Buy ACME Solar Holdings Ltd for the Target Rs.370 by HSBC

* Early and larger commissioning of BESS sets the stage for monetising diurnal variation in power prices

* 4Q earnings grew 13% y-o-y, but increase in gross block and net debt are key items to watch

* Maintain Buy and increase TP to INR370 (from INR350) as we factor in merchant BESS in our estimates

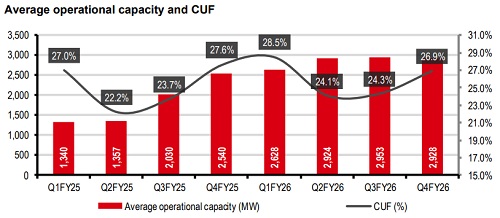

Q4FY26 review. ACME reported revenue growth of 13% y-o-y at INR5.5bn for Q4FY26, supported by generation growth of 14%. CUF for the quarter saw a 70bps y-o-y decline at 26.9% due to curtailment issues. Gross block increased by INR13.5bn q-o-q reflecting increased installation of Battery Energy Storage Systems (BESS) despite low generational capacity increase. This also resulted in net debt increase to 2.5x equity (1.7x in FY25) as the company spent INR64bn during the year. PAT growth of 13% y-o-y was largely the result of other income of cINR1.6bn (+200% y-o-y).

What we liked.

(1) The company has commissioned c2.4GWh of BESS capacity. Management guided for c10GWh of installed BESS capacity by end FY27 of which c8.5GWh will be operated on merchant basis until the respective FDRE projects are commissioned.

(2) Generation capacity commissioning is expected to be 1.5GW for FY27 as per the company.

(3) Days of sales outstanding saw a reduction to 14 in FY26 vs 42 in FY25.

What we didn’t like.

(1) Finance cost as a percentage of revenue increased to 62% in Q4FY26 vs 58% in the previous quarter, eating into earnings. PAT growth was supported by non-recurring hedging gains.

(2) Management churn continues with CFO resignation announced along with earnings.

Investment view

We believe ACME, a fully vertically integrated renewable IPP, is in a high growth phase adding significant capacity over the next two years. Strategically, the business is evolving from a pure-play solar provider to more complex firm and dispatchable renewable energy (FDRE) projects, which require a combination of solar, wind, and battery storage capacity. Further, it is using a strategy of early BESS commissioning to generate merchant revenue before the BESS is integrated into their FDRE projects. All this positions it well to benefit from India’s RE growth story

Valuation and risks.

We adjust our estimates to account for a more aggressive BESS strategy which is driving EBITDA and net debt increase. Our EPS estimates increased by 8-9% for FY27/FY28 and we introduce FY29 estimates. We value ACME on FY28 run-rate EBITDA, which is based on already-signed 25-year PPAs expected to be executed by end FY28. We assign a 10x EBITDA multiple which reflects growth. Adjusting for net debt as of March 2028, we derive an equity value of INR275bn. We discount it back to June 2026 (unchanged) to arrive at a TP of INR370 (INR350 earlier). Our TP implies c31% upside from current levels.

Downside risks:

(1) High leverage with projects financed with an 80-20 debt equity ratio

(2) rise in equipment and borrowing costs

(3) delay in commissioning of contracted capacity.

Above views are of the author and not of the website kindly read disclaimer