Buy Signature Global Ltd for the Target Rs. 1,023 by Motilal Oswal Financial Services Ltd

Muted market conditions lead to a miss on guidance

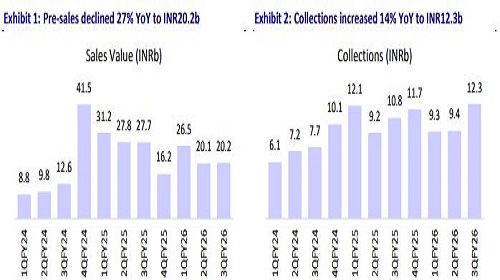

* Signature Global (SIGNATUR)’s presales of INR20.2b declined 27% YoY/were flat QoQ (42% below our estimate) for 3QFY26. It achieved presales of INR67b (down 23% YoY) for 9MFY26.

* Management cited the soft market environment as the primary reason for the miss on its INR127b guidance. However, the company is now prioritizing efforts to recover and meet its FY25 presales target. SIGNATUR launched two projects in 9MFY26: 1) Cloverdale (Jun’26) and Sarvam (Dec’26).

* Area sold during the quarter was 1.4msf, down 42% YoY/up 7% QoQ (38% below our estimates). In 9MFY26, volumes were 4msf, down 36% YoY.

* Average sales realization stood at INR14,028/sqft, up 28% YoY/down 6% QoQ (6% below our est.). In 9MFY26, realizations were INR15,182/sqft, up 21% YoY.

* Total units sold in the quarter were ~408, down 73% YoY and 27% QoQ. In 9MFY26, units sold were 1,746, down 51% YoY.

* Collections were higher by 14% YoY and 31% QoQ to INR12.3b for 3QFY26 (31% below our estimate). However, collections at INR31b were flat YoY for 9MFY26. ? In 9MFY26, the company acquired a total of 2.3msf of land in Sohna.

* Debt mounted to INR10.2b in 3QFY26 from INR9.7b in 2QFY26. It increased by INR1.4b from FY25. However, management is confident to be back on the growth path guided by the good collections in the future.

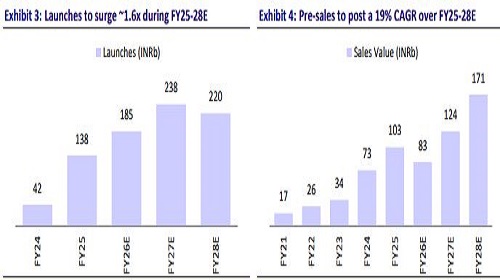

* SIGNATUR’s project pipeline remains strong, comprising 21msf of recently launched projects, 20.7 msf of upcoming developments, and 13.8msf under ongoing construction, all scheduled for execution over the next 2–3 years.

* P&L performance: In 3QFY26, the company reported revenue of INR2.8b, down 66%/16% YoY/QoQ (77% below estimate). In 9MFY26, revenue was at INR14.9b, down 25% YoY.

* SIGNATUR’s operating loss stood at INR632m vs. a profit of INR135m YoY. In 9MFY26, operating loss was INR1.0b vs. a profit of INR7m YoY.

* Adj. loss after tax in 3QFY26 was INR453m vs. a profit of INR291m YoY. In 9MFY26, loss after tax stood at INR578m vs. a profit of INR400m YoY.

Key highlights from the management commentary

* In 9MFY26, presales stood at INR67b, driven by sales of 4.4msf across 1,746 units with an average realization of INR15,182/sft and a ticket size of INR38m. The 3QFY26 presales were INR20b, down 27% YoY, and guidance was revised to match FY25 vs. the INR127b target earlier.

* Collections reached INR31b in 9MFY26 (~50% of guidance), fueled by ongoing projects, while 3QFY26 collections were strong at INR12.3b, up 32% QoQ and 14% YoY, with acceleration expected in 4QFY26.

* The company launched 6.8msf worth INR106b across Cloverdale (Sector 71) and Sarvam (Sector 37D), with Sarvam selling 318 of 800 units (~40%) since Dec-2025.

* An additional 2–3 msf worth INR45–50b is planned for launch before year-end, taking the total FY26 launch value above INR150b vs earlier guidance of INR170b.

* Over the last 24 months, 21msf worth INR330b has been launched, with another 21msf pipeline valued at INR350–400b planned over the next 8–10 quarters.

* Operating surplus of INR8.6b in 9MFY26 was utilized towards INR6.7b in land, INR2.7b in debt servicing, and INR0.6b in approvals. These activities led to a rise in net debt of INR1.4b.

* Total debt rose to INR10.2b in 3QFY26, with management targeting FY26 net debt below 0.5x projected surplus.

* The company continues to focus on middle-income and premium housing, with Dwarka Expressway, SPR, and Sohna seeing sustained traction from HNIs and premium buyers.

Valuation and view

* We cut our estimates based on weak operational and financial performance. Further, management has also hinted at the miss on its FY26 presales guidance of INR127b. It is working to meet its FY25 presales number of ~INR102.9b.

* However, SIGNATUR is preparing for multiple premium project launches, which we expect to support a 19% bookings CAGR over FY25-28E, aiding a gradual recovery in growth.

* We have valued the current residential portfolio by discounting the cash flows from all projects and accounting for the recent BD as well as potential land investments.

* We reiterate our BUY rating with a revised TP of INR1,023 (earlier INR1,385), indicating a 16% upside potential.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412