5.08% in the previous fortnight and remained nine basis points (bps) below the prevailing repo rate of 5.25%

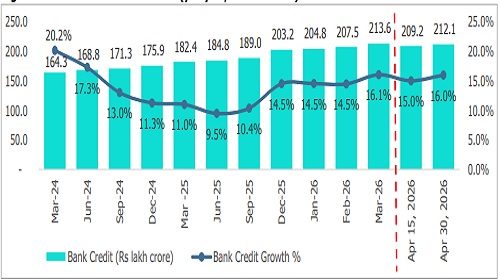

Bank Credit Growth Remains Robust YoY and Sequentially

Figure 1: Bank Credit Growth Trend (y-o-y %, Rs lakh crore)

• Bank credit growth improved to 16.0% y-o-y as on April 30, 2026, compared with 15.0% in the previous fortnight and 10.3% in the corresponding fortnight last year, reflecting sustained momentum in lending activity across segments. On a sequential basis, credit outstanding increased by Rs 2.9 lakh crore (1.4%) over the previous fortnight, reaching Rs 212.1 lakh crore. However, incremental credit growth during April remained relatively moderate, in line with the typical slowdown observed after the financial year-end surge in March. Despite this, overall credit growth was primarily supported by continued traction in retail lending, particularly in gold and vehicle loans, as well as steady MSME financing and working capital requirements. Incremental

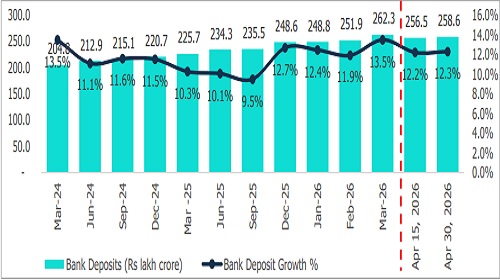

Figure 2: Bank Deposit Growth Sees Marginal Sequential Increase (y-o-y %, Rs lakh crore)

• Bank deposits increased by Rs 2.1 lakh crore (0.8%) on a sequential basis to Rs 258.6 lakh crore as on April 30, 2026. The deposit growth improved marginally to 12.3% y-o-y from 12.2% in the previous fortnight. It remained above 10.1%, the level recorded in the corresponding period last year, indicating improvement in overall deposit mobilisation. Time deposits remained the key driver of deposit growth, accounting for 87.2% of total deposits and rising by 12.2% y-o-y to Rs 225.6 lakh crore, compared with 8.7% growth in the year-ago period. Meanwhile, demand deposits grew by 13.0% y-o-y, moderating from 19.8% in the corresponding period last year, reflecting normalisation in low-cost deposit growth following higher base effects and shifting customer preference towards term deposits.

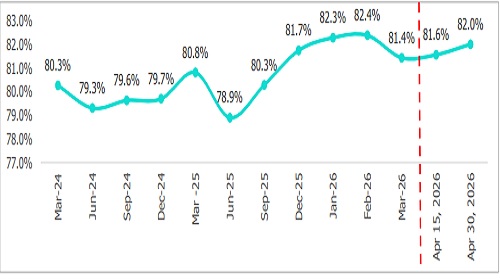

Figure 3: Loan-to-Deposit Ratio Edges Up Sequentially

The loan-to-deposit ratio (LDR) increased to 82.0% as of April 30, 2026, from 81.6% in the previous fortnight and 80.8% in the corresponding period last year, indicating that credit growth continued to outpace deposit mobilisation. The sequential increase was driven by a faster rise in bank credit (1.4%) compared with deposits (0.8%) during the fortnight.

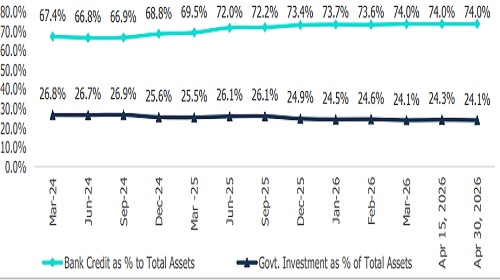

Bank Credit Share Remains Firm while Government Investments Decrease

Figure 4: Proportion of Govt. Investment and Bank Credit to Total Assets (%)

The credit-to-total assets ratio remained stable at 74.0% as on April 30, 2026, while the share of government investments in total assets moderated slightly to 24.1% from 24.3% in the previous fortnight. Sequentially, G-Secs (including Central and State government securities) grew modestly at 0.6%.

Above views are of the author and not of the website kindly read disclaimer