Neutral JSW Cement Ltd For Target Rs.137 by Motilal Oswal Financial Services Ltd

Strong North India capacity ramp-up Scaling capacity; GGBS franchise continues to strengthen

We interacted with the management of JSW Cement (JSWC) to understand the current demand trend, progress on the company’s expansion plans and recently commissioned capacities, Ground Granulated Blast Furnace Slag (GGBS business) growth and future opportunities, prevailing cost trends, and key cost reduction measures. JSWC management indicated a positive outlook on cement demand in the medium term, supported by strong demand from the infrastructure, real estate, and housing segments. While near-term cost pressures persist due to the West Asia crisis, the company is implementing internal cost measures (higher green power share and logistics cost optimization) to partly offset the impact. Further, it possesses a unique and highly differentiated GGBS franchise, supported by a dominant market share, strong customer relationships, and structural growth drivers linked to increasing RMC penetration. The newly commissioned integrated plant in Rajasthan is witnessing a healthy ramp-up, with the company’s products receiving strong acceptance in northern markets and commanding prices comparable to A-category brands. Management reiterated its highly ambitious yet structured capacity growth roadmap of ~46mtpa vs. 24.1mtpa currently. We maintain our EBITDA estimates for FY27/FY28. However, we raise EPS estimates by ~12-15% for FY27/FY28 due to lower depreciation and finance cost estimates. We reiterate our Neutral rating with a TP of INR137 (valuing the stock at 13x FY28E EV/EBITDA).

GGBS business: A structural competitive moat

* A key differentiator for JSWC is its dominant position in the GGBS segment, where it holds ~84% market share in India and has been instrumental in developing the category. GGBS is a B2B product widely used in Ready Mix Concrete (RMC) applications due to its superior strength, durability, and sustainability benefits. Unlike Portland Slag Cement (PSC), GGBS enables RMC producers to tailor concrete mixes to specific project requirements, environmental conditions, and soil profiles. Its high resistance to chloride penetration and chemical attacks makes it particularly suitable for coastal and marine infrastructure projects.

* The business benefits from several structural advantages, including:

1) Secured multi-year slag supply contracts from JSW Steel plants in South and West India, along with similar arrangements with JSW Steel and other steel producers in East India

2) Co-location of grinding units with JSW Steel plants in South and West India, reducing inbound logistics costs and ensuring supply security

3) Regulatory approvals for key infrastructure applications, driving higher customer acceptance of GGBS. Moreover, JSW Steel’s planned capacity expansion from ~40mtpa to over 75mtpa by FY31 is expected to significantly increase slag availability. This will likely support sustained volume growth, margin stability, and long-term profitability in the GGBS segment.

* JSWC has strengthened its GGBS franchise through a service-led approach, offering concrete testing, mix design, and technical advisory support to RMC customers. The upcoming capacity expansions at Vijayanagar and Dolvi (to be completed by FY29E) are largely GGBS-led, underpinned by the group's rising steel production capacity. Industry estimates suggest GGBS demand is likely to expand at a 14-15% CAGR over FY25-30, outpacing cement demand growth. JSWC’s dominant market position and continued customer acquisition strategy position it well to capture a meaningful share of this opportunity.

Valuation and view

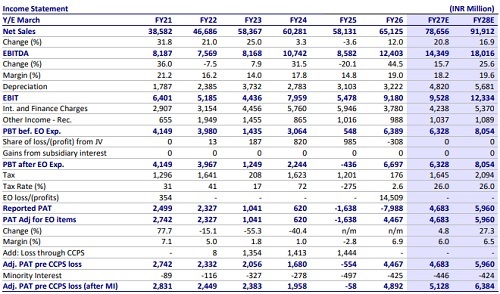

* JSWC delivered a resilient performance in FY26, supported by strong volume growth (up ~11% YoY) and higher profitability (EBITDA/t up ~31% YoY to INR915), led by better grey cement realizations, cost efficiencies, and positive operating leverage. The company’s net debt declined to INR35.8b in FY26 vs. INR40.7b in FY25, partly led by cash proceeds from IPO. * * We estimate a CAGR of ~19%/21%/14% in revenue/EBITDA/Adj. PAT over FY26- 28, driven by higher sales volume (~18% CAGR). EBITDA/t is estimated to reach INR872/INR948 in FY27/FY28 vs. INR915 in FY26. The company’s GGBS profitability remains higher, given the cost advantage and stable realization.

* Cumulative OCF is expected to increase to INR28.8b over FY27-28 vs. INR19.1b over FY25-26. The company’s capex is pegged at INR22.0b in FY27/FY28 (each). We estimate cumulative net cash outflow of INR15.4b over FY27-28 (given the aggressive expansions) vs. INR12.1b over FY25-26. Net debt is estimated to increase to INR60.6b by FY28 vs. INR35.8b in FY26. Net debt-to-EBITDA ratio is estimated to increase to 3.4x by FY28E vs. 2.9x in FY26.

* We maintain our EBITDA estimates for FY27/FY28. However, raise EPS estimates by ~12-15% for FY27/FY28 due to lower depreciation/ finance cost estimates. We value JSWC at 13x FY28E EV/EBITDA to arrive at our revised TP of INR137. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)