Buy Triveni Turbine Ltd for the Target Rs. 615 by Motilal Oswal Financial Services Ltd

Export inflows yet to recover

Triveni Turbine (TRIV)’s 3QFY26 result reflected a beat on revenue, fueled by higher export execution, while PAT was in line. Domestic inquiries are improving with new products, too, gaining traction in terms of inquiries. Export order inflows are still weak but are expected to recover by 4QFY26. The 9MFY26 order inflows dipped 9% YoY, which can result in revenue volatility for FY27. We expect profitability to be dependent on the revenue mix going forward. TRIV is also working on new products and initiatives, which will start yielding benefits in 1-2 years. To factor in lower inflows seen in 9MFY26, we cut our estimates by 5%/8% for FY27/28 and arrive at our revised TP of INR615, premised on 40x Mar’28 estimates. We reiterate our BUY rating as we believe the company can ramp up sharply whenever demand revives.

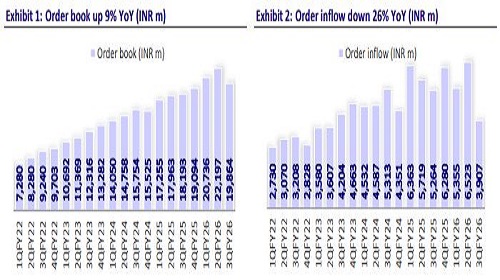

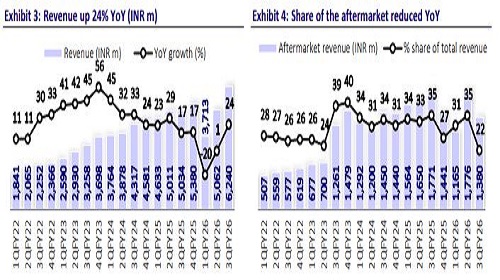

Beat on revenue and EBITDA; PAT in line TRIV’s 3QFY26 revenue and EBITDA were above our estimates, while PAT was in line. Revenue was above our estimates and increased 24% YoY to INR6b. Domestic sales were down 6% YoY to INR2.4b, while export sales increased 54% YoY to INR3.9b. Gross margin dipped 270bp YoY to 46.8%, leading to an EBITDA margin contraction of 20bp/110bp YoY/QoQ to 21.5%, though this was ahead of our expectation of 21.2%. Absolute EBITDA rose 23%/17% YoY/QoQ to INR1.3b, representing a 13% beat versus our estimate. Lower other income and a higherthan-expected tax rate resulted in an in-line PAT, which increased 11% YoY to INR1b. Order inflows declined 26% YoY to INR4b due to weak export ordering. This led to an order book of INR20b as of Dec’25 (+9% YoY). With reference to the new labor code, TRIV recognized a one-time impact of INR157m. For 9MFY26, its revenue and EBITDA increased 2% each YoY, but PAT declined 2% YoY. TRIV’s EBITDA margin was flat YoY at 21.5% for the period.

Domestic inquiry conversion visibility improves TRIV reported domestic order inflows of INR2b in 3QFY26 (broadly flat YoY), while domestic revenues declined 6% YoY to INR2b, reflecting continued delays in dispatches and customer readiness. The domestic order book increased sharply by 64% YoY to INR10b. The domestic inquiry pipeline remains strong across food processing, chemicals, sugar distilleries, steel, and cement. The company also expects incremental orders similar to heat pumps that it is executing for NTPC and from mechanical vapor recompression (MVR). Thus, the domestic market outlook remains strong in both the medium and long term. We bake in 15%/18% YoY growth in domestic inflows for FY27/28, resulting in similar growth in domestic revenue for the same period.

Export order inflows likely to recover by 4QFY26 TRIV reported strong export revenues in 3QFY26, up 54% YoY to INR4b, reflecting the execution of prior orders, even as export order inflow declined 40% YoY to INR2b. The export order book also declined 20% YoY to INR9b, driven by delays in finalizations. With easing trade?related uncertainty, management highlighted improving traction in newer applications such as geothermal and waste?to? energy. TRIV expects inflows to come from product, aftermarket, and refurbishment. We expect export inflows to grow 20%/22% in FY27/FY28.

South Africa provides an incremental growth opportunity from FY27 TRIV has consolidated its South African operations to create a unified platform for addressing refurbishment and aftermarket opportunities across Sub-Saharan Africa. Management highlighted a growing opportunity pipeline in utility refurbishment, leveraging prior execution experience to pursue similar projects in neighboring markets. The focus remains on services-led growth rather than large new-build orders, which should support steadier execution. While near-term revenue contribution is modest, the South Africa platform provides incremental growth optionality from FY27 onwards.

The US business expected to approach breakeven in FY27 TRIV continued to report losses in its US operations, with the subsidiary incurring a loss of ~INR210m in 9MFY26 as the company invests to build market presence. The inquiry momentum has improved across data centers, SMRs, industrial applications, and refurbishment opportunities. The recent reduction in US import duties is expected to support faster inquiry-to-order conversion. While near-term revenue contribution remains limited, the US business is likely to move towards breakeven in FY27, with operating leverage becoming more visible from FY28 onwards.

New products to scale gradually New product initiatives continued to gain commercial traction, though revenue contribution remains modest in the near term. CO?-based heat pumps have crossed 100+ inquiries with the first order secured, while MVR systems have seen 7-8 orders under execution, validating customer acceptance. The company is also progressing in geothermal applications, drives, and energy storage solutions. Management positioned FY27 as a validation and execution phase, with meaningful revenue and margin contribution expected from FY28 as these platforms scale.

Financial Outlook We broadly maintain our estimates for FY26 and cut our estimates by 5%/8% for FY27/28 to bake in the impact on revenue from lower order booking in FY26. We expect TRIV’s revenue/EBITDA/PAT to clock a CAGR of 11%/11%/11% over FY25-28. Backed by a comfortable negative working capital cycle, strong margins, and low capex requirements, we expect its OCF and FCF to report a CAGR of 44% and 49% over the same period, respectively.

Valuation and view The stock is currently trading at 42.8x/38.1x/33.1x on FY26E/27E/28E earnings. We roll forward our TP to INR615, based on 40x Mar’28E earnings. We maintain our BUY rating. However, in the near term, we expect performance to remain impacted by weakness in order conversions.

Key risks and concerns Slowdown in capex initiatives; intensified competition; technology disruption; inability to innovate and launch new products; and geopolitical headwinds resulting in a sharp slowdown in exports and aftermarket segments.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412