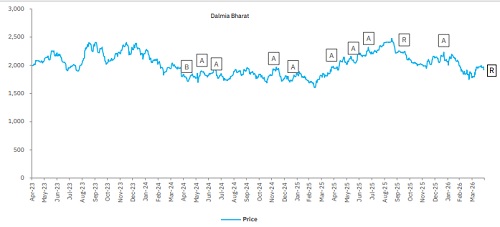

Buy Dalmia Bharat Ltd for Target Rs.2020 by Elara Capital

Volume underperformance continues

Dalmia Bharat (DALBHARA IN) reported EBITDA of ~INR 9.0bn in Q4FY26, in line with our estimates but ~8% ahead of Bloomberg estimates, up ~14% YoY. However, realization growth was lower than that reported by peers till date due to lower recoveries of incentives on account of elections. DALBHARA expects an impact of INR 125-150/tonne in Q1FY27 due to operational challenges arising from the West Asia Conflict (~INR 80-90/tonne is expected to be for the packaging cost). Going ahead, recent price hikes in DALBHARA’s core market should provide cushion against the jump in the cost structure. Net debt declined to INR 14.3bn in Q4FY26 versus INR 17.9bn in Q3FY26. Given higher presence in oversupply markets of South and East India, we believe DALBHARA will be unable to pass on the full impact of cost increase in H2CY26. Thus, we revise DALBHARA to Reduce from Accumulate with a lower TP of INR 2,020 (from INR 2,384) on 12.0x March 2028E EV/EBITDA.

Sequential EBITDA per tonne improvement lower then peers: Volumes grew ~3% YoY and ~20% QoQ to ~8.8mn tonnes. Management attributed weak YoY growth to plant breakdown at Rajgangpur, Odisha, which led to volume loss of 3%. However, it may be noted that FY26 and FY25 volume growth for the company stood at ~2% each, lagging industry growth for the second year. The management targets above-industry growth in FY27 with focus on profitability. Blended realization was up ~1% YoY and QoQ to INR 4,824/tonne, due to improved pricing but partly offset by lower incentives. Further, operating costs were down ~1% YoY and ~4% QoQ to INR 3,799/tonne due to reduction in power and fuel cost and benefits of operating leverage. EBITDA/tonne improved QoQ by INR 202 to INR 1,025 versus our estimate of INR 970. Ultratech Cement and Nuvoco Vistas Cement reported QoQ EBITDA per tonne improvement of INR 245 and INR 212 respectively.

Clarity on roadmap awaited to reach 75mn tonnes by FY28: Announced expansions — 3.6mn tonnes of clinker and 3.0mn tonnes of cement capacity at Belgaum, along with 3.0mn tonnes of cement capacity at Pune — are progressing as planned with civil work already completed for Belgaum. These projects are expected to take clinker and cement capacities to ~30.7mn tonnes and ~55.5mn tonnes, respectively, by end-FY27. FY27 capex is guided at ~INR 32–34bn (of which ~INR 22–23bn is towards expansion). Further expansion is underway at Kadapa (Andhra Pradesh), with a 3.6mn-tonne clinker unit and 6.0mn-tonne grinding unit, along with a 3.0mn-tonne bulk terminal in Chennai (Tamil Nadu), targeted for commissioning by Q2–Q3FY28. Post completion, total cement and clinker capacities are expected to reach ~61.5mn tonnes and ~34.3mn tonnes, respectively. The company is also evaluating a grinding unit in the North East to use surplus clinker and is targeting to achieve its ~75mn tonne capacity target by FY28.

Revise to Reduce with a lower TP of INR 2,020: We expect peak cost inflation to hit in Q2FY27, coinciding with seasonal volume weakness. Factoring in higher fuel and packing costs, we cut EBITDA estimates by 15% for FY27E and 6% for FY28E and introduce FY29E. We downgrade to Reduce (from Accumulate), and maintain 12x Mar ’28E EV/EBITDA—advising investors to await a better entry point. A sharp uptick in cement price is the key upside risk.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

.jpg)