Buy Devyani International Ltd for the Target Rs. 180 by Motilal Oswal Financial Services Ltd

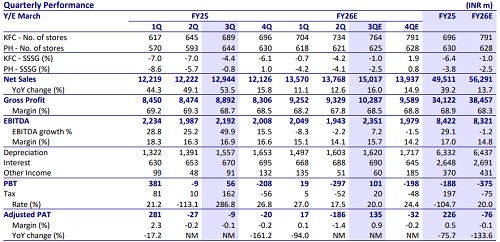

* Demand remained soft in 3QFY26. PH same-store sales are likely to decline by 2.5%. We model 4 store additions and 1% revenue decline for PH.

* We model 9% revenue and 2% SSSG in Costa Coffee. International business revenue is expected to grow by 14%.

* KFC revenue expected to grow 9% YoY, led by store additions. We model 30 store additions (+11% YoY), while same-store sales may decline by 1% on a negative base.

* EBITDA margin pressure will persist due to lower demand and negative operating leverage.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motila...