ECLGS 5.0 to Support Entities Affected by the West Asia Conflict by CareEdge Ratings

Synopsis

The Emergency Credit Line Guarantee Scheme (ECLGS), launched during the COVID-19 crisis, has evolved into a central policy instrument, transitioning from broad-based relief to targeted support for sectors vulnerable to global and geopolitical shocks. The RBI’s Financial Stability Report indicates that credit-guarantee schemes such as ECLGS and CGFMU have meaningfully improved credit access for MSMEs while containing asset quality risks, thereby strengthening both enterprise resilience and systemic stability. Building on this experience, ECLGS 5.0 seeks to catalyse Rs 2.55 lakh crore in additional credit and functions as a counter-cyclical tool to ease liquidity stress, support employment and production, and mitigate macro-financial spillovers during periods of heightened uncertainty.

Overview

The Union Cabinet has approved ECLGS 5.0, which aims to provide credit guarantee coverage to Lenders via the National Credit Guarantee Trustee Company Limited (NCGTC) for the amount in default under the additional credit facility extended to eligible borrowers to tide over short-term liquidity mismatches in view of the West Asia Crisis. The key features of the scheme include:

Segment Details Eligible Borrowers

• MSMEs and non-MSMEs with existing WC limits and airlines with o/s credit facilities, as of March 31, 2026, provided their accounts are standard. Guarantee Coverage

• 100% for MSMEs

• 90% for non-MSMEs as well as the airline sector Guarantee Fee

• Nil Quantum of Support

• Additional credit up to 20% of peak working capital utilised during Q4FY26 (capped at Rs 100 crore)

• Airlines: Up to 100% (capped at Rs 1,500 crore per borrower) Tenor of Loan

• MSMEs/non-MSMEs (except the airline sector): 5 years from the date of first disbursement, including a moratorium of 1 year.

• Airlines: 7 years from the date of first disbursement, including a moratorium of 2 years. Tenure of Guarantee Cover

• The maximum period of guarantee coverage is to be aligned with the loan tenor. Scheme Duration The scheme would apply to all loans sanctioned during the period from the date of issue of these guidelines by NCGTC up to March 31, 2027

CareEdge View

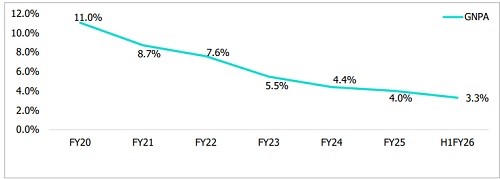

MSME credit has grown strongly, with outstanding advances crossing Rs 35 lakh crore, registering a CAGR of 15.1%, indicating higher bank lending to the sector. The MSME GNPA ratio has shown steady improvement, declining from 11% in FY20 to 3.3% by September 2025, supported by recoveries, upgrades and moderation in fresh slippages. Further, MSME lending remains largely priority-sector driven, with around 80%-90% of PSBs' exposure and 70%-85% for PVBs classified as priority sector. However, the pace of improvement has slowed recently, suggesting limited room for further significant declines in GNPA. With MSMEs becoming more export-CareEdge View MSME credit has grown strongly, with outstanding advances crossing Rs 35 lakh crore, registering a CAGR of 15.1%, indicating higher bank lending to the sector. The MSME GNPA ratio has shown steady improvement, declining from 11% in FY20 to 3.3% by September 2025, supported by recoveries, upgrades and moderation in fresh slippages. Further, MSME lending remains largely priority-sector driven, with around 80%-90% of PSBs' exposure and 70%-85% for PVBs classified as priority sector. However, the pace of improvement has slowed recently, suggesting limited room for further significant declines in GNPA. With MSMEs becoming more export

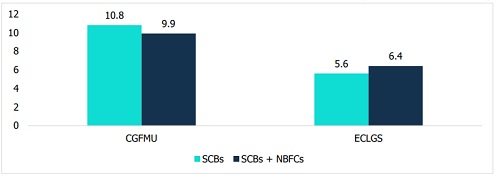

According to the RBI's Financial Stability Report, government credit-guarantee schemes have significantly strengthened the flow of institutional credit to the MSME sector, particularly to financially vulnerable enterprises. Around Rs 6.28 lakh crore of guarantees have been extended under two flagship initiatives, namely the Credit Guarantee Fund for Micro Units (CGFMU) and the ECLGS. Notwithstanding the relatively higher risk profile of the beneficiary borrowers, the non-performing asset (NPA) ratios under both schemes have remained well contained. This experience underscores the role of well-designed credit-guarantee mechanisms in simultaneously supporting MSME resilience and preserving systemic financial stability.

Introduced at the height of the COVID-19 pandemic, the Emergency Credit Line Guarantee Scheme has evolved into an instrument of the government’s crisis-management strategy. In the current iteration, the framework has moved beyond broad-based relief to offer targeted credit support for sectors that remain particularly exposed to global economic disruptions, supply-chain volatility, and geopolitical shocks. The ECLGS 5.0 is expected to facilitate an incremental credit flow of Rs 2.55 lakh crore, including a dedicated Rs 5,000 crore window for the aviation sector (which can help address elevated ATF prices) to mitigate stress arising from the West Asia conflict.

Meanwhile, the o/s bank credit to the aviation sector as of March 2026 stood at Rs 52,688 crore, up 14.4 y-o-y from last year. If the full amount of Rs. 5,000 crores earmarked for the sector is disbursed, the proposed measure would be approximately 9.5% of the year-end advances. The scheme has been introduced at a time when many MSMEs are facing tighter cash-flow cycles, delayed receivables, and heightened operational uncertainty. Along with the longer tenure, the 100% government guarantee embedded in the scheme reduces lenders’ risk perception, thereby enabling smoother credit flow. As highlighted earlier, experience from earlier phases suggests that targeted, time-bound credit-guarantee mechanisms can enhance MSME resilience while maintaining asset quality.

Above views are of the author and not of the website kindly read disclaimer

.jpg)