Buy Emami Ltd for the Target Rs 525 by Motilal Oswal Financial Services Ltd

Weak summer portfolio; miss on earnings

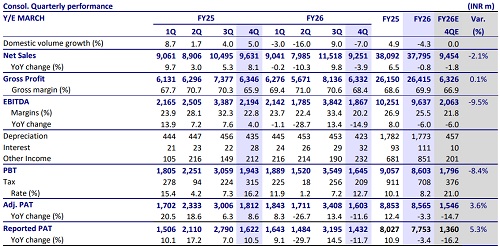

* Emami’s (HMN) consolidated revenue declined 4% YoY in 4QFY26 (below), impacted by weak demand for summer portfolio, along with geopolitical disruptions in West Asia. Domestic revenue contracted 3% YoY, with a 7% volume dip. Summer portfolio declined 22%, with talcum powders declining 40% YoY. Non-summer portfolio delivered healthy 11% growth, with a 7% volume growth. International revenue declined 5% YoY. Strategic subsidiaries delivered robust growth of 34% in 4QFY26, and management expects growth momentum to sustain going ahead. D2C brands now contribute 9% to the domestic business (5% in FY23).

* GM expanded 230bp YoY to 68.4%, backed by disciplined cost management and calibrated pricing actions. Meanwhile, EBITDA margin contracted 260bp YoY to 20.2% (below) due to operating deleverage and higher ad spends. We expect ~26% EBITDA margin for FY27 and FY28.

* Summer portfolio is likely to witness a recovery in growth from 1Q onwards, supported by a steady onset of the season and a favorable base. Additionally, the new-age portfolio is expected to provide further growth levers over the coming years. The company’s market leadership in its core portfolio also provides a better ability to pass on RM pressure, limiting EBITDA margin risk in FY27 relative to peers. With comfort in valuation (21x FY27), we reiterate a BUY rating with a TP of INR525 (25x on FY28 EPS).

Key highlights from the management commentary

* The summer portfolio declined 22%, with talcum powders declining 40% YoY. Talcum powder contributed INR3b of sales in FY26 (~10% of total sales).

* Due to disruptions and rising costs, competitive intensity from unorganized players has eased somewhat.

* HMN highlighted that it reduced trade receivables by over INR1b in FY26, implying a 10-day improvement in the working capital cycle.

* Management indicated that new-age channel margins are now closer to those in general trade.

* HMN expects the international business to stabilize by June and witness doubledigit growth by 2QFY27.

* Strategic subsidiaries delivered robust growth of 34% in 4QFY26, and management expects growth momentum to sustain going ahead.

Valuation and view

* We largely maintain our EPS estimates for FY27 and FY28.

* HMN is focusing on rebranding its portfolio to reduce seasonal dependence. Its strategic subsidiaries are expected to grow in their thirties. Moreover, the company continues to strengthen its distribution reach predominantly in alternate channels (MT, e-com, and QC).

* We believe a healthy season, coupled with a comfortable valuation, bodes well for HMN. We reiterate our BUY rating with a TP of INR525 (based on 25x Mar’28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412