Buy Dr. Agarwal’s Health Care Ltd for the Target Rs. 565 by Motilal Oswal Financial Services Ltd

Multi-region scale-up keeps growth intact

High-end surgeries, facility maturity and patient growth drive upside

* Dr. Agarwal’s Health Care (DAHL) delivered better-than-estimated earnings in 3QFY26. While revenue was largely in line, EBITDA/PAT came in 8% above our estimates. Growth was driven by an increased share of high-end surgical procedures, robust product sales, and facility additions.

* DAHL reported 24% YoY growth in the number of patients served for eye care. Interestingly, the share of high-end cataract surgeries increased to 26% of total cataract surgeries (vs. 20% YoY), driving better realizations.

* The south and west regions saw 15-16% YoY growth in the number of surgeries performed in 3Q. The north and east regions also saw a pickup.

* Mature facilities (operationalized till FY22) posted 14% YoY revenue growth in YTD FY26. About nine facilities have been shifted from emerging to mature given the time since those facilities in operations.

* We raise our earnings estimates by 7%/4%/2% for FY26/FY27/FY28, factoring in enhanced efforts for high-end surgeries, healthy scale-up in north region facilities and robust growth in patients served in west/east regions. We value DAHL on an SoTP basis (30x EV/EBITDA for the surgery business, 15x EV/EBITDA for the opticals business, 13x EV/EBITDA for the pharmacy business, adj for a stake in Dr. Agarwal Eye Hospital/Thind hospital) and arrive at a TP of INR565.

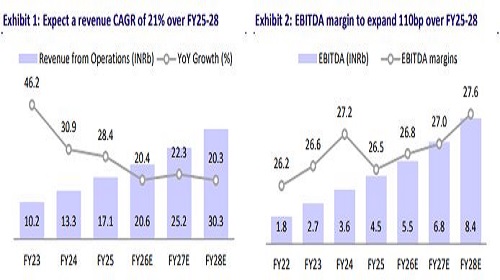

* We expect a CAGR of 21%/23%/42% in revenue/EBITDA/PAT over FY26-28. We believe DAHL is well positioned for stable growth momentum on the back of increased market share and facility additions. Maintain BUY.

Margin expansion drives robust earnings growth

* 3Q revenue grew 23% YoY to INR5.3b (in line).

* EBITDA margin expanded 180bp YoY to 27.2% (our estimate: 26%), driven primarily by lower raw material costs (down 40bp YoY as % of sales), employee expenses (down 10bp YoY, and other expenses (down 130bp YoY).

* Consequently, EBITDA grew 31.5% YoY to INR1.4b (our estimate: INR1.3b).

* PAT after minority interest came in at INR337m, up from INR187m in 3QFY25.

* For 9MFY26, revenue/EBITDA/PAT grew 21%/27%/97% YoY, driven by facility expansion and operational efficiencies.

Network expansion and higher surgical volumes drive growth

* Geography-wise, India business rose 23.1% YoY to INR4.8b (91% of total revenue), while international revenue grew 22.4% YoY to INR499m (9% of total revenue).

* Mature facilities reported 37.8% YoY growth to INR4.1b (76% of revenue), partly due to a shift of nine facilities to the mature category, all added to the surgical sub-category.

* Vintage facilities (up to FY22) grew 14.2% YoY in 9MFY26.

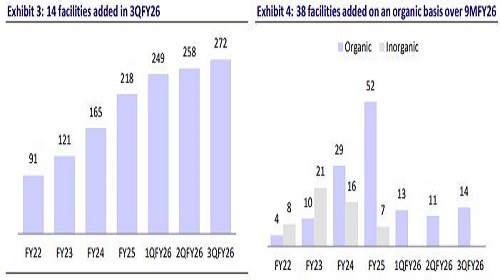

* DAHL added 38/14 new centers during 9MFY26/3QFY26, expanding its network to 272 facilities. The number of surgeries performed in 9MFY26 increased 11.6% YoY to 238,283.

* Service sales accounted for 78.8% of total revenue, whereas product sales contributed 21.2% in 9MFY26.

Highlights from the management commentary

* Management highlighted steady growth in patient footfalls, with daily walk-ins increasing to nearly 10k patients (vs. 8k YoY), supported by a stronger brand recall and a wider geographic reach.

* The company expanded its network to 253 facilities across 148 cities, with 14 new greenfield facilities commissioned during the quarter, and a total of 38 facilities added in 9MFY26.

* High-end cataract surgeries accounted for 26% of total cataract procedures in 9MFY26 (vs. 20% YoY), with robotic (femto) cataract surgeries recording strong YoY growth after the addition of new robotic systems.

* Management has reiterated its continued focus on premiumization through a higher adoption of advanced cataract, refractive (SMILE), retinal, and corneal procedures, supported by ongoing investments in advanced surgical technologies.

* Same-store sales growth remained healthy, supported by a combination of patient volume growth, improved conversion rates, and increasing contribution from premium procedures rather than price-led growth.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)