Neutral Dr Reddy's Labs Ltd for the Target Rs. 1,195 by Motilal Oswal Financial Services Ltd

Limited niche opportunities weigh on earnings growth visibility

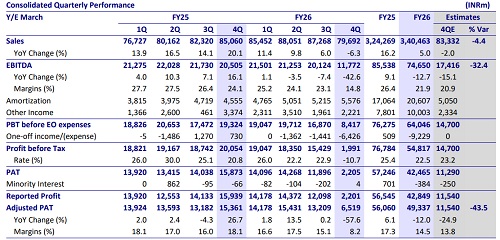

* Dr Reddy’s Labs (DRRD) delivered lower-than-expected 4Q performance with a 4%/32%/43% miss on sales/EBITDA/PAT. These misses were after adding shelf-stock adjustments related to g-Revlimid. Reduced sales in North America (NA) considerably hurt the performance for the quarter.

* After three years of robust growth in NA sales over FY22-25, FY26 witnessed a 23% YoY decline in sales, led by increased competition in g-Revlimid. DRRD had 25 launches in FY26, offsetting the adverse impact to some extent. ? Pricing pressure in generics dragged the EU revenue, and lower volume offtake in CIS countries hit the overall performance for the quarter.

* Enhanced focus on innovative products and higher marketing efforts led to considerable industry outperformance in the domestic formulation (DF) segment in 4QFY26.

* The NRT portfolio grew at a better-than-expected rate of 16% YoY for 4Q.

* We cut our earnings estimate by 25%/8% for FY27/FY28, factoring in

1) reduced profitability post-competition in g-Revlimid

2) delay in semaglutide launches in certain markets like Brazil/Canada

3) pricing pressure in the generics portfolio

4) lower operating leverage. We value DRRD at 18x 12M forward earnings to arrive at our TP of INR1,195

* DRRD’s earnings decelerated in FY25 and FY26 after recording a robust show during FY20-25. We expect the earnings to further decline in FY27 due to a lower pace of niche launches. Certain niche products like b-abatacept are under regulatory process, which might revive FY28 earnings, subject to timely approval. We reiterate our Neutral rating on the stock.

Lenalidomide normalization continues to put pressure on growth and profitability

* DRRD’s 4QFY26 revenue declined 11.6% YoY to INR75.2b (vs. our estimate of INR83.3b), impacted by a Shelf Stock Adjustment (INR4.5b; SSA) related to Lenalidomide. Adjusted for this, revenue declined 6.3% YoY to INR80b.

* Adjusted for the SSA, gross margin contracted 760bp YoY to 48%, due to reduced Lenalidomide sales/price erosion in NA/EU Generics businesses.

* EBITDA margin contracted 930bp YoY to 14.8% (vs. our estimate of 20.9%).

* EBITDA declined 42.6% YoY to INR11.7b (vs. our estimate of INR17.4b). This was adjusted against a one-off expense (INR1.1b) related to VAT liability.

* Further, adjusting for a one-off gain of INR1.9b on the sale of non-core assets, PAT declined 57.6% YoY to INR6.5b (vs. our estimate of INR11.5b).

* For FY26, its revenue increased 5%, while EBITDA/PAT declined 12.7%/12%

Strong growth across India, the EU, and EM offset by a sharp dip in NA

* NA sales declined 51% YoY to INR17.6b (~USD187m; 23% of sales). Adjusted for the SSA, NA sales declined 38% YoY to INR22.1b (~USD235m).

* Europe (EU) sales grew 14% YoY to INR14.5b (19% of sales), led by contributions from the NRT portfolio, product launches, higher volumes, and favorable forex movements. NRT sales increased 16% YoY to INR7b

* India sales grew 20% YoY to INR15.7b (21% of sales), driven by innovative product launches, price hikes, higher volumes, and contributions from recently acquired portfolios.

* Emerging market sales grew 29% YoY to INR18.1b (24% of sales).

* Pharmaceutical Services and Active Ingredients (PSAI) segment revenue declined 5% YoY to INR9.1b (12% of sales).

Highlights from the management commentary

* Compared to the earlier guidance of 12m units of Semaglutide sales, DRRD lowered the guidance to 10-11m units for FY27, considering some delay in approval. DRRD has assumed a price of USD30+ per unit, subject to competition.

* SGA spending would include higher marketing/promotional expenses for innovative products. Hence, SGA spending would be similar to that of FY27.

* With respect to the Intravenous (IV) version of b-Abatacept, DRRD awaits plant inspection at Bacchupally. DRRD continues to work on the subcutaneous version.

* DRRD expects GM to improve to 50-52% in FY27.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412