Buy Devyani International Ltd for the Target Rs. 180 by Motilal Oswal Financial Services Ltd

Unchanged print; positive start to 2026

* Devyani International’s (DEVYANI) consolidated revenue grew 11% YoY in 3QFY26. India revenue was up 12% YoY, led by the Skygate acquisition and 13% YoY store expansion. KFC/PH saw same-store sales decline in 3Q, but the company reported SSSG in Jan’26 across brands, except PH.

* KFC revenue grew 6% YoY, aided by 14% store expansion, which was offset by a 2.9% decline in same-store sales. Pizza Hut (PH) revenue declined 6% YoY. Same-store sales declined 9.1% YoY. Franchisees brands’ (Costa Coffe, NYF, tealive, SK) revenue grew 9% YoY, with 1% YoY store additions. Vaango revenue rose 3%. Sky gate revenue was INR115m with 13 store addition.

* India ROM was up 5% YoY at INR1.3b, and margin contracted by 80bp YoY to 13.1%, owing to operating deleverage. KFC’s ROM contracted 40bp YoY to 16.8%, and PH’s ROM contracted 130bp YoY to 0.8%.

* International revenue grew 10% YoY to INR4.7b with ROM at INR810m (vs. INR714m in 3QFY25), and margin expanded 50bp YoY to 17.1%.

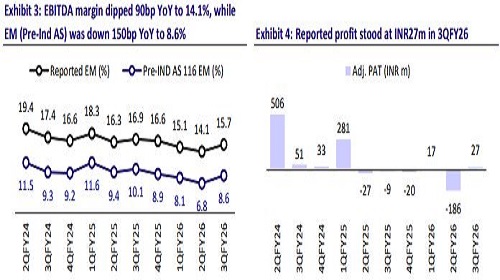

* Consolidated GP margin rose 20bp YoY and 110bp QoQ to 68.9 (est. 68.5%). EBITDA (pre-Ind-AS) margin was down 150bp YoY/up 180bp QoQ at 8.6%. Consol. RoM margin contracted 20bp YoY and 110bp QoQ to 68.9 (est. 68.5%).

* The weak unit economics is a big concern for QSR players, given fast store expansion. With expectation of urban demand recovery, we need to see if January trends are sustaining. Devyani–Sapphire merger is expected to unlock scale benefits and strengthen execution across brands and geographies (refer to our detailed merger note). The merger is expected to deliver recurring annual synergies of ~INR2.2b (mostly from FY29 onward), driven by lower PH operating costs, reduction in overall corporate overheads, and other operational efficiencies.

* We reiterate our BUY rating and value the entity at 25x Dec’27E EV/EBITDA (pre-Ind AS), implying a TP of INR180 per share.

Weak SSSG; change in key leadership

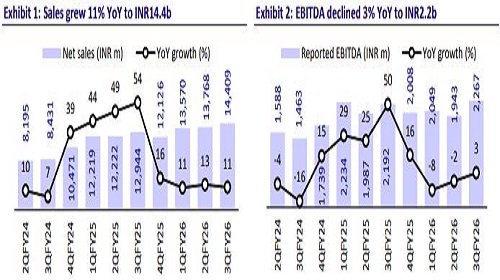

* Soft underlying growth trend continues: Consolidated sales grew 11% YoY to INR14.4b (est. INR 15.0b). India revenue was up by 12% YoY at INR9.8b (est. INR10.1b), supported by the Sky Gate acquisition and store addition. KFC sales grew 6% YoY to INR6.0b, while same-store sales declined 2.9% (est. -1.0%). PH sales declined 6% YoY to INR1.8b (est. INR1.9b). Same-store sales declined 9.1% (est. -2.5%). ADS of KFC was down 6% YoY at INR90k, and PH ADS dipped 11% YoY to INR31k.

