Neutral Bajaj Auto Ltd for the Target Rs. 9,070 by Motilal Oswal Financial Services Ltd

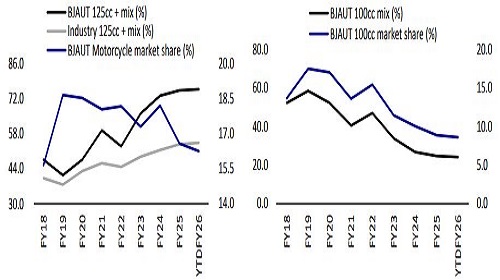

Loss in motorcycle share remains a key concern

We met with the management of Bajaj Auto (BJAUT) to understand the outlook for its key business segments. In the domestic motorcycle market, management looks to revive the lost market share, aided by new launches that include three Pulsar variants, a new 125cc model, and a few other premium models. Demand momentum is likely to sustain in the export markets due to healthy growth in the Latin American and Asian markets. In 2W and 3W EVs, BJAUT aims to achieve a leadership position on the back of another Chetak launch next year and the recently launched e-rik, Riki, respectively. BJAUT remains the only player to be on the verge of being EBITDA break-even in 2W EVs. Further, currency depreciation is likely to help drive the margin cushion in the coming quarters. We model a revenue/EBITDA/PAT CAGR of 12%/12%/11% for BJAUT. At ~24.1x/21.9x FY27E/28E EPS, BJAUT appears fairly valued. We reiterate our Neutral rating on the stock with a TP of INR9,070, based on 24x Sep27E core EPS.

Targets to regain its lost share, backed by new launches

Management targets to recover the lost share in domestic motorcycles on the back of a few new launches, which include: 1) the new 125cc commute motorcycle, which is likely to be launched in FY27E; 2) three Pulsar variant launches in Dec’25, Mar’25, and May’25; 3) intervention in the Dominar brand; 4) the 350cc Triumph variant; and 5) the recently launched KTM brands, which include Adventure, Super Moto, and Duke 160. We model BJAUT to post a 6.5% volume CAGR over FY25-27E.

Export momentum likely to be sustained

BJAUT has surpassed 200k units per month in exports recently, a feat achieved after 40 months. This too despite its key market, Nigeria, being at less than 50% of the peak. Latin America is driving growth, which has now emerged as the largest market for BJAUT. Management remains upbeat on the ramp-up in Brazil and Mexico, which are likely to help sustain the export momentum. While the demand momentum is likely to remain strong in exports, the recent currency depreciation will also provide a margin cushion for the company in the current quarter.

Gaining prominence in EVs

On the back of healthy demand for Chetak, BJAUT has already emerged as the second-largest EV player. Backed by the expected launch of a Chetak model next year, BJAUT targets to move to the leadership position in the segment. More importantly, BJAUT is the only player to be on the verge of being EBITDA positive in the 2W segment in Q2. In 3Ws, the recent launch of the e-rick, Riki, is expected to help drive growth in the coming quarters.

BJAUT would look to leverage synergy benefits post KTM buyout

After the KTM acquisition, BJAUT would now focus on the restructuring of the core operations. They would also look to leverage synergy benefits in manufacturing operations, the supply chain, and the distribution network. The company would plan to exit the bicycle business, cars, and other smaller brands and focus on the KTM and Husqvarna brands. Management has indicated that 1HCY26 will be the year of consolidation/restructuring, and from 2HCY26, one can observe operational benefits of these measures.

Valuation and View

While a recovery in exports and a healthy ramp-up of Chetak and 3Ws are key positives, market share loss in domestic motorcycles, particularly in the crucial 125cc+ segment, remains the key concern. While BJAUT has acquired a controlling stake in KTM under a lucrative deal, its effectiveness depends on how quickly it is able to turn around its operations, which will remain the key monitorable going forward. At ~24.1x/21.9x FY27E/28E, BJAUT appears fairly valued. We reiterate our Neutral rating with a TP of INR9,070, based on 24x Sep27E core EPS.

Targets to regain its lost share, backed by new launches

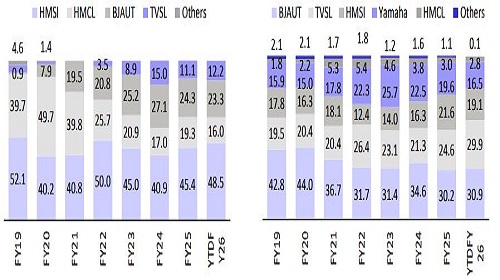

- BJAUT’s market share in the motorcycle segment declined from 18.5% in FY20 to 16.6% in FY25 and further down to ~16% for YTD’26.

- More importantly, it has lost share in both the 125cc segment as well as the 150- 250cc segments in the last couple of years.

- For instance, in the 125cc segment, its market share had peaked at 27% in FY24, which declined to 24.3% last year and further to 23.3% for YTDFY26. Similarly, in the 150-250cc segment, from a share of 34.6% in FY24, its share on a YTD basis now stands at 30.9%.

- The company’s loss of market share in its core 125cc+ segments has been a key concern for investors in the recent past.

- To address this, BJAUT is planning multiple model interventions going forward.

- In the 125cc segment, BJAUT is looking to launch a commute product. However, this is likely to be launched only in FY27.

- Further, BJAUT has indicated that it would look to refresh its entire Pulsar range in the coming months. The company has a variant launch in Pulsar each in Dec’25, Mar’26, and May’26.

- The Dominar is also likely to see some intervention in FY27.

- Further, BJAUT has indicated that they are at the moment absorbing the impact of the GST increase on >350cc 2Ws on its Triumph models. However, they are planning to launch a 350cc Triumph variant in FY27E.

- On the back of these initiatives, management hopes to regain its lost market share in the domestic motorcycle market. We expect BJAUT to post a 6.5% volume CAGR over FY26-28E.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

600-400.jpg)