Buy Emami Ltd for the Target Rs. 675 by Motilal Oswal Financial Services Ltd

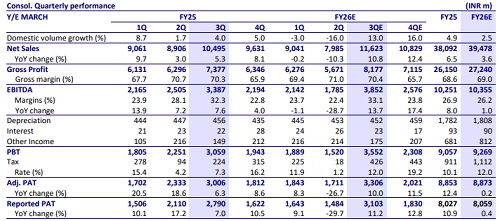

* We model 11% revenue growth and 13% volume growth, led by the loading of winter products and normalization of trade post-GST implementation.

* Kesh King has seen improvement, and the product relaunched in 2Q will also contribute to the growth.

* GM is expected to flat YoY at 70.4% and EBITDA margin is likely to expand 80bp YoY to 33.4% led by operating leverage.

* International business expected to deliver 10% revenue growth in 3Q.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Cement Sector Update : Earnings downgrade behind; cost reversal to begin from exit-2Q by Mot...