Buy Ipca Laboratories Ltd for the Target Rs 1,800 by Emkay Global Financial Services Ltd

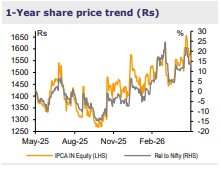

Ipca’s 4QFY26 EBITDA was ahead of our expectations (broadly in line with the consensus’). The beat was driven by higher overall sales, a marginally higher gross margin, as well as lower staff costs. The magnitude of gross margin and EBITDA margin expansion (ex-Unichem) was much higher (~330bps YoY) vs the reported figures. The top-line beat was primarily driven by higher generic sales (broad-based growth across markets, per the management). The commentary was positive on all fronts – double-digit growth outlook across segments (~12-13% consolidated sales growth in FY27; 10% growth in Unichem’s US portfolio), ~22% consolidated EBITDA margin (12-13% margin in Unichem), and a healthy US launch pipeline (Ipca + Unichem). Note that we had anyway not extrapolated Ipca’s recent gross margin performance, and our conservative consolidated EBITDA margin expansion assumptions (~170bps over FY26-28E) are largely a function of operating leverage gains in the standalone business and margin improvement in Unichem. We have, in the past, argued that with India formulations being a volume play, leverage gains from sustained volume-led, double-digit domestic growth will keep Ipca’s overall margin expansion targets within reach (~150bps per year on 10-12% topline growth). Despite concerns around the potential volatility in Ipca’s ex-India earnings, we note that the consensus’ FY27 EPS estimate has been remarkably stable over the last 2 years. We see a sharp price-value disconnect emerging post recent correction (even basis our conservative estimates). We broadly maintain our FY27/28 EPS estimates. We roll forward to Jun-28E earnings and introduce FY29 estimates. We retain BUY and raise our TP (now Jun-27) by ~6% to Rs1,800 from Rs1,700

Strong generics + branded performance; domestic formulation sales in line

Domestic formulations growth (12% YoY) was in-line, driven by acute as well as chronic outperformance. Growth in the branded business (14% YoY) was led by the CIS and African markets. Generics growth (39% YoY) was meaningfully ahead of expectations, aided by growth across various markets (EU, US, and Australia). Institutional sales declined 33% YoY (albeit ahead of our expectations) owing to ongoing funding pressures.

KTAs from the earnings call

1) Overall US sales (Ipca + Unichem) stood at ~Rs16bn in FY26 and witnessed a growth of ~14%. Unichem’s US business was flat in FY26 due to loss of market share in highvolume products. However, Unichem has started regaining market share and is expected to launch 5-6 products in the US in FY27.

2) Ipca is currently marketing eight products in the US, where it plans to launch an additional 6-8 products in FY27; it also has plans to launch 3-4 products per market in Europe and other generic markets.

3) The company aims to implement a 6-7% price hike in non-NLEM domestic products, to offset the higher raw material costs arising from an increase in packaging and solvent prices.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

2.jpg)