Buy Emami Ltd for the Target Rs. 650 by Motilal Oswal Financial Services Ltd

Steady show; positive commentary on growth recovery

* Emami’s consolidated revenue grew 10% YoY in 3QFY26 (in line), backed by a favorable winter season. Emami saw a sequential improvement following the GST 2.0-related trade disruptions in the early part of 3Q. Domestic business grew by 11% YoY with 9% volume growth. International business revenue rose 9% YoY, led by steady performance in the SAARC and CIS regions. Management expects its summer portfolio channel loading to start by Feb end. Emami aims to achieve high-single-digit to low-double-digit revenue growth in the near term.

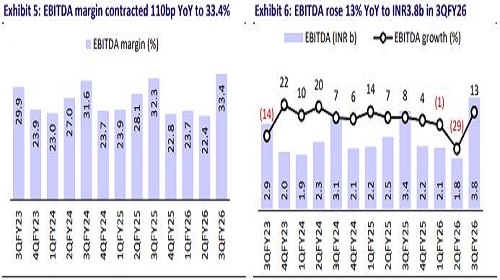

* While GM saw a marginal expansion of 40bp to 70.6% (in line), EBITDA margin expanded 110bp YoY to 33.4% (in line). We expect ~26.5% EBITDA margin for FY26 and FY27.

* Given a resilient performance in rural markets and Emami’s own initiatives related to distribution, new launches, and marketing spends, it is expected to sustain revenue growth. Emami plans to prioritize rural markets with more focus on LUP mix in FY27. We believe a healthy season and a broadbased consumption recovery, coupled with comfortable valuation, bode well for Emami. We reiterate our BUY rating with a TP of INR650 (based on 30x Dec’27E EPS).

In-line performance; volume up 9%

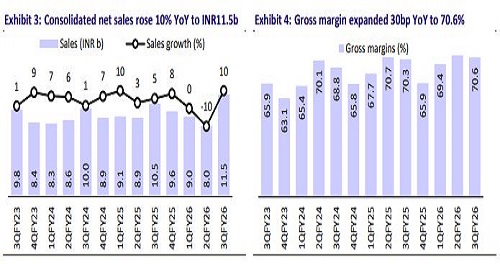

* Double-digit sales growth: Consol. net sales rose 10% YoY to INR11.5b (est. INR11.6b). Domestic business revenue grew 11% YoY, backed by 9% volume growth. A favourable winter season supported stronger offtake across the winter portfolio and health supplements. All brands registered healthy performance during the quarter. International business revenue grew 9% YoY, led by steady performance in the SAARC and CIS regions.

* Healthy growth across brands: All major brands saw healthy performance during the quarter. Backed by strong growth in the winter portfolio, BoroPlus grew 16% YoY (on a base of 20%). Pain management grew 8% and healthcare range grew 7%. Following a revamp, Kesh King grew 10% after nine quarter of declining growth trajectory. Strategic subsidiaries delivered robust growth of 31% in 3QFY26 and management expects to sustain the growth momentum going ahead.

* EBITDA margin in line with estimates: Gross margin expanded marginally by 30bp YoY to 70.6% (est. 70.4%). Employee expenses/ad spending rose 8%/9%, while other expenses grew 5% YoY. EBITDA margin expanded 110bp YoY to 33.4% (est. 33.1%).

* Healthy PAT growth of 13% YoY: EBITDA rose 13% YoY to INR3.8b (est. INR3.85b). PBT (before exceptional) grew 16% YoY to INR3.5b (est. INR3.5b). PBT (adjusted for new labour code impact) grew 13% YoY to INR3.4b. APAT rose 13% YoY to INR3.4b (est. INR3.3b).

* In 9MFY26, revenue was flat, while EBITDA/PAT dipped 4%/1%.

* Emami has declared an interim dividend of INR6/share with 10th Feb’26 as the record date.

Key highlights from the management commentary

* All major brands registered healthy performance in 3QFY26. Post GST 2.0, the blended price cut for Emami at portfolio level is ~8%.

* Summer product portfolio channel loading will start from Feb end.

* Given a strong performance in rural markets, Emami will increase its focus on smaller SKUs in FY27, with more focus on shampoo sachets, Smart and Handsome, and other small SKUs.

Valuation and view

* Given an increase in ETR guidance, we cut our EPS estimates by 4% for FY27-28.

* Emami’s core categories are niche, which have been facing slow user addition over the last five years. That said, Emami is focusing on rebranding its portfolio to reduce the seasonal dependence. Moreover, Emami continues to strengthen its distribution reach predominantly in alternate channels (MT, e-com, and QC). Emami will prioritize rural markets with more focus on LUP mix in FY27.

* We reiterate our BUY rating with a TP of INR650 (based on 30x Dec’27E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412