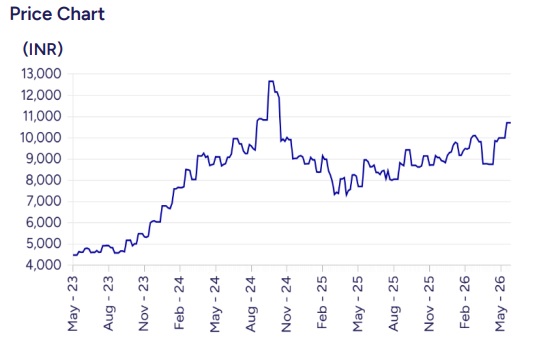

Hold Bajaj Auto Ltd for Target Rs.10,400 by Prabhudas Liladhar Capital Ltd

Strong Performance Aided by Margin Expansion

We downgrade the stock to ‘HOLD from ‘Accumulate’ due to run-up in prices following the buyback announcement and disruptions from the West Asia conflict. BJAUT’s Q4FY26 standalone revenue of INR160.1bn (+31.8% YoY, +5.2% QoQ) is 1.7% above BBGe (met PLe). Margins expanded as favorable Fx, mix and operating leverage more than offset RM inflation, higher discretionary spends and absorption of PM E-Drive (e3Ws) incentive withdrawal. BJAUT expects to outperform industry growth, driven by sustained gain in market share in 150cc+ motorcycles, EVs and exports. However, we note that its 75-125cc domestic motorcycle segment (~53% of its overall 2W volumes for FY26) has been losing market share. We expect overall volume/blended realization CAGR of 9.7%/3.4% over FY26-28E translating to revenue/EBITDA/EPS CAGR of 13.5%/13.9%/13.3%. Downgrade to ‘HOLD’ with TP of INR10,400 (previously INR10,000), valuing it at 23x (previously 22x) P/E on its FY28 standalone EPS.

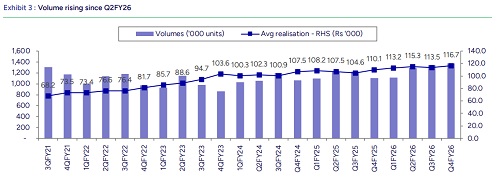

Realization grows 6.0% YoY to INR116.7k:

Gross margin at 30.1% (-10bps YoY/+20bps QoQ) beat BBGe/PLe by 55bps/30bps. EBITDA was INR33.2bn (+35.6% YoY), and EBITDA margin at 20.8% (+60bps YoY, flat QoQ) was 20bps above BBGe (met PLe). Adj PAT was INR27.2bn (+32.6% YoY), beating BBGe by 3.9% (met PLe). In FY26, op revenue was INR587.3bn (+17.4% YoY), EBITDA margin was 20.5% (+30bps YoY), EBITDA was INR120.2bn (+19.0% YoY), adj PAT was INR98.4bn (+20.7% YoY), FCF was above INR80bn, and surplus cash was above INR180bn

Price hike taken might soften demand:

Compared to Q4, steel prices have increased by +15%; copper, 20%, and aluminum and noble metals, 35%-45%. The management estimates RM cost inflation impact of 3.5-4% of revenue QoQ in Q1FY27. Price increase taken in Apr’26 has offset 40% of this impact. Accelerated cost optimization, reduced discretionary spends and further price hikes (last option) along with currency tailwind should cushion the margin drag. Rate settlement and supplier negotiation is happening more frequently (monthly vs. done quarterly previously).

Highest-ever quarterly/annual exports revenue of ~US$600mn/US$2.2bn:

FY26 was 2nd highest in terms of annual volumes, driven by LatAm (even as currency devaluation hasn’t yet impacted its economy), a recovering market in Nigeria (operating at 50% of its peak performance amid fuel price increases), and double-digit growth in Asia (Sri Lanka, Philippines and Nepal). BJAUT is advancing well against the competition from a new Chinese player (125cc bikes). FTAs, like the potential US-Mexico one, will further augment international business. In the top 30 global markets (~80% of emerging markets), BJAUT grew 2x vs. industry in Q4. KTM exports from India have revived (~17.5k units), and sales in Brazil crossed 10k units with manufacturing capacity increasing to 60k units/year (50k usable) with further capacity increase expected in a year.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

600-400.jpg)