Buy Waaree Energies Ltd for the Target Rs. 3,850 by Motilal Oswal Financial Services Ltd

Earnings momentum remains robust

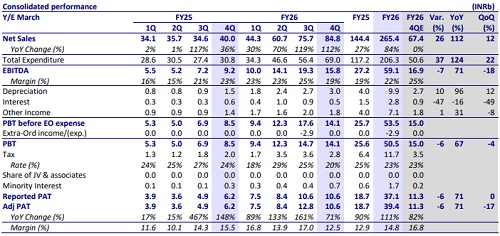

* Waaree Energies (WEL) reported robust revenue of INR84.8b (26% ahead of our estimates) in 4QFY26, but EBITDA came in 7% below our estimate due to a lower-than-expected EBITDA margin of 19%, impacted by elevated silver and copper prices, increased freight costs, a weaker overseas revenue mix, and reliance on externally procured DCR cells to fulfill certain module orders. Consequently, APAT came in at INR10.6b, missing estimates by 6%. Module production increased 19% QoQ; cell production declined 12% QoQ owing to the transition of three cell lines to G12R during the quarter.

* WEL’s FY26 Revenue/EBITDA/APAT came in at INR265b/INR59b/INR39b (+84%/117/110% YoY). Module/cell production for the year was 12.6GW/2.3GW (vs. 7.1GW/0.1GW in FY25).

* Key positives from the results: 1) management guidance of INR70-77b operating EBITDA for FY27 (implying ~25% EBITDA growth YoY), 2) strong traction in the retail segment (revenue of INR55b, +84% YoY), which contributed 20% to FY26 revenue, and 3) capacity expansion plans remain on track, including scaling up the US module capacity to 4.2GW over the next six months and commissioning 10GW of domestic cell capacity in 2HFY27, both of which are expected to support margin expansion.

* Key monitorables: 1) the impact of elevated input costs (silver and copper), higher freight expenses, and continued reliance on external DCR cell procurement on EBITDA margins in 1Q-2QFY27, 2) delay in commissioning target of the 10GW ingot-wafer facility to FY28 (from FY27 earlier), 3) working capital management, with working capital days increasing to 90 in FY26 from 45 in FY25, and 4) the relatively high proportion (65–70%) of the order book tied to long-range overseas orders (3-4 years).

* Earnings estimate and valuation changes: We have revised our FY27/FY28 revenue estimates upward by 8%/14% and EBITDA estimates by 3%/9%, resulting in a 7% increase in our TP. We reiterate our BUY rating on the stock, with a revised TP of INR3,850.

Robust revenue performance but margin disappoints

Financial Performance

* Revenue for 4QFY26 came in at INR84.8b (+112%YoY, +12%QoQ), beating our est. by 26%.

* However, 4QFY26 EBITDA stood at INR15.8b (+71% YoY, -18% QoQ), coming in 7% below our estimate due to a lower-than-expected EBITDA margin of 19% (vs. our estimate 25%).

* Consequently, adjusted PAT also missed our est. by 6% at INR10.6b (+71% YoY, -17% QoQ).

* The Board has approved a final dividend of INR2/share for FY26. Total dividend declared for FY26 stands at INR4/share.

Other Highlights:

* WEL produced 4.2GW of modules in 4QFY26 (+20% QoQ), reaching a full-year production of 12.6GW in FY26.

* It has guided for operating EBITDA of INR70-77b in FY27 (est. INR71b).

* Working capital days increased to 90 in FY26 from 45 in FY25.

* During the quarter, WEL operationalized 3GW of additional module capacity at Samakhiali in Gujarat.

* Further, the company seeks to raise up to INR100b via QIP or other permissible modes through equity shares/NCDs with warrants/other convertible securities, subject to shareholder and regulatory approvals.

Highlights of 4QFY26 performance

* EBITDA margin contracted to 19% in 4QFY26 (25%/23% in 3QFY26/4QFY25).

* 10GW of additional cell capacity is expected to come online from 2HFY27 onwards.

* WEL’s ingot-wafer capacity is expected to be commissioned by FY28 at its Nagpur facility.

* Solar glass facility (2,500 TPD) is expected to be commissioned in 24 months.

* The increase of US module capacity to 4.2GW in six months is a critical catalyst to help improve supplies to a strong US market.

* WEL’s G12R transition is underway, which is expected to be completed by 1HFY27. This is expected to improve realizations by 10-12%.

* The Middle East crisis has delayed overseas deliveries; this is expected to be rolled over to 1QFY27.

* Going forward, the company aims to unlock more export markets in Europe, Africa, and Middle East.

* An INR100b fundraiser is being planned to fund the Waaree 2.0 journey.

Valuation and view

* The valuation of WEL has been derived through a sum-of-the-parts (SoTP) methodology, resulting in a TP of INR3,725/share.

* The domestic module business is valued at 13x FY28E EBITDA. The US module business is valued at 12x FY28E EBITDA, which is in line with global peers. The new business segment, valued at 10x FY28E EBITDA, is consistent with domestic peer valuations. The sum of these segment valuations (adjusting for net debt) results in a TP of INR3,850/share.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412