Buy IndiaMART Ltd For Target Rs. 2,500 by Motilal Oswal Financial Services Ltd

ARPU doing the heavy lifting

Supplier softness persists following price hikes and macro conditions

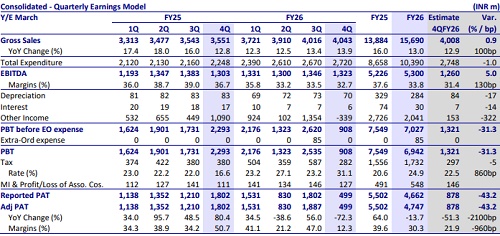

* IndiaMART (INMART) reported a 4QFY26 revenue growth of 14% YoY vs. our estimate of 13% YoY growth. Deferred revenue rose 16% YoY to INR19.6b. EBITDA margin declined ~80bp QoQ to 33%, above our estimate of 31.4%. Adj. PAT was INR500m, down 72% YoY, and below our estimate of INR878m.

* For FY26, revenue/EBITDA grew 13%/1.4%, while adj. PAT declined 15.3% YoY. We expect revenue/EBITDA to grow 12.7%/3.3%, while adjusted PAT is expected to dip 14.8% YoY (as other income normalizes) in 1QFY27. FY26 RoE was 20.7% (vs. 28.1%/17.7%/11.8% in FY25/24/23). We reiterate our BUY rating on the stock, citing undemanding valuations, with a TP of INR2,500.

Our view: Premium cohorts provide stability; churn remains broadly unchanged

* Paying suppliers weak in the near term; recovery depends on Silver churn normalization: INMART saw a QoQ decline of ~1.2k paying suppliers to ~220k in 4Q, despite a net addition of ~3.2k over FY26. The drop was largely due to slower gross adds post the Silver price hike and some one-off impact from geopolitical disruptions (~3k customers impact).

* Churn in the Silver segment (4% annual / ~7% monthly) continues to remain high. Gold and Platinum cohorts remain stable (75% of revenue) continue to see steady upsell, which, in our opinion, should support near-term growth even as additions stay muted. We currently model collections growth of ~10% over FY27E–FY28E, largely led by ARPU with gradual support from volumes.

* Cost discipline intact; margins steady despite limited operating leverage: EBITDA margin remained healthy at ~33–34%, with costs largely stable. Employee count declined slightly on a QoQ basis to 6,222, but this dip was not due to any structural cost action. Performance marketing spends remain below the INR100m quarterly target as experiments continue, suggesting limited near-term cost pressure. We expect margins to remain broadly range-bound at 32.6% in FY27E.

? Optional levers building gradually but not material yet: Busy continues to scale well (billing growth ~24% YoY in 4Q; ~43% in FY26), with deferred revenue growth (~44%) indicating strong traction. INMART’s accounting ecosystem now serves ~225k customers, creating future bundling optionality.

? The export business has scaled to ~INR600–700m in collections, and AI-led initiatives (voice bots handling ~80% interactions) are improving efficiency. ? While these are positives, they are not yet large enough to materially move overall growth, in our view. Over time, these could support ARPU and improve platform stickiness.

Valuation and changes to our estimates

* We continue to view INMART as a key beneficiary of the growing technology adoption by India’s MSME universe. We keep our estimates largely unchanged. We expect INMART to deliver an 11% revenue CAGR over FY26-28. We estimate the EBITDA margin at 32.6%/33.1% for FY27/FY28.

* Currently, INMART is trading at an undemanding valuation, in our view, as the valuations reflect uncertainties surrounding the churn rate, product-market fit, and subscriber growth. We value INMART on a DCF basis to arrive at our TP of INR2,500. Reiterate BUY.

Revenue in line and beat on margins; ARPU rises 8% YoY

* INMART reported a 4QFY26 revenue of INR4b (+14% YoY), in line with our estimate of 13%. For FY26, revenue stood at USD15.7b, up 11% YoY.

* Collections stood at INR5.9b (+9% YoY). Deferred revenue rose 16% YoY to INR19.6b. ? Paying subscribers declined by 1.2k QoQ. ARPU grew 8% YoY to INR67k.

* EBITDA margin was 33%, down 80bp QoQ; it was above our estimate of 31.4% due to lower manpower expenses. For FY26, adj. EBITDA margin stood at 33.8% vs. 37.6% in FY25.

* Adj. PAT was INR500m, down 72% YoY, below our estimate of INR878m due to lower other income.

* Total suppliers on the platform stood at 8.7m, up 5% YoY. ? Total cash and investments stood at INR32.8b.

* The company declared a final dividend of INR30/share for FY26 and a special dividend of INR30/share, aggregating to a total dividend of NR60/share for FY26.

Highlights from the management commentary

* Paying suppliers declined ~1,200 QoQ to ~2,20,000 in 4QFY26, FY26's net addition stood at ~3,200. Management attributed the decline to muted gross additions following the Silver tier price hike (implemented at the end of Q2FY26) and geopolitical disruption.

* Churn metrics remain differentiated across tiers: Platinum monthly churn remains well below 1%; Gold at 1–1.5%/month; Silver Annual at 4%/month; Silver Monthly elevated at 7%/month - no meaningful improvement QoQ.

* Performance marketing expenses remained below the stated INR100m/quarter target, as the company continues experimenting across categories and channels before committing full budgets.

* Consolidated collections grew 10% YoY to INR 5.95b in 4QFY26 and 14% YoY to INR 18.57b for FY26, steady monetization momentum despite headwinds at the Silver tier.

* A three-tier differential pricing architecture (standard, premium, and superpremium, covering 95%, 5%, and the top 1,000 categories, respectively) is being refined to better capture demand-supply dynamics at a category level.

Valuation and view

* We are confident of strong fundamental growth in operations, propelled by: 1) higher growth in digitization among SMEs; 2) the need for out-of-the-circle buyers; 3) a strong network effect; 4) over 70% market share in the underlying industry; 5) the ability to improve ARPU on low price sensitivity; and 6) higher operating leverage.

* We value INMART on a DCF basis to arrive at our TP of INR2,500. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)