Buy Godrej Agrovet Ltd for the Target Rs. 700 by Motilal Oswal Financial Services Ltd

Strong palm oil margins and recovery in CP drive performance

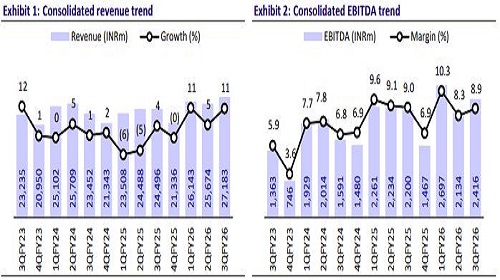

In-line operating performance

* Godrej Agrovet (GOAGRO) reported a healthy operating performance (EBIT up 13.7% YoY) in 3QFY26, primarily led by continued strong growth in the palm oil business (EBIT up 25%). The crop protection (CP) business witnessed a 67.5% YoY rise in EBIT, led by a recovery in Astec (both CDMO and enterprise performed well). The poultry business also witnessed an increase in EBIT by 94.5% in 3Q. The Animal Feed (AF) business posted a marginal EBIT growth of 5% YoY, while the Dairy business’s EBIT declined 49% YoY.

* The growth trajectory is expected to remain healthy across key segments. Cattle feed volumes remain strong, driven by premiumization, while palm oil FFB growth is expected to remain healthy over the long term, supported by improving OER and the ramp-up of downstream value addition. The outlook for the crop protection business also remains positive, led by new product launches in standalone crop protection and a steady recovery in Astec (broad-based).

* Hence, we broadly retain our FY26/FY27/FY28 EBITDA estimates. We reiterate our BUY rating on the stock with an SOTP-based TP of INR700.

Healthy quarter led by broad-based revenue growth

* Consolidated revenue stood at INR27.2b, up 11% YoY (est. in line). EBITDA margin contracted 10bp YoY to 8.9% (est. 9.5%), led by an increase in employee costs (stood at 6.1% vs 5.7% in 3QFY25) and other expenses (stood at 11.0% vs 10.9% in 3QFY25). Meanwhile, gross margins expanded 40bp YoY to 26.0%. EBITDA stood at INR2.4b, up 9.8% YoY (est. in line). Adjusted PAT grew ~24% YoY to INR1.4b (est. of INR1.6b).

* AF: Revenue inched up 1.9% YoY to INR13b, while margins expanded 20bp to 6.2%. Volumes grew ~12% YoY, which was partially offset by a 9% dip in realizations (product mix change).

* Palm Oil: Revenue grew ~29% YoY to INR6.3b, led by higher realizations in palm kernel oil (PKO, up ~24%), while realizations for crude palm oil (CPO) declined ~7%. FFB arrivals rose 16% YoY. However, EBIT margin contracted 60pp YoY to 23.1%. EBIT grew ~25% YoY to INR1.4b. The OER improved to 21% in 3QFY26 vs 19.5% in 2QFY26 and 20.7% in 3QFY25.

* CP: Consolidated CP revenue grew 34% YoY to ~INR2.6b, with standalone CP revenue/Astec growing 37%/33% YoY. Astec’s revenue grew on account of robust volume growth in both the enterprise & CDMO categories. Consolidated CP EBIT grew 67.5% YoY to INR200m, with standalone CP EBIT declining 3.3% YoY to INR260m. Growth was led by a strong reduction in Astec’s operating loss to INR61m vs. INR151m in 3QFY25.

* The Dairy business revenue grew 2.7% YoY to INR3.8b, while EBIT declined ~49% YoY to INR47m, on account of higher milk procurement prices and a deficit in revenue. The Poultry and Processed Food business’s revenue stood at INR2.1b (flat YoY), while EBIT was INR127m (up 94% YoY), standing at 6% in 3QFY26 compared to 3% YoY to 3QFY25.

* For 9MFY26, GOAGRO’s revenue/EBITDA/adj. PAT grew 9%/8%/9% to INR79b/INR7.2b/INR3.9b.

Highlights from the management commentary

* Guidance/Outlook: GOAGRO’s near-term outlook remains strong. Management has guided for mid-teen growth in cattle feed, palm oil FFB growth of 12–15% supported by improving OER and downstream ramp-up, and crop protection margins sustaining at 28–30%. Astec targets EBITDA breakeven in FY26 and 15– 20% revenue growth in FY27, while poultry and dairy continue to shift toward higher-margin branded value-added products.

* Astec: Triazole chemistry has normalized, with margins and volumes recovering as excess inventory has cleared amid improving demand. The company is undertaking strategic initiatives, such as obtaining its own registrations. Three approvals have already been secured in Europe and two in Brazil, with additional registrations expected over the next 12-18 months.

* Palm oil: Coconut prices have risen sharply due to supply constraints and now trade at a substantial premium to PKO. With strong demand and limited scope to increase coconut oil production, elevated PKO prices are expected to persist.

Valuation and view

* GOAGRO’s near- to mid-term outlook remains constructive, led by strong momentum in branded cattle feed, steady palm oil volume growth with improving OER, rising value-added poultry and dairy mix, and an expected recovery in crop protection and Astec from 4Q.

* We have built in revenue/EBITDA/Adj. PAT CAGR of 9%/15%/20%. We broadly retain our FY26/FY27/FY28 EBITDA estimates and reiterate our BUY rating on the stock with an SOTP-based TP of INR700.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412