Financials Banking Sector Update : Reconciling banking business updates with systemic data by Motilal Oswal Financial Services Ltd

Implied bias softer on SBIN’s Q1FY27 business growth, mainly deposits

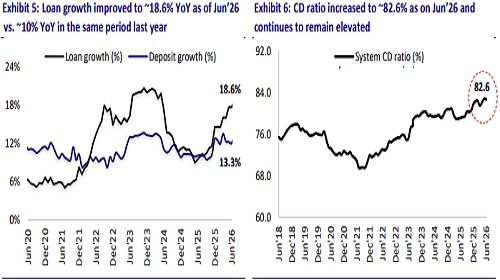

* System credit growth stood at 18.6% YoY/2.7% QoQ as of 30th Jun’26, with the outstanding base increasing by INR5.6t to INR219t in 1QFY27, as against 9.7% YoY/1.3% QoQ in 1QFY26 (increase of INR2.4t), indicating a sharp improvement.

* The 1QFY27 business updates across our coverage universe showed large private banks (16.2% YoY/3.1% QoQ) outperforming PSU banks (15.1% YoY/1.7 QoQ), gaining incremental credit market share. Within our coverage universe: HDFCB (3.4% QoQ), KMB (3.3% QoQ), and CBK (4.5% QoQ) outperformed the system, while most PSBs underperformed.

* Based on our reconciliation of the 1QFY27 business updates with the systemic business data, we see a potential marginal miss on ICICIBC’s credit growth and a relatively larger miss of 80-100bp on SBIN’s credit growth estimate, compared to our 1QFY27 preview estimates published earlier. In our preview note, we had estimated sequential credit growth of 4.1% for ICICIBC and 3.1% for SBIN.

* Deposit growth stood at 13.3% YoY/1.2% QoQ as of 30th Jun’26, with outstanding base increasing by INR3.1t (similar to 1QFY26) to INR265t. PSBs (under coverage) underperformed with 10.0% YoY/0.6% QoQ growth, while large private banks delivered a robust 15.3% YoY/2.0% QoQ growth. Consequently, we see downside risk to our deposit growth estimates for ICICIBC (3.2% QoQ) and SBIN (2.9% QoQ).

* Mid-sized banks within our coverage universe reported credit growth of 13.1% YoY/3.3% QoQ, indicating a strong sequential pick-up. Accordingly, we believe our estimate of 3.3% QoQ growth for FB is broadly in line.

* We expect the banking sector’s earnings to rebound with ~15% CAGR over FY26-28, fueled by ~15% CAGR in net interest income (NII). Private banks, with an anticipated earnings CAGR of ~20%, are likely to outperform PSBs, which are expected to post an earnings CAGR of ~10%. Our top ideas are ICICIBC, HDFCB, SBIN, AUBANK, and RBK.

Reconciliation implies a negative bias on SBIN’s 1QFY27 credit growth

System credit growth remained robust at 18.6% YoY/2.7% QoQ, in line with the business updates covering ~67% of the banking universe. Reconciliation of the 1QFY27 business updates indicates residual growth of INR1.9t QoQ, compared to our combined credit estimate of INR2.2t QoQ for ICICIBC, SBIN, and FB (forming ~31% market share). Given HDFCB and KMB outperformed the system with a 3.4% QoQ and 3.3% QoQ growth, respectively, we expect a marginal miss on our 1QFY27 growth estimate of 4.1% QoQ for ICICIBC. PSU banks (under coverage) largely missed our estimates, reporting credit growth of 15.1% YoY/1.7% QoQ. Consequently, we believe our 1QFY27E of 3.1% QoQ for SBIN carries a relatively higher negative bias of 80-100b.

Downside risk to deposit mobilization for SBIN and ICICIBC

Deposit growth of 13.3% YoY/1.2% QoQ continues to lag credit growth. Large private banks gained incremental market share, posting 15.0% YoY/2.0% QoQ growth, with AXSB posting a robust print of 2.8% QoQ. PSBs (under coverage) witnessed muted deposit growth of 10.0% YoY/0.5% QoQ, significantly underperforming the system. Consequently, we see downside risk to our 1QFY27 deposit growth estimates for ICICIBC (3.2% QoQ) and SBIN (2.9% QoQ).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Cement Sector Update : Earnings downgrade behind; cost reversal to begin from exit-2Q by Mot...