Buy Dixon Technologies Ltd for the Target Rs. 14,600 by Motilal Oswal Financial Services Ltd

Better-than-expected performance

Dixon Technologies (Dixon)’s 4QFY26 result was above our estimates, even amid the challenging environment. Mobile volumes were hit by weak demand on account of continued high memory prices. Going ahead for Dixon, the focus will be on 1) smartphone volume traction as demand has gradually started improving, 2) approval for the Vivo JV, 3) PLI 2.0 with a focus on boosting mobile exports, 4) pace of commissioning of the display facility during 2HFY27, and 5) volume improvement in exports. We tweak our estimates to bake in lower volumes and lower margins but higher smartphone realization. We reiterate our BUY rating with a DCF-based TP of INR14,600 (vs. INR14,700).

In-line revenue, beat on EBITDA and PAT

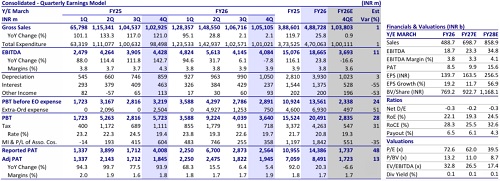

During 4QFY26, Dixon’s revenue was in line, while EBITDA and PAT beat our estimates. Consolidated revenue grew 2% YoY to INR105b. Revenue was in line, supported by better-than-expected performance of the mobile phones division, while the consumer electronics and home appliances segments underperformed. Absolute EBITDA declined 8% YoY to INR4.1b (11% above our estimates), while margins contracted 40bp YoY to 3.9% vs. our estimate of 3.6%. Better-than-expected margins for mobile and consumer electronics segments more than offset the home appliance margin weakness. Dixon’s adj. PAT grew 5% YoY to INR2b (13% ahead of our estimates). For FY26, revenue/ EBITDA/PAT grew 26%/24%/20% YoY to INR488b/INR18.7b/INR8.5b, while margin contracted 10bp YoY to 3.8%. For FY26, OCF/FCF rose 55%/185% YoY to INR17.8b/INR7.2b. The NWC position remained comfortable at -2 days.

Smartphone volumes to remain stable

The mobile phone business continued to face pressure from rising memory prices and softer industry demand. Despite this, revenue increased 4% YoY during the quarter with margins of 3.6% vs. our estimate of 2.7%. The company expects domestic smartphone volumes excluding Vivo to remain broadly stable at around 32m units in FY27, supported by higher wallet share from existing customers and new project wins. Revenue growth is expected to remain stronger than volume growth due to 12-15% higher realizations, led by memory price inflation and an improving product mix. The company is also scaling up exports through Motorola and Ismartu, with feature phone exports to Africa expected to start from 2QFY27, while smartphone exports are also being planned gradually. A potential PLI 2.0 framework focused on export-led manufacturing could further increase mobile export opportunities and add another 4-5m units over time. The 1m sq. ft. Noida facility is nearing completion and is expected to begin operations by 2QFY27. The Vivo-JV remains a key upside trigger, as it could potentially add 20-22m per annum in volumes with better realizations compared to the current portfolio.

Specialty EMS expansion

The company is building a specialty EMS platform across aerospace, defense, automotive, medical devices, and industrial electronics to diversify beyond mobile manufacturing and improve margins. Multiple inorganic opportunities are under evaluation, supported by a dedicated leadership team and a global consulting partner. The company expects specialty EMS to scale into an INR30-40b opportunity with structurally higher margins and lower dependence on government incentives compared to traditional EMS businesses. We have not factored these into our estimates currently.

Valuation and view

The stock is currently trading at 62.0x/39.5x P/E on FY27/28E earnings. We reiterate our BUY rating on the stock with a revised DCF-based TP of INR14,600 (INR14,700 earlier), implying a target P/E multiple of 55x on Jun’28E earnings.

Key risks and concerns

The key risks to our estimates and recommendations would come from the lowerthan-expected growth in the market opportunity, loss of relationships with key clients, increased competition, and limited bargaining power with clients.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412