Buy JK Lakshmi Cement Ltd for the Target Rs. 900 by Motilal Oswal Financial Services Ltd

Weak performance; next phase of expansion remains slow

Trade volumes rebound; pricing upside ahead

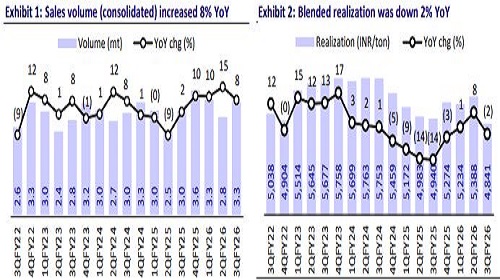

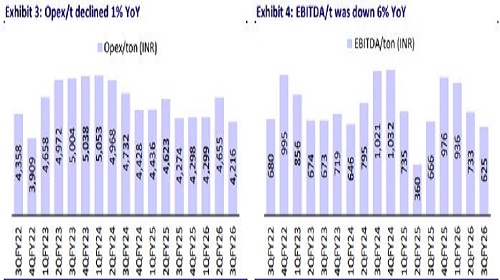

* JK Lakshmi Cement’s (JKLC) 3QFY26 EBITDA was up marginally ~2% YoY to INR2.1b (~20% miss due to lower-than-estimated realization/t). Sales volume increased ~8% YoY to 3.3mt (in line). EBITDA/t declined ~6% YoY to INR625 (est. INR801). OPM contracted 60bp YoY to ~13% (est. ~15%). Adj. PAT declined ~5% YoY to INR714m (-34% vs. our estimate).

* Management indicated that trade sales declined during the period, primarily due to higher volumes in Gujarat following the commissioning of Surat GU. Further, non-trade prices were under significant pressure due to temporary disruptions from GST-related pass-through, extended monsoons, elections in Bihar, and labor shortages. However, it is seeing a pick-up in trade demand in Dec’25-Jan’26 as well as price increases in non-trade across markets in late-Dec’25. It estimates industry volume growth in double digits in 4QFY26, and aims to grow in line with the industry.

* We cut our EBITDA estimates ~7% for FY26 and ~3% for FY27E-FY28 (each) to factor in 3Q underperformance and lower volume growth in FY27. The stock is trading reasonably at 10x/9x FY27/FY28E EV/EBITDA. We value the stock at 10x FY28E EV/EBITDA to arrive at our TP of INR900. Reiterate BUY.

Volume up ~8% YoY; realization/t declines ~2% YoY (down 10% QoQ)

* Consol. revenue/EBITDA/adj. PAT stood at INR15.9b/INR2.1b/INR714m (+6%/+2%/-5% YoY and down ~6%/20%/34% vs. our estimates). Volume grew ~8% YoY to 3.3mt (in line). Realization/t was down 2%/10% YoY/QoQ at INR4,841/t (~8% below estimates).

* Opex/t declined 1% YoY (~6% below estimates), led by a ~7%/3%/2% YoY decline in employee expenses/other expenses/freight expenses per ton. However, Variable cost/t increased ~1% YoY. OPM contracted 60bp YoY to ~13%, and EBITDA/t declined ~6% YoY to INR625 in 3QFY26. Depreciation/finance costs were up ~12%/21% YoY. Other income was up 3.2x YoY.

* In 9MFY26, revenue/EBITDA/Adj. PAT stood at INR48.6b/INR7.2b/INR3.1b (up ~13%/41%/2.2x YoY). OPM expanded 3.0pp YoY to ~15%. Realization/t was up ~2% YoY to INR5,144, while EBITDA/t grew ~27% YoY to INR767.

Highlights from the management commentary

* Industry demand grew ~7% YoY in 3Q. Overall demand outlook is positive, which is also expected to lead to price increases in the trade segment.

* Its trade volume share declined to 49% vs. 57%/53% in 3QFY25/2QFY26. The blended cement share was ~62% v/s ~65%/62% in 3QFY25/2QFY26.

* Capex stood at INR3.5b in 9MFY26, including INR2.5-2.6b towards the Durg expansion. Capex to be incurred is estimated at INR4.0b in 4QFY26. Capex is pegged at INR16.b-17.0b in FY27.

Valuation and view

* JKLC reported a weak set of results in 3Q, with realization/t below estimates due to declining prices in Gujarat markets, where it has higher exposure. Meanwhile, the company’s opex/t remained under control. It expects prices to improve following the continued strong demand momentum. Further, its clinker capacity is operating at an optimum level, and the next clinker line at Durg is expected in end-FY27/FY28. Hence, we estimate it has a limited volume growth opportunity in the near term.

* We estimate a CAGR of ~8%/12%/7% in revenue/EBITDA/PAT over FY26-28 and project an EBITDA/t of INR851/INR870 in FY27/FY28E vs. INR790 in FY26E. We further estimate its net debt to rise to INR26.7b in FY28 from INR19.7b in FY26. The net debt-to-EBITDA ratio is estimated to be range-bound at 2.0x over FY26-28. The stock is trading reasonably at 10x/9x FY27E/FY28E EV/EBITDA. We value the stock at 10x FY28E EV/EBITDA to arrive at our TP of INR900. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412