Buy Mahindra And Mahindra Ltd For Target Rs.3,963 by Motilal Oswal Financial Services Ltd

Strong growth guidance provided across segments

Will focus on ‘accelerating in uncertainty’

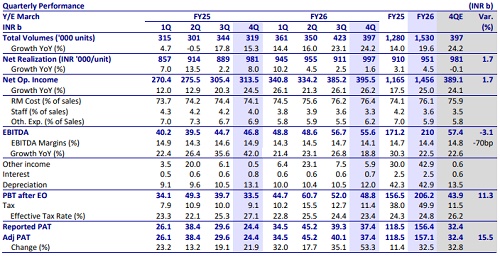

* Mahindra & Mahindra’s (MM) 4QFY26 PAT at INR37b was 15% ahead of our estimates, led by higher-than-expected other income, even as operational performance across the auto and farm segments was in line.

* On the back of its healthy launch pipeline and positive consumer sentiment, management has provided a strong outlook for FY27E across segments: tractor industry at mid-single digit, MM UV at mid to high teens, and LCV industry at high single digit. As such, we have raised our EPS estimates by 4%/3% over FY27E/FY28E. We estimate MM to post a CAGR of ~15%/12%/13% in revenue/EBITDA/PAT over FY26-28. Reiterate BUY with a TP of INR3,963 (based on Mar’28E SoTP).

PAT beat due to higher other income

* MM’s 4Q standalone revenue grew 26% YoY to INR395b (in line), driven primarily by a strong 24% volume growth and a blended ASP growth of 1.6%.

* Overall, EBITDA margins came in marginally lower than estimates at 14.1% (est of 14.8%). EBITDA grew 19% YoY to INR55.6b (in line).

* Auto revenues grew 25% YoY to INR311b (vs est of INR301b), while PBIT margins came in at 9.5% (in line).

* Farm revenues grew 32% YoY to INR84.8b (vs est of INR88.2b), while PBIT margins came in at 19.4% (in line, flat YoY)

* Other income grew 10x YoY to INR5.9b (vs est of INR631m). ? On the back of higher-than-expected other income, PAT grew 53% YoY to INR37.3b, 15% ahead of our estimates.

* FY26 performance: Revenue/EBITDA/PAT grew 25%/23%/33% to INR1.45t/INR209b/INR157b, respectively. OCF/FCF grew from INR166b/120b in FY25 to INR228b/166b.

Highlights from the management commentary

* Management has indicated that despite ongoing macro headwinds, it remains confident of delivering 15-20% EPS CAGR over the next five years as well, with a target to maintain RoE at 18%.

* Management expects the company’s SUV business to grow in the mid-tohigh teens in FY27, supported by strong demand for its models.

* During this quarter, it has added six ICE SUV launches and three BEV launches to its earlier planned launch pipeline till 2031. As a result, MM now plans to launch 10 ICE SUV products between April 2026 and 2031, including one mid-cycle enhancement and nine new SUV nameplates.

* The company expects the LCV industry to grow in high single digits in FY27.

* Management expects the tractor industry to grow in mid-single digits in FY27.

* On capacity, Mahindra’s ICE SUV capacity stood at 56.5K units per month as of FY26, while BEV capacity stood at 8K units per month. In FY27, the company plans to add another 3.5K units per month of ICE capacity. Further, the Chakan plant for the NU-IQ platform is expected to add 10K units per month of ICE capacity and 4K units per month of EVs by the start of FY28.

Valuation and view

* On the back of its healthy launch pipeline and positive consumer sentiment, management has provided a strong outlook for FY27E across segments: tractor industry at mid-single digit, MM UV at mid-to-high teens, and the LCV industry at high single digit.

* As such, we have raised our EPS estimates by 4%/3% over FY27E/FY28E. We estimate MM to post a CAGR of ~15%/12%/13% in revenue/EBITDA/PAT over FY26-28. Reiterate BUY with a TP of INR3,963 (based on Mar’28E SoTP).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)