Buy Castrol (India) Ltd for the Target Rs. 250 by Motilal Oswal Financial Services Ltd

Volume growth remains robust

* Castrol’s 4QCY25 EBITDA/reported PAT missed our estimates by 10%/17%. Volume grew 8% YoY to 63.7m lit and EBITDA margin contracted 230bp YoY. The company recognized incremental obligations of INR225m related to new labor codes. Adjusted PAT was 12% below our estimate at INR2.6b.

* Management highlighted that it continues to focus on brand building, widening the distribution network, and launching new products, all of which we believe will drive volume growth and market share expansion. Management has maintained its volume growth guidance of 1.5x-2x market volume growth, with EBITDA margin guidance of 21-24%.

* Castrol has always enjoyed a strong brand legacy, and we are confident in its ability to maintain profitability through an improved product mix, stringent cost-control measures, and the launch of advanced products that command better realization. We reiterate our BUY rating with a TP of INR250.

EBITDA misses estimate in 4Q

* 4QCY25 revenue came in at ~INR14.4b (in line, up 6% YoY).

* Volume grew 8% YoY to 63.7m lit (in line).

* EBITDA came in 10% below our estimate at INR3.7b (down 2% YoY).

* EBITDA margin contracted 230bp YoY.

* Reported PAT came in 17% below our estimate at INR2.4b.

* The company recognized incremental obligations of INR225m related to new labor codes. Adjusted PAT was 12% below estimate at INR2.6b.

* Other income came in above our estimate.

Other key highlights:

* Castrol expanded its footprint and strengthened market presence:

* National distribution increased to ~150,000 outlets, with the Auto Care portfolio available across e-commerce, modern trade, and 67,000+ physical outlets.

* The service network has been scaled up to 750+ Castrol Auto Service centers, ~33,000 independent bike workshops, and ~11,500 multi-brand workshops.

* Rural distribution has expanded to ~40,000 outlets and ~500 Rural Service Express, delivering stable double-digit growth.

* Castrol signed strategic agreements with Triumph Motorcycles (Castrol POWER1) and VinFast Auto India to support EV aftersales through select Castrol Auto Service workshops.

* Castrol is building momentum through new launches and localization:

* In CY25, Castrol launched and localized ~20 products across automotive, industrial, and speciality segments.

* New launches across automotive and industrial segments included Hysol SL 20 XBB, Alusol SL 41 XBB/5505, Spheerol 40K/SM 00, Radicool, and Transmax.

* Castrol MAGNATEC was upgraded to the latest API SQ specifications.

* The Auto Care portfolio was expanded with mechanic care solutions, an Allin-One Helmet Cleaner, and an Aesthetic Care range.

Valuation and view

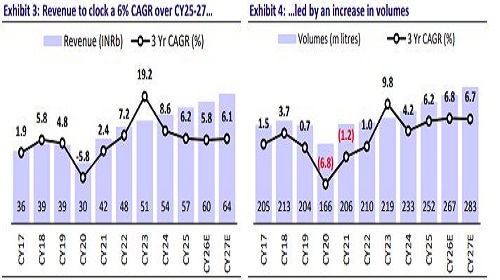

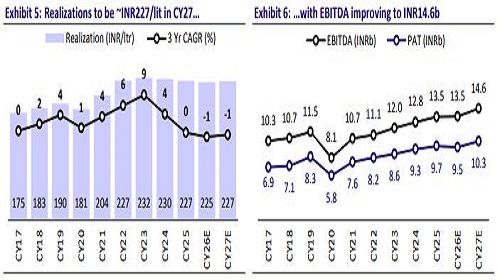

* Our EBITDA margin assumptions are already within the company’s guided range of 21-24%. Further, we build in a 6% CAGR in volumes over CY25-27, primarily driven by strong growth in industrial and rural segments. The stock currently trades at 18.1x CY27E EPS with 5% dividend yield and ~50% RoE/RoCE over CY26-27.

* We value the stock at 24x Dec’27E EPS to arrive at our TP of INR250. We reiterate our BUY rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412