Buy Restaurant Brands Asia Ltd for the Target Rs. 120 by Motilal Oswal Financial Services Ltd

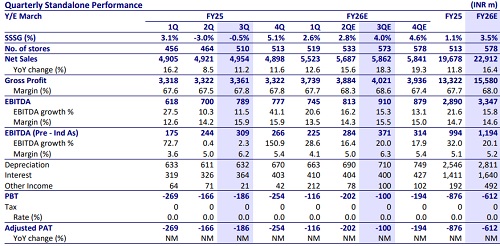

* The India business is expected to grow 18% YoY. We build 4% SSSG as there is not much improvement in the underlying demand.

* Demand in Indonesia remained moderate, and we model 4% revenue growth.

* We model 40 store additions in India, taking the store count to 573 (12% YoY). We expect 80bp improvement in GP margin to 68.6% on stable RM prices and EBITDA Margin to be contracted 40bp YoY to 15.5% on account of some operating deleverage.

* ADS is expected to remain flat YoY at ~INR114k.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motila...