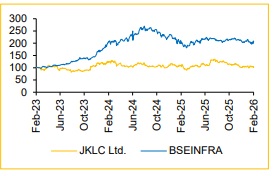

Buy JK Lakshmi Cement Ltd for Target Rs.1,075 by Choice Institutional Equities

Strong Capacity Addition Planned

We maintain our BUY rating on JK Lakshmi Cement Ltd (JKLC) with a revised TP of INR 1,075 (implying an upside of 41.2%) (vs earlier 1,175), as we moderate our margin forecast for FY27E/28E. On our TP, JKLC’s implied FY28E EV/EBITDA is 9.9x, which is reasonable. The amalgamation of Udaipur Cement Works Ltd. (UCWL) and its other subsidiaries into JKLC removes the overhang of a complex corporate structure. We continue to be constructive on JKLC owing to: 1) Capacity addition plans to reach 30 Mnt by FY30E, 2) Positive pricing momentum expected owing to sectoral tailwinds and 3) Cost-saving of INR 120/t expected in the next 2 years. We adopt a robust EV-to-CE (Enterprise Value to Capital Employed) valuation framework, which provides a rational basis for assigning a valuation multiple that captures fundamentals (ROCE expansion of 380 bps over FY25–28E).

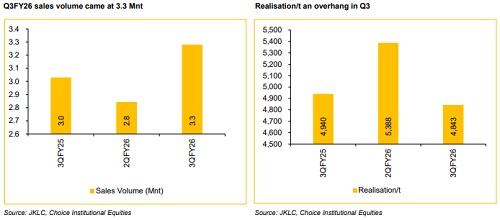

We forecast JKLC’s EBITDA to expand at a CAGR of 18.8% over FY25– 28E, supported by our assumption of volume growth of 8.0/6.0/6.0% and realisation growth of 3.5/0.5/0.0% in FY26E/FY27E/FY28E, respectively.

We value JKLC on our EV/CE framework, where we assign an EV/CE multiple of 2.2x/2.2x for FY27E/28E. This framework gives us the flexibility to assign a commensurate valuation multiple based on an objective assessment of the quantifiable forecast financial performance of the company. We did a sanity check of our EV/CE TP using implied EV/EBITDA multiples. On our TP of INR 1,075, the implied FY28E EV/EBITDA multiple translates to 9.9x, which is reasonable in our view.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131