Key Highlights: RBI–MPC Expectations: Policy Pause Likely Amid Uncertain Macro Landscape by CareEdge Ratings

Backdrop: MPC Policy Meeting Comes Amidst Volatile Environment

• Conflict in West Asia entered its third month without any meaningful resolution, extending beyond initial expectations.

• Global crude oil prices have risen by 30% since the beginning of crisis.

• Inflationary concerns have intensified as retail fuel price increases by cumulative of about Rs 7.5/lit in last one month

• Sharp rise in WPI inflation in April to 8.3% also raises the risk of a faster second-round pass-through to consumer prices.

• Domestic growth outlook has weakened considerably as the economic impact of the prolonged conflict transmits through multiple channels.

• Both global and domestic bond yields rose sharply amid a persistently inflationary environment and increasing fiscal concerns.

• USD/INR has weakened by 4.9% since the onset of the conflict, due to subdued investment inflows and a widening of current account deficit.

• Against this backdrop, we expect the RBI’s Monetary Policy Committee (MPC) to remain in a wait-and-watch mode, maintaining a status quo on both policy rates and stance while closely monitoring evolving geopolitical developments.

• Tone of the policy statement will be crucial, as the possibility of policy rate hikes towards the end of the year cannot be ruled out if the inflationary pressure prolongs.

• Measures aimed at supporting the rupee — including measures to attract capital flows and special dollar liquidity facilities for oil marketing companies (OMCs) — may also be considered.

The MPC Awaits Signal: Transient or Persistent Price Pressures?

• We expect the MPC to adopt a wait-and-watch approach amid external volatility, assessing whether current price pressures are transient or persistent based on external developments. The current uptick in inflation is a supply shock and not demand driven.

• If external conditions stabilize fast, the recent uptick in inflation can be seen as transient.

• In this scenario, the real policy rate is expected to remain below its long-term average (0.95%) for three quarters (Q2 FY27–Q4 FY27), before converging to this average by Q1 FY28, and move into the RBI’s estimated natural rate band (1.4–1.9%) by Q2 FY28.

• Future trajectory of the policy rate will depend on the MPC’s assessment of evolving inflation dynamics, which are significantly influenced by external factors.

• If the MPC considers inflationary pressures to be transient it may look through the nearterm spike. However, if conflict persists and inflation risks become entrenched in household expectations, rate hikes could be considered toward the end of the year.

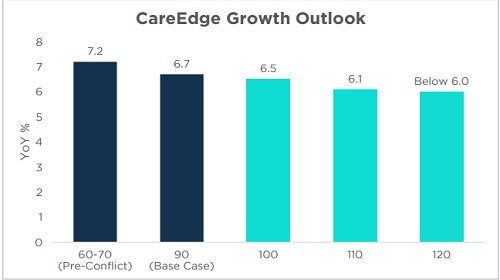

• MPC will also remain attentive to growth risks. We project FY27 GDP growth at 6.7% assuming crude oil averaging USD 90/bbl. However, prolonged conflict and oil prices around USD 110/bbl could lower growth closer to 6%.

• Growth in FY27 is likely to remain below potential growth rate of 7% as estimated by Economic Survey.

• This further reinforces our expectation that the RBI should be comfortable with a few quarters of low real policy rate, unless there is clear evidence of sustained pass-through into household inflation expectations.

• Some central banks, such as Bank Indonesia, have implemented larger-than-expected rate hikes, it is important to note that BI’s primary mandate focuses on Rupiah stability, unlike the RBI.

• The RBI has additional tools and a comfortable foreign exchange reserves to manage exchange rate volatility beyond policy rate adjustments.

Growth Projections to be Revised Downward

• We expect Q4 FY26 GDP growth to moderate to around 6.8–7.0%, compared with 7.8% in Q3FY26. Q4FY26 remained partially insulated from the adverse effects of the crisis, as the first two months of the quarter were relatively unaffected.

• In addition, companies likely relied on existing inventories to cushion the impact of rising input costs. Moreover, the government and OMCs absorbed a major portion of the increase in energy prices before the pass-through to consumers began in Q1FY27.

• However, growth momentum is likely to weaken further in Q1 FY27 as impact of the West Asia crisis gradually transmits through the economy.

• Furthermore, potential impact of El Nino conditions poses downside risks, particularly for the agricultural sector, which is already facing pressures from elevated fertiliser and input costs.

• Growth projected at 6.7% in FY27 assuming crude averages $90/bbl. However, it can inch closer to 6% if conflict lingers longer with average crude oil price at $110/bbl.

• We expect the MPC to lower growth projections from its earlier projection of 6.9% .

Inflation Projections to Be Revised Up

The cumulative increase in retail fuel prices following the conflict in West Asia is estimated to have a direct impact of around 35 bps on headline CPI inflation. Indirect inflationary pressures may add another 10–15 basis points to overall CPI inflation.

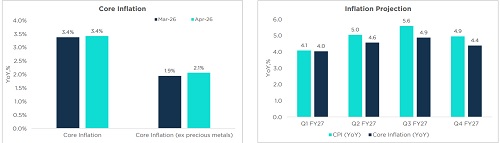

• High WPI inflation in April to 8.3% increases the risk of faster pass-though to consumers. Considering the higher pass-through of costs to consumers and impact of ElNino, we expect CPI inflation in FY27 to average in the range of 4.6–5.0% (assuming brent oil prices average $90/bbl). RBI is likely to revise its inflation projection upward inline with our projection.

• The MPC is likely to derive some comfort from the recent correction in Crude prices following expectations of positive developments in West Asia.

• Additionally, core inflation (excluding precious metals) has remained benign so far, at 2.1% in April, which should also provide reassurance to the MPC. However, core inflation is expected to average around 4.5% in FY27.

• Despite the recent increase in retail fuel prices by Rs 7.5/lit, there remains further scope for upward revisions, depending on the trajectory of global crude oil prices.

Above views are of the author and not of the website kindly read disclaimer