Buy Sobha Ltd for Target Rs.1,840 by Choice Institutional Equities

Pipeline Visibility Steering Growth

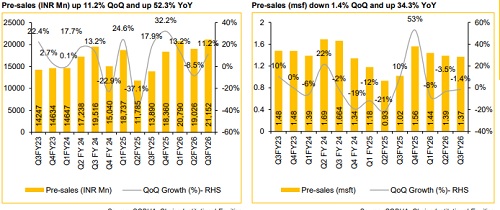

Achieved historic pre-sales, expands presence in Mumbai Sobha Ltd. delivered a strong operational performance in Q3FY26, led by record pre-sales of INR 21.2 Bn, driven by robust demand, higher realisation and new project launches, including its entry into the Mumbai market. While revenues and profitability declined due to delay in getting OC for completed projects, collections grew strongly YoY. With a solid launch pipeline and a strengthened balance sheet, the management remains confident of sustaining growth.

Robust pipeline in FY26 and FY27 will drive pre-sales growth: Management is confident of achieving pre-sales growth of 35% YoY to INR 85 Bn in FY26 (9MFY26 pre-sales are up 37.3% at INR 60,968 Mn) and aims to achieve INR 100 Bn pre-sales in FY27E. SOBHA has launched 2.58 msf in 9MFY26 and plans to launch further 4.5 msf of projects in Q4FY26E. From its ongoing and completed projects, SOBHA expects to generate net cash flows of INR 90 Bn over the next 4–5 years, while future projects of 18 msf are projected to yield INR 70 Bn over the next 5–6 years.

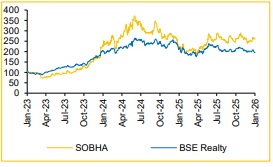

Expanding into new geographies: SOBHA is gradually expanding its presence beyond the Southern market. The company has already made an impressive start in the NCR and also started investing in new geographies, such as Pune and Hyderabad with increasing presence in Kerala in the recent past. In Q3FY26, it started penetrating the MMR market with the phase 1 launch of SOBHA Inizo at Sewri-Parel.

Robust balance sheet to support future pipeline: SOBHA had raised INR 20 Bn through rights issue, dated 12 June 2024, which will be used for funding certain project-related expenses for ongoing and forthcoming projects, capex, acquisition of land parcels and partial debt payment. Despite higher land prices across Tier-I and Tier II cities, we believe SOBHA has the execution wherewithal to generate over 30% project-level EBITDA.

Valuation: We maintain our BUY rating on SOBHA with a TP of INR 1,840/sh, factoring in the residential business with strong pipeline, commercial rental, contract & manufacturing business, as well as the land bank.

Risks: A broad-based slowdown in the domestic economy and delay due to legal and regulatory issues.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

.jpg)