* Network expansion by 95 stores: It added a total of 95 stores in 3QFY26 to reach 2,279 stores. The store additions or closures in KFC/PH/CC/own brands/International are 54/18/-13/17/20, taking the total store count for KFC/PH/CC/own brands/International to 788/639/211/218/402.

* Pressure on margins continues: Gross profit grew 12% YoY to INR9.9b (est. 10.3b). Gross margins rose 20bp YoY and 110bp QoQ to 68.9 (est. 68.5%). Reported EBITDA increased by 3% YoY to INR2.3b (est. INR2.4b). Consol. EBITDA margins were down 120bp YoY/up 160bp QoQ at 15.7% (est. 15.7%). Consol. ROM was up 8% YoY at INR2.0b. Margin contracted 40bp YoY while rose 220bp QoQ to 13.9%. Pre Ind-AS EBITDA declined 5% YoY to INR1.2b. Margin fell 150bp YoY to 8.6%. There is an exceptional item of INR215mn related to the one-time impact of labor codes.

* APAT stood at INR27m vs. a loss of INR9m in 3QFY25.

Key leadership changes

* Devyani has announced the appointment of Mr. Manish Dawar as President & CEO, effective 1st Apr’26. Mr. Dawar is currently the CFO and Whole-Time Director of the company and has over 30 years of experience across leading companies such as HUL, Vodafone India, Vedanta, Reckitt Benckiser, and Reebok. At Devyani, he has played a key role in the company’s growth, including the successful IPO, Thailand business acquisition, acquisition and turnaround of Sky Gate Hospitality (Biryani by Kilo, Goila Butter Chicken), and the proposed merger with Sapphire Foods. Subject to approvals, Mr. Dawar will also lead the merged entity of Devyani and Sapphire as President & CEO.

* Mr. Virag Joshi, current President & CEO, will continue on the Board as a NonExecutive Director and will support the company with his strategic guidance.

* The company has also appointed Mr. Anupam Kumar as CFO. He was earlier EVP – Finance and has over 20 years of experience, including stints at Vedanta and Walker Chandiok & Co LLP.

* Mr. Neeraj Tiwari has been appointed as CTO. He brings in 19 years of experience in building digital platforms and has earlier worked with Americana Group, Jubilant FoodWorks, and Zee Entertainment.

Highlights from the management commentary

* Devyani reported positive SSSG across all brands in January, except Pizza Hut, where losses continue to moderate. Management indicated that steady momentum through the quarter could provide a strong base for medium-term growth.

* The company has initiated the turnaround of Pizza Hut by rationalizing lossmaking stores. New store openings will largely be limited to offset closures, enabling better utilization of existing assets and lowering capex intensity.

* The Biryani by Kilo brand achieved EBITDA breakeven ahead of management guidance, indicating improving unit economics.

* For the Devyani-Sapphire merger, applications for stock exchange approvals have been submitted, and the CCI filing is expected shortly. Management reiterated that it does not expect any material deviation from the previously guided 12–15-month merger timeline.

Valuation and view

* We largely maintain our EBITDA estimates for FY27 and FY28.

* Management remains committed to improving ADS and profitability across the existing network across brands and will adopt a more cautious approach to future store openings for PH.

* The merger of Devyani and Sapphire is expected to unlock meaningful scale benefits, improve unit economics through operating leverage and revised commercial terms, and enhance execution across brands and geographies.

* The merger is expected to deliver recurring annual synergies of ~INR2.2b, driven by lower Pizza Hut operating costs, reduction in overall corporate overheads, and other operational efficiencies. As per the company, ~60% of synergies (~INR1.1b) will be realized in the first year after the merger and the full benefits (INR2-2.25b) from the second year onward. We estimate an EBITDA gain of ~INR500m in FY28, considering weak QSR industry performance and any delay in occurring synergy benefits.

* We value the entity at 25x EV/EBITDA (pre-IND AS) on Dec’27E and arrive at a TP of INR180. Maintain BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